Executive Summary

For the past four years, the prevailing narrative surrounding Meta Platforms Inc. (formerly Facebook) within the digital asset sector has been defined by the spectacular, highly publicized failure of the Libra/Diem project. Chased out of the market in 2022 by a coordinated, unprecedented global regulatory crackdown, Mark Zuckerberg’s ambitions to engineer a sovereign digital currency were seemingly permanently shelved. The market assumed Meta had retreated to the safer harbors of Artificial Intelligence and the Metaverse.

However, as we progress through the first quarter of 2026, the paradigm has violently shifted. Meta is orchestrating a massive, strategically cunning comeback into the stablecoin sector.

According to highly credible institutional leaks, Meta aims to integrate dollar-pegged stablecoin payments across its family of apps—most critically, WhatsApp and Instagram—by the second half of 2026. Unlike the hubristic, ground-up approach of Libra, Meta is executing a sophisticated "arm's length" strategy. The tech conglomerate has reportedly issued a Request for Product (RFP) to third-party vendors to administer the stablecoin architecture, with financial infrastructure giant Stripe (and its recently acquired stablecoin specialist, Bridge) emerging as the overwhelmingly likely partner.

The stakes have never been higher. According to real-time on-chain data, the total stablecoin market capitalization has swelled to an astonishing $309.45 billion. This is no longer a niche crypto trading instrument; it is the parallel circulatory system of the U.S. Dollar.

Simultaneously, the regulatory environment is undergoing a massive, synchronized global evolution. From the passage of the U.S. GENIUS Act in 2025 to the UK Financial Conduct Authority's (FCA) brand-new stablecoin sandbox launched just this week (February 25, 2026), the legal runway for corporate stablecoin integration is finally being cleared. Yet, a fierce new legislative battle over "Stablecoin Yield" threatens a $1.3 trillion deposit flight from traditional banks—a battle Meta will undoubtedly exploit.

This research report provides an exhaustive, institutional-grade analysis of Meta’s 2026 stablecoin masterplan. We dissect the ghosts of the Libra failure, analyze the macroeconomic rationale driving the "Super-App" arms race, evaluate the radically shifting US and UK regulatory landscapes, dissect the current oligopolistic state of the $309B stablecoin market, and provide highly actionable tactical perspectives for professional traders navigating this seismic shift in global payment rails.

Part 1: The Breaking Catalyst – Unpacking Meta’s 2026 Masterplan

The recent leaks regarding Meta’s strategic pivot represent one of the most significant macro-crypto developments of the decade. The details of the operation, while still officially under wraps, paint a picture of a company that has learned profound, painful lessons from its past regulatory traumas.

The "Arm's Length" Integration Strategy

In 2019, Meta attempted to act as a quasi-central bank. They created a proprietary blockchain (Move) and formed a Swiss-based association to govern a new global currency. In 2026, Meta has entirely abandoned the ambition of being a digital currency issuer.

Instead, Meta is positioning itself purely as the distribution network and front-end interface. By issuing an RFP to third-party firms to help administer stablecoin-based payments, Meta effectively offloads the massive regulatory, compliance, and collateral-management burdens to specialized financial technology partners.

The core objective is the seamless implementation of a new digital wallet natively integrated into the Meta ecosystem. This will allow users to send, receive, and hold dollar-pegged value as easily as sending a WhatsApp text message, without ever realizing they are interacting with blockchain architecture.

The Stripe and Bridge Connection: A Match Made in Silicon Valley

Market intelligence heavily points to Stripe as the primary candidate for piloting Meta’s stablecoin infrastructure. The connective tissue here is undeniable, and for institutional analysts, it is the smoking gun.

The Board Seat: In April 2025, Stripe CEO Patrick Collison officially joined Meta's board of directors. This signaled a deep, strategic alignment between the premier Web2 payment processor and the world's largest social network.

The Bridge Acquisition: Last year, Stripe made shockwaves in the crypto industry by acquiring the stablecoin API platform Bridge for a staggering premium. Bridge specializes in allowing non-crypto-native enterprises to seamlessly issue, accept, and manage stablecoins via clean Web2 APIs.

By leveraging Stripe and Bridge, Meta gains immediate access to battle-tested, highly compliant fiat-to-crypto on-ramps and off-ramps. Stripe assumes the regulatory liability, the Know Your Customer (KYC) overhead, and the technical heavy lifting of smart contract management. Meta, in turn, retains total control over the User Experience (UX) and the monetization of the payment flow. This vendor-client relationship is the cornerstone of Meta’s new "arm's length" playbook.

Part 2: The Ghost of Libra Past – Anatomy of a Failed Revolution

To truly appreciate the brilliance and stealth of Meta's current strategy, macro traders must conduct a post-mortem on one of the most spectacular corporate failures in Silicon Valley history: Project Libra. Why did it fail so spectacularly, and why is this time structurally different?

The Hubris of the Original Design (2019)

Announced in June 2019 under the leadership of David Marcus, Libra was breathtaking in its ambition. Mark Zuckerberg did not just want to build a PayPal competitor; he attempted to engineer a supranational synthetic currency.

The original Libra token was designed to be backed by a basket of global fiat currencies (USD, EUR, JPY, GBP) and short-term government securities. This architectural design was perceived by global regulators not as a fintech innovation, but as a direct, existential threat to the monetary sovereignty of nation-states.

