Morgan Stanley filed an early-form prospectus with the SEC for a spot Ethereum ETF called the Morgan Stanley Ethereum Trust, and the document includes a staking component that would let the fund earn yield on the ETH it holds. The filing lands while ETH trades at $1,618.80, down 2.62% on the day, deep inside a broad crypto selloff that has pulled most large-cap tokens lower through June. For a bank that has spent the past year building out a crypto-ETF shelf, the timing says more about conviction than about chasing momentum.

This is not Morgan Stanley's first crypto-ETF move. The firm already has a bitcoin ETF filing (MSBT) and a solana ETF filing (MSOL) in the pipeline, and the Ethereum trust extends that lineup to the second-largest asset in the market. The staking angle is the part worth slowing down for, because a bank-issued product that captures native ETH yield changes the math for the institutions that buy it.

Here is what the filing actually contains, why the staking feature matters, how it stacks up against existing staked-ETH products, and what the SEC review path looks like from here.

What the Morgan Stanley Ethereum Filing Actually Is

The document Morgan Stanley submitted is an early-form registration statement, the opening step a sponsor takes to bring a new exchange-traded product to market. The filing itself is searchable through SEC EDGAR company search, the public database where the registration documents are posted. It registers the Morgan Stanley Ethereum Trust as a spot vehicle, meaning the fund would hold actual Ethereum rather than futures contracts, and each share would represent a claim on a slice of that underlying ETH. A spot structure tracks the asset directly, which is why these products tend to draw far more institutional capital than the futures-based wrappers that came before them.

What separates this filing from a plain spot ETF is one clause. The prospectus provides for the trust to stake a portion of its ETH holdings, putting that Ethereum to work securing the network and collecting the staking rewards the protocol pays out. A standard spot ETF holds the asset and does nothing with it. A staking-enabled spot ETF holds the asset and earns on it, and that single difference reshapes how the product competes for capital.

The filing slots into a wider Morgan Stanley crypto-ETF effort. The firm's bitcoin product (MSBT) and solana product (MSOL) are already on file, and the Ethereum trust gives the bank coverage across the three assets that institutional desks ask about most. A traditional-finance heavyweight assembling a full crypto-ETF shelf, rather than testing the water with a single bitcoin fund, is the signal here. Details on the firm's broader investment-management business sit on the Morgan Stanley Investment Management site.

The Staking Angle Explained

Staking is how proof-of-stake networks like Ethereum stay secure. Validators lock up ETH as collateral, take turns proposing and confirming blocks, and the protocol pays them a yield for the work. That yield currently runs in the low-to-mid single digits annually, and it is paid in ETH, so a holder who stakes is accumulating more of the asset over time instead of letting it sit idle in cold storage.

For an ETF, the appeal is direct. A spot Ethereum fund that stakes can pass some of that native yield through to shareholders or use it to offset the fund's management fee, which lowers the real cost of holding the product. A non-staking ETF leaves that yield on the table entirely. Put two otherwise identical spot ETH funds side by side, one staking and one not, and the staking version delivers a measurably better total return over a full year. That is a hard advantage to ignore once more than one issuer is in the market.

The trade-off is that staking introduces operational complexity a plain fund never has to manage. Staked ETH can face exit-queue delays when validators want to unstake, which affects how quickly the fund can meet redemptions. There is slashing risk, the protocol penalty for validator misbehavior or downtime, which a sponsor mitigates by using professional staking infrastructure and custodians. And the yield itself is variable, moving with network participation rather than sitting at a fixed rate. None of these are dealbreakers, but they are the reasons a staking ETF takes longer to structure and longer for regulators to sign off on than a vanilla one.

Why a Bank-Issued Staked-ETH ETF Matters for Institutional Adoption

Plenty of institutions want ETH exposure but cannot or will not run their own staking operation. Setting up validators, managing keys, handling slashing risk, and tracking variable rewards is operational overhead that most allocators, pensions, and registered advisors are not built to carry. A staking ETF removes that barrier completely. The buyer gets spot ETH exposure plus the network yield in a single regulated ticker that trades on a normal brokerage account, with no wallet, no validator, and no key management.

