Key Takeaways

PayFi stands for Payment Finance or Payment Financing and combines payments with onchain liquidity and financing infrastructure.

It aims to solve problems such as slow settlement, prefunding, fragmented intermediaries, and inefficient working capital in global payments.

PayFi usually relies on stablecoins, blockchain rails, tokenized receivables, compliance infrastructure, and liquidity providers.

The model is especially relevant for cross-border payments, remittances, card settlement, payroll, and merchant financing.

As of April 2026, PayFi is being pushed most visibly by projects and ecosystems such as Huma, Stellar, Solana ecosystem players like PolyFlow and Perena, and other infrastructure providers focused on stablecoin-enabled financial flows.

Payments are supposed to be simple. Money should move from one party to another quickly, cheaply, and with minimal friction. But in reality, traditional payment systems are often slow, fragmented, and capital-intensive. Cross-border transfers can take days. Merchants and payment processors frequently deal with delayed settlement. Businesses often have to pre-fund accounts in multiple regions just to keep money moving. That inefficiency is one of the main reasons the crypto industry has become so interested in PayFi, short for Payment Finance or Payment Financing.

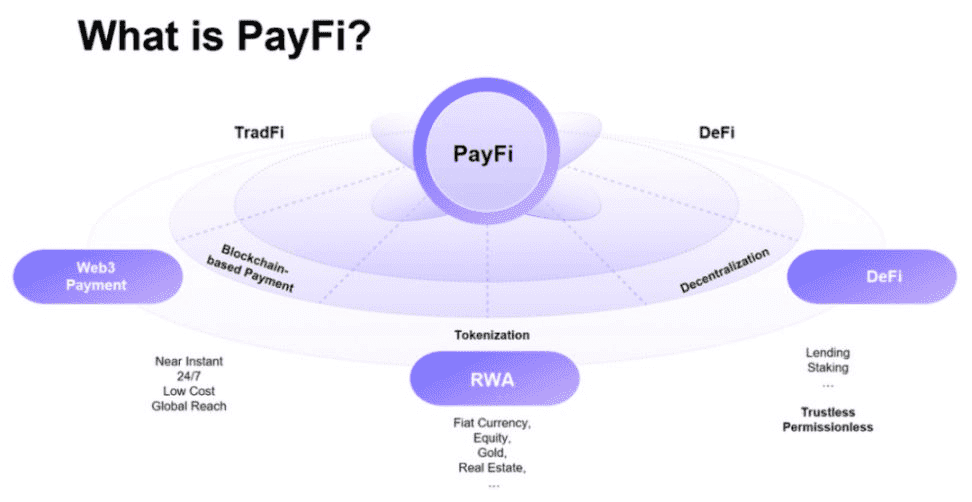

At a high level, PayFi describes the combination of payments infrastructure and onchain liquidity. Instead of treating payment settlement and financing as two separate systems, PayFi tries to merge them using stablecoins, blockchain rails, tokenized receivables, and programmable liquidity. Stellar’s explainer defines PayFi as the integration of payments with onchain financing and blockchain technology to enable the free flow of value onchain. Huma’s materials frame it similarly, describing PayFi as a way to use tokenized receivables and blockchain-based financing to unlock faster and more affordable liquidity.

In simpler terms, PayFi is about making money move faster while also making capital more efficient. A payment is not just a transfer anymore. It can become a financing event, a yield-bearing asset, a programmable cash flow, or collateral for instant liquidity. That is why PayFi is increasingly being discussed as one of the more important bridges between stablecoins, RWAs, DeFi, and real-world commerce.

What Does PayFi Mean?

The easiest way to understand PayFi is to compare it with ordinary digital payments.

In a traditional payment flow, money may pass through multiple banks, processors, settlement agents, and clearing systems before it finally arrives. Even if the end user sees a simple card swipe or bank transfer, the back-end process can involve settlement delays, counterparty risk, and trapped capital. Huma’s explainer says traditional payment systems are often slow, expensive, and inaccessible, while PayFi uses Web3 rails to make payments faster, cheaper, and more liquid. Transak’s 2026 overview adds that PayFi uses stablecoin rails and programmable digital assets to move and settle value in real time, reducing the need for prefunding and delayed settlement.