By creating a currency basket, Meta was effectively attempting to privatize the International Monetary Fund’s (IMF) Special Drawing Rights (SDRs). Central banks, from the U.S. Federal Reserve to the European Central Bank (ECB) and the People's Bank of China (PBOC), instantly realized that a privately controlled currency distributed instantly to 2.5 billion users could fatally disrupt their ability to control the M1 and M2 money supply, execute monetary policy, and manage domestic inflation.

The Regulatory Hammer and Reputational Baggage

The timing of Libra could not have been worse. Meta was still heavily engulfed in the toxic fallout of the Cambridge Analytica data privacy scandal, facing accusations of interfering in democratic elections.

When Zuckerberg was summoned to Capitol Hill, the U.S. Congress, led by figures like Representative Maxine Waters, was highly combative. The underlying message from lawmakers was unyielding: A technology conglomerate that cannot be trusted to protect user data and safeguard democratic processes absolutely cannot be trusted to manage the global financial system. Operation Chokepoint 2.0 began to take root, with regulators leaning heavily on Meta's initial partners (Visa, Mastercard, Stripe, PayPal) to abandon the Libra Association. One by one, terrified of regulatory reprisal, the partners defected.

The Pivot to Diem and the Ultimate Demise (2020 - 2022)

Under crushing regulatory pressure, the Libra Association rebranded to the Diem Association in late 2020. They drastically scaled back their ambitions, entirely abandoning the multi-currency basket in favor of single-currency stablecoins (e.g., a Diem USD).

Despite this massive concession, the regulatory agencies maintained a shadow blockade. Realizing that the U.S. government would never permit a Facebook-branded stablecoin to see the light of day, Meta capitulated. In early 2022, the project was officially shut down, and the intellectual property and assets were sold to Silvergate Capital for a mere $200 million.

The lesson Meta learned was written in blood: Do not attempt to usurp the U.S. Dollar, do not attempt to be the central bank, and do not attempt to be the issuer of the money. Meta’s 2026 approach—outsourcing the stablecoin entirely to Stripe—is a direct, highly calculated response to the political trauma of 2019.

Part 3: The Strategic Imperative – Why is Meta Returning to the Arena Now?

Given the severe bruising Meta took during the Libra saga, why would Mark Zuckerberg willingly step back into the highly scrutinized stablecoin arena in 2026? The answer lies in a confluence of massive macroeconomic shifts, competitive existential threats, and the evolving limits of the advertising business model.

1. The Super-App Arms Race and the Threat of WeChatification

The era of the pure "Attention Economy"—monetizing user eyeballs purely through highly targeted advertising—is reaching terminal velocity. Apple's App Tracking Transparency (ATT) framework severely handicapped Meta’s ability to track users across third-party apps, permanently impacting its ad-targeting efficiency.

The new frontier for Silicon Valley is the "Transaction Economy." Tech giants are racing to build the Western equivalent of Tencent's WeChat—a singular "Super-App" where users communicate, consume media, hail rides, and, crucially, conduct all of their financial lives. Meta is currently facing severe, existential threats on two distinct fronts:

Elon Musk’s X (formerly Twitter): Musk has explicitly stated his intention to transform X into a financial behemoth. By 2025, X had secured money transmitter licenses across nearly all 50 U.S. states. X is aggressively moving toward in-app peer-to-peer (P2P) payments and creator monetization, threatening to siphon high-value user engagement and financial flow away from Instagram and Threads.

Telegram and the TON Network: Pavel Durov’s Telegram, boasting nearly a billion users, has deeply integrated the TON (The Open Network) blockchain. Telegram users can already seamlessly send USDT to each other within the chat interface, buy mini-app subscriptions, and engage in decentralized commerce. Telegram has proven to the world that chat-based crypto payments are not just viable; they are explosive.

If Meta does not integrate native, frictionless payments into WhatsApp and Messenger, it risks being relegated to a legacy social media platform, while its competitors evolve into sovereign global digital economies.

2. Monetizing the Global Remittance Corridor via WhatsApp

WhatsApp is the undisputed king of global messaging, particularly in emerging markets across Latin America, Africa, and Southeast Asia (most notably India, Brazil, and Mexico). However, Meta has historically struggled to monetize this massive user base effectively without ruining the UX with invasive display ads.

The global cross-border payments and remittance market is valued at over $800 billion annually. Currently, migrant workers send money home using legacy rails like Western Union, MoneyGram, or the SWIFT banking network. They suffer average fees of 5% to 7% and multi-day settlement delays.

By integrating a third-party stablecoin via Stripe, Meta can instantly capture this market. A user in Texas could seamlessly purchase USDC or a Stripe-issued stablecoin via their bank account, and send it instantly via a WhatsApp message to a family member in Mexico or Nigeria for fractions of a cent.

The Monetization Model: Meta doesn't need to charge the retail user a 5% fee to send the money. They can monetize the float, charge micro-fees to merchants (Merchant Discount Rates), or simply benefit from the massive increase in "social commerce." As users begin buying goods from local businesses directly inside WhatsApp shops, Meta captures the entire commercial loop.

3. The "Dollar Milkshake Theory" Accelerated

From a macroeconomic perspective, Meta’s integration of stablecoins accelerates the "Dollar Milkshake Theory." In emerging markets suffering from high local currency inflation, citizens are desperate for U.S. Dollar exposure. By putting a digital dollar wallet into the hands of 3 billion people via WhatsApp, Meta essentially acts as a massive vacuum, sucking local currency liquidity globally and converting it into synthetic USD demand. This aligns perfectly with U.S. geopolitical interests—exporting the Dollar's hegemony digitally without relying on traditional banking infrastructure.

Part 4: The 2026 Stablecoin Landscape – An Oligopoly Ripe for Disruption