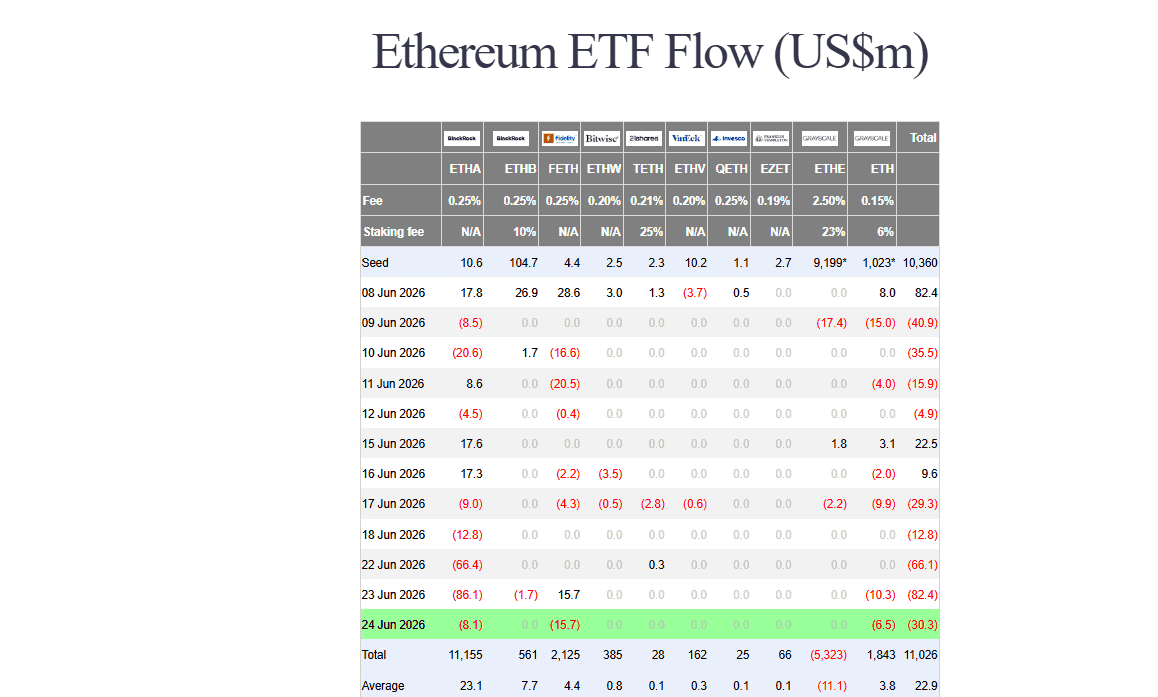

Source: Farside

The issuer matters as much as the structure. Morgan Stanley is a globally systemic bank with deep distribution into wealth-management channels, financial advisors, and institutional clients. When a firm of that size sponsors a product, it carries weight with allocators who would never touch a crypto-native wrapper, and it pulls Ethereum further into the same conversation that already includes bitcoin ETFs. The reflexive comparison is the bitcoin spot-ETF wave, where bank-grade products opened the asset to a buyer base that had been sitting on the sidelines, and the flows that followed were measured in tens of billions of dollars. Reading those flows became its own discipline, and the same ETF flow dynamics will shape how ETH performs if a staked product reaches the market.

There is a structural point underneath the headline too. A staking ETF does not just hold ETH, it locks ETH into validators, which pulls supply out of circulation for as long as the fund holds it. If staked Ethereum products gather assets the way the bitcoin funds did, a meaningful share of supply moves into validator contracts and stops trading freely. That same dynamic is part of what makes the broader Ethereum and Layer 2 ecosystem story matter, because activity on those networks ultimately settles back to the base layer that the ETF would be staking.

How It Compares to Existing Staked-ETH Products

Staked-ETH exposure already exists, but not in the form Morgan Stanley is proposing. Liquid staking tokens let holders stake ETH and receive a tradable receipt token in return, which keeps the position liquid while it earns. That model works, but it lives entirely on-chain and asks the user to manage a wallet, understand smart-contract risk, and handle the receipt token themselves. It is a crypto-native solution for crypto-native users, not something a traditional wealth-management client reaches for.

The current crop of spot Ethereum ETFs solved the access problem but skipped the yield. The first wave of approved ETH funds held spot Ethereum in a clean regulated wrapper, yet most launched without a staking feature because the regulatory path for staking inside an ETF was unsettled at the time. That left a gap. Investors could get ETH exposure through a ticker, or they could get the yield through on-chain staking, but not both inside one bank-grade product.