That means PayFi is not just “paying with crypto.” A person buying coffee with a stablecoin is not automatically using PayFi in the deeper sense. PayFi becomes more meaningful when payment flows and financing are linked together. For example, a business waiting to receive settlement from a payment processor might use tokenized receivables to access capital immediately. A remittance company might settle faster onchain while financing its working capital through stablecoin liquidity. A card settlement pipeline might tokenize future receivables and let global capital fund them.

This is why many PayFi discussions revolve around the time value of money. In a notable Huma post, Lily Liu, President of the Solana Foundation, described PayFi as “the creation of new financial markets around the time value of money,” emphasizing that onchain finance can enable new financial primitives and product experiences. That description captures the core idea well: if stablecoins can move instantly, then delays in payment settlement can be converted into programmable financing opportunities.

What is PayFi (source)

Why PayFi Matters

PayFi matters because global payments are a massive market, but the infrastructure underneath them is often outdated.

Many businesses have to lock up capital before it is actually needed. For example, they may pre-fund accounts in different countries to ensure future payments can settle on time. They may also wait days for receivables to clear, even though the economic activity has already happened. Stellar’s PayFi overview says the category is designed to enable the free flow of value onchain, while Huma’s materials argue that PayFi can synchronize money movement with modern commerce through real-time settlement.

For crypto, this is a big deal because stablecoins already proved that value can move globally at internet speed. The next step is making those payment flows economically productive. Instead of leaving capital idle while businesses wait for settlement, PayFi tries to turn future payment claims into financeable onchain assets. CoinMarketCap’s glossary describes PayFi as operating like a flywheel between TradFi and DeFi, using stablecoins and blockchain technology to accelerate payment flows while improving capital efficiency.

In practical terms, that could mean:

Faster settlement for merchants,

Better liquidity for payment companies,

Cheaper cross-border transfers,

New yield opportunities for capital providers,

More programmable financial products built on top of payment flows.

How PayFi Works

Most PayFi systems use a combination of five building blocks.

Stablecoin Payment Rails

Stablecoins are usually the base layer. They provide the digital dollars or dollar-like assets that move onchain quickly and globally. Solana’s institutional payments page highlights low-cost, near-instant settlement as one reason major payment networks are building around stablecoins, while Transak notes that PayFi relies on stablecoin rails to embed settlement and logic directly into the payment flow.

Without stablecoins, PayFi loses much of its appeal. The entire model depends on being able to move value rapidly and predictably, often with less friction than correspondent banking networks.

Tokenized Receivables or Payment Claims

The next layer is the financial claim itself. A payment processor, merchant network, remittance platform, or payroll business may have future receivables that are expected to settle soon. Huma’s explanation says PayFi can use tokenized receivables as collateral, allowing businesses to access instant, borderless financing with high liquidity.

This is a key point. PayFi is not usually lending against random crypto collateral. It is often financing real payment activity—money that is expected to arrive based on actual invoices, settlement flows, card transactions, wages, or remittance obligations.

Onchain Liquidity Providers

Someone still needs to supply the capital. In PayFi, that role can be played by liquidity providers, vault depositors, institutional lenders, or tokenized yield participants. Huma’s Huma 2.0 FAQ says the product is designed to let anyone access institutional-grade PayFi yields, while its overview says those yields come from deploying capital into PayFi applications that generate revenue through transaction fees from businesses using accelerated payment solutions.

This gives PayFi a DeFi-like side. Global capital can fund real-world payment flows and potentially earn yield from the fees and financing spreads generated by that activity.

Compliance, Identity, and Attestation

Payments touch the real world, so compliance matters. This is one reason PayFi is often discussed alongside identity, attestations, and regulated infrastructure. The Solana Attestation Service announcement describes PolyFlow’s PayFi infrastructure as anchoring transaction proofs and participant credentials onchain to make payments traceable, verifiable, and tamper-proof.

In other words, PayFi is not just about speed. It also needs trust layers for businesses, institutions, and regulators.

Settlement and Financing Logic

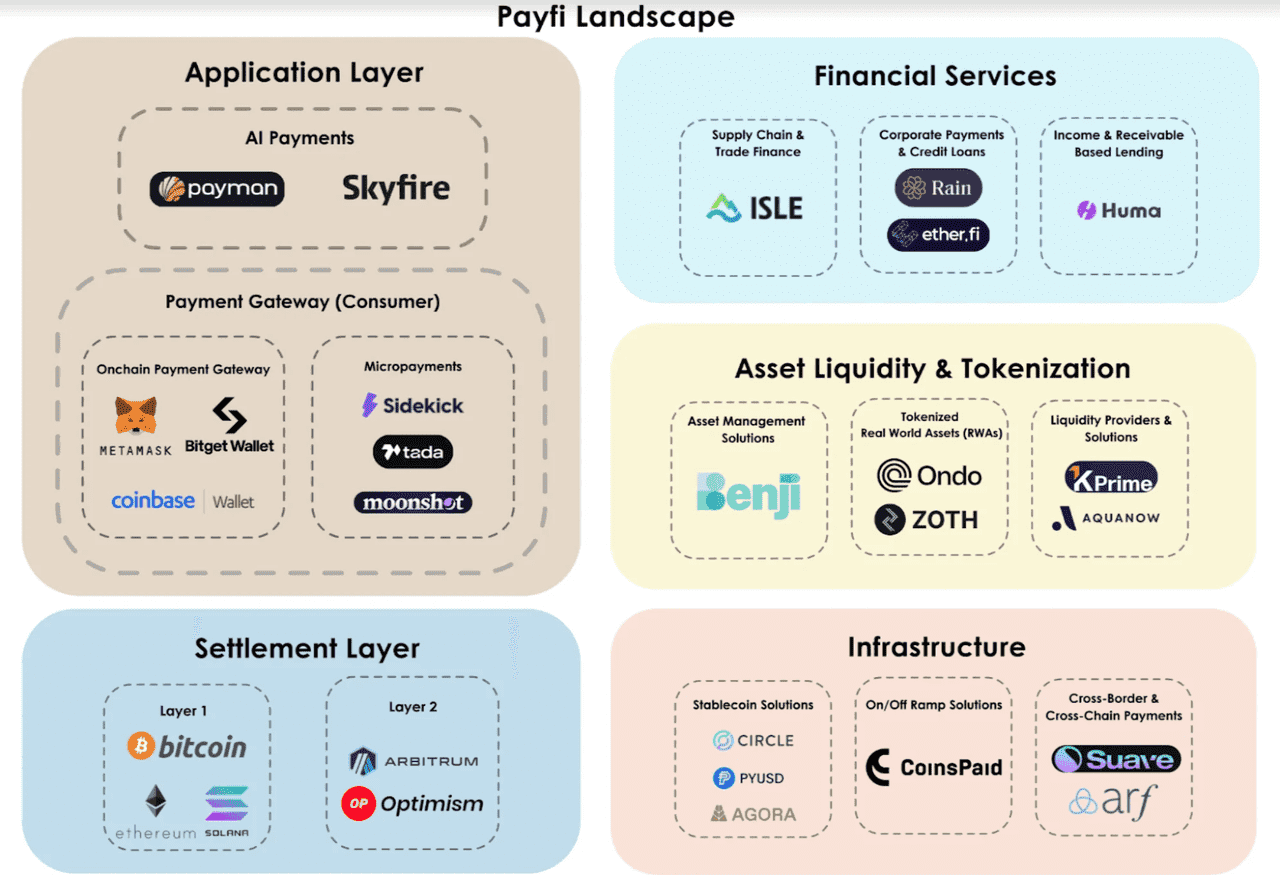

Finally, the system needs logic that determines when financing is extended, when payments settle, how risk is priced, and how fees or yields are distributed. Huma’s “PayFi Stack” describes a modular framework spanning chain infrastructure, stablecoins, custody, compliance, financing, and applications. That suggests PayFi is best understood as a full-stack financial architecture, not a single protocol feature.

PayFi Landscape (source)

PayFi vs Traditional Payments

Traditional payments and PayFi may look similar on the surface—they both move money—but the back-end assumptions are very different.

Traditional payment systems often rely on batch settlement, bank intermediaries, delayed reconciliation, and siloed financing. PayFi tries to compress these functions into an onchain system where settlement and financing can happen in much closer coordination. Huma’s “Why Huma?” page says PayFi creates a new standard that is faster, fairer, and always on, while Transak emphasizes that it removes the need for prefunding and fragmented intermediaries.