The SEC Approval Path and Timeline

An early-form filing is the start of a process, not the finish. After a sponsor submits the registration statement, the SEC reviews the disclosures, often issues rounds of comments, and the sponsor amends the document in response. For an ETF that holds and stakes a crypto asset, the staking mechanics draw extra scrutiny, because the regulator wants clarity on how rewards are handled, how redemptions work when assets are locked in validators, and how slashing and custody risks are disclosed to investors. That back-and-forth takes time and is the reason a launch date cannot be pinned down at the filing stage.

The encouraging context is that the regulatory posture toward staking inside ETFs has been softening. Spot Ethereum ETFs already exist as approved products, so the core question of a US-listed fund holding ETH is settled. The open question is the staking layer, and momentum has been moving toward allowing it rather than blocking it. That backdrop makes a staking-enabled approval more plausible than it would have been a year ago, even if the exact timing stays in the SEC's hands.

No firm launch date exists yet, and any specific date circulating before the SEC completes its review is speculation. The honest framing is that the Morgan Stanley Ethereum Trust is pending SEC review, that the staking component adds review complexity, and that approval depends on the comment process running its course. Traders watching this should track the filing's amendments and the SEC's published decisions rather than any rumored countdown.

What It Means for ETH

The filing and the price are telling two different stories right now. ETH is at $1,618.80, down 2.62% on the day, caught in a market-wide selloff that has little to do with Ethereum-specific news and everything to do with broad risk-off positioning. A weak tape can run for weeks regardless of how constructive the longer-term setup looks, and nobody should treat a single filing as a reason the chart turns tomorrow.

The signal is structural and slower. A globally systemic bank filing for a staked-ETH product extends a crypto-ETF push that already covers bitcoin and solana, and it points institutional demand toward Ethereum at a moment when the price is reflecting fear rather than fundamentals. If a staked ETF reaches the market and gathers assets, it adds a steady institutional bid and pulls supply into validators, and both effects work in ETH's favor over a horizon measured in quarters, not days. The relationship between regulated ETF demand and the underlying asset is the same one that played out across the bitcoin ETF wave that reshaped that market, and the same one that gives products built around stablecoins and other regulated rails their institutional pull. Coverage of the filing and the broader ETF push is tracked on the CoinDesk markets section.

Frequently Asked Questions

What is a spot Ethereum ETF?

A spot Ethereum ETF is an exchange-traded fund that holds actual ETH, so each share represents a direct claim on the underlying Ethereum the fund custodies. It lets investors get ETH exposure through a regulated brokerage ticker without holding a wallet or managing private keys, which is why these products draw far more institutional capital than futures-based alternatives.

Can an ETF stake Ethereum?

Yes, a spot Ethereum ETF can be structured to stake a portion of its ETH holdings, which lets the fund earn the network's native staking yield and either pass it to shareholders or use it to offset fees. The Morgan Stanley filing includes exactly this feature, though staking adds operational and regulatory complexity around redemptions, slashing risk, and custody that a plain spot fund does not have to manage.

When will the Morgan Stanley Ethereum ETF launch?

No launch date is confirmed. The filing is an early-form registration statement that is pending SEC review, and the staking component adds extra scrutiny to that process, so any specific date circulating now is speculation. Approval depends on the SEC's comment process running its full course rather than on a fixed timeline.

Bottom Line

Morgan Stanley filing for a spot Ethereum ETF with staking is a long-term institutional signal landing against a weak tape, and the two should not be confused. ETH at $1,618.80 and down 2.62% reflects a broad selloff, while the filing reflects a globally systemic bank extending its crypto-ETF shelf beyond bitcoin and solana to the second-largest asset in the market. The staking feature is the real story, because a single regulated ticker that delivers both ETH exposure and native yield is the product institutions have been asking for since the first spot ETH funds launched without it. Watch the filing's amendments and the SEC's published decisions for the staking sign-off, not a rumored launch date, and treat sustained ETF inflows as the catalyst that matters once a product clears review. If the staked-ETF wave for ETH echoes what bank-grade bitcoin funds did, the supply pulled into validators and the steady institutional bid are what tighten the setup over the coming quarters.

This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency trading involves substantial risk. Always conduct your own research before making trading decisions.