That can create several advantages:

faster settlement, because stablecoins move continuously rather than in banking windows,

better capital efficiency, because receivables can be financed earlier,

global accessibility, because onchain rails are not limited by local banking hours,

and programmability, because payment and financing terms can be embedded in smart contracts or tokenized products.

Of course, traditional systems still have strengths, especially in regulatory integration and incumbent merchant acceptance. But PayFi’s promise is that the back-end finance layer can be rebuilt for a world where money moves more like data.

Common Use Cases for PayFi

Cross-Border Payments

Cross-border transfers are one of the clearest PayFi use cases. They are often slow and expensive in traditional finance, especially when multiple correspondent banks are involved. Huma’s materials specifically reference cross-border payment solutions, and Stellar’s PayFi explainer also frames the category around removing friction from global value transfer.

Remittances

Remittance corridors can also benefit. A PayFi model can allow value to move via stablecoins while financing or liquidity layers reduce delays and working-capital friction for service providers. Stellar’s educational materials and broader PayFi explainers place remittances among the natural applications of Payment Finance.

Card Settlement

Card payments often involve settlement delays, reserve requirements, and operational financing needs. Huma’s “What is Huma?” page explicitly lists card payments as one of the real-world payment asset categories it serves, alongside payroll advances and cross-border settlements.

Payroll and Wage Access

Payroll is another strong fit because employees often need money sooner than the underlying employer settlement cycle allows. Huma’s docs also mention payroll advances as part of its PayFi network’s real-world payment assets.

Merchant and Fintech Working Capital

Fintechs and payment companies often carry receivables, float costs, and treasury inefficiencies. PayFi can potentially let them tokenize those flows, access liquidity sooner, and optimize settlement. PolyFlow’s materials describe the company as building PayFi infrastructure that unites traditional and crypto payments with DeFi, which is exactly the type of merchant-and-fintech bridge this category targets.

Key Projects and Ecosystems in PayFi

As of April 2026, Huma is probably the most prominent project explicitly branding itself around PayFi. Its docs call Huma “the first PayFi network,” and its newer product materials describe permissionless access to institutional-grade PayFi yields through Huma 2.0.

Stellar has also published educational material framing PayFi as a broader category, which is notable because Stellar has long focused on payment rails and cross-border settlement. That gives the concept more credibility as a sector narrative, not just a single project slogan.

On the Solana side, ecosystem participants such as PolyFlow and Perena are helping push related themes around stablecoin liquidity, settlement infrastructure, and payment-focused financial design. PolyFlow’s public materials explicitly use the PayFi label, while Solana’s March 2026 podcast with Perena’s founder discusses the broader importance of PayFi for global finance.

This does not mean the category is already mature. It is still early, and different teams use the term slightly differently. But the direction is clear: PayFi is becoming a recognized narrative around stablecoins and real-world financial flows.

PayFi Narrative Harmonies

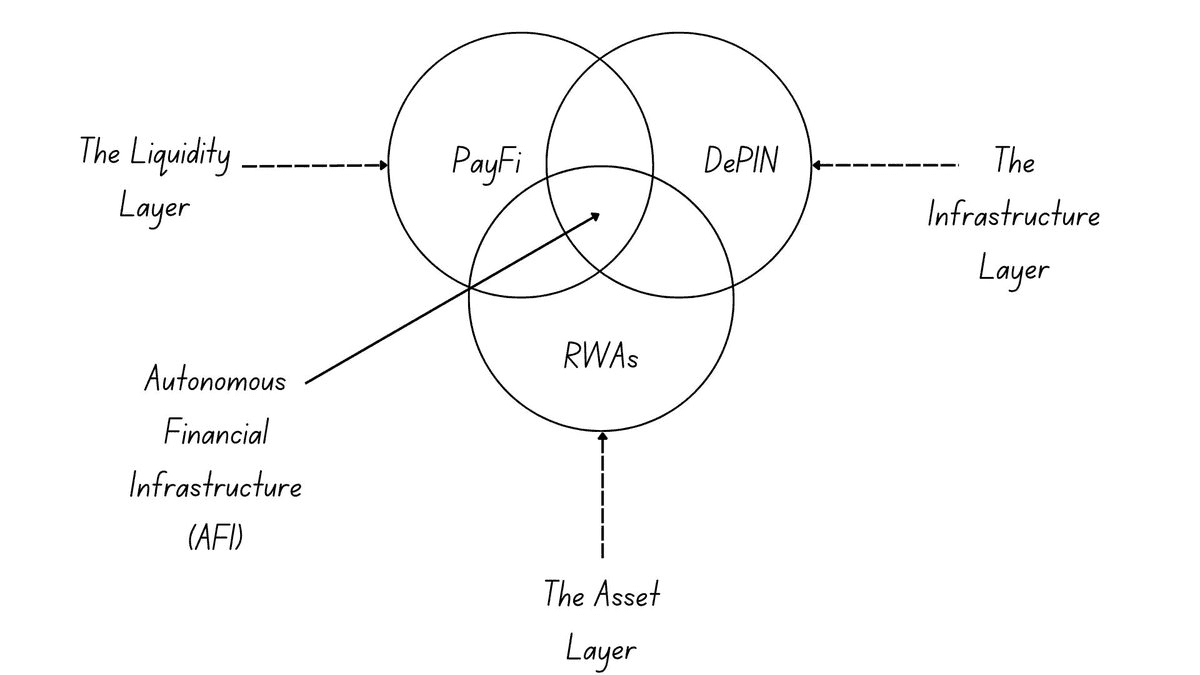

Why PayFi Is Related to RWAs

PayFi is often discussed alongside real-world assets because the cash flows behind payments are real economic claims.

If a protocol finances invoices, merchant receivables, remittance flows, or card settlements, those are not purely crypto-native assets. They are claims on real-world money movement. Huma explicitly describes its network as connecting global capital to real-world payment assets such as cross-border settlements, card payments, and payroll advances.

That is why PayFi can be seen as an RWA sub-sector. Instead of tokenizing Treasuries or real estate, it tokenizes or finances payment-linked cash flows. In that sense, PayFi sits at the overlap of RWAs, stablecoins, and DeFi credit.

Risks and Challenges of PayFi

PayFi is promising, but it is not risk-free.

The first challenge is regulatory complexity. Payments and financing are both heavily regulated in many jurisdictions, so projects must navigate compliance, licensing, KYC, AML, and potentially securities or lending rules depending on how products are structured. The strong emphasis on compliance and attestation in PayFi stacks shows that the sector is aware of this challenge.

The second is credit and underwriting risk. If PayFi systems are financing real receivables or settlement flows, someone must assess whether those claims are high quality and likely to be repaid. That means the category is not just about technology; it also depends on strong risk management. Huma’s product materials emphasize institutional-grade access and real-world payment assets, which implies underwriting discipline matters.

The third is stablecoin and blockchain infrastructure risk. PayFi often depends on stablecoins, settlement chains, smart contracts, and cross-border liquidity. Problems in any of those layers can affect the full payment flow. Solana, Stellar, and other ecosystems emphasize the importance of speed and low-cost settlement precisely because the base rails matter so much.

The fourth is narrative inflation. Because PayFi is becoming a popular term, some projects may use it loosely for almost any crypto payment product. Investors and readers should ask a simple question: Is this actually integrating payments with financing, or is it just a payments app using a trendy label? That distinction matters.

Conclusion

PayFi is one of the more interesting crypto narratives because it addresses a real problem: global payments still waste time, capital, and operational resources.

By combining stablecoins, onchain liquidity, tokenized receivables, and programmable settlement, PayFi aims to make payments not only faster, but also more financially efficient. That is why the category is attracting attention from payment-focused chains, stablecoin ecosystems, and protocols like Huma that want to connect DeFi capital to real-world economic activity.

The simplest way to understand the thesis is this: PayFi turns payment flows into financeable, programmable onchain assets. If stablecoins were the first step in bringing dollars onchain, PayFi may be part of the next step—bringing the business logic, working capital, and financing infrastructure around those dollars onchain too.

As stablecoins, RWAs, and onchain finance continue to converge, PayFi could become an increasingly important category for both builders and traders. For users looking to stay ahead of emerging crypto sectors, from PayFi and RWAs to AI agents and TradFi, Phemex offers a secure and user-friendly platform to track new narratives, explore market opportunities, and sharpen your trading edge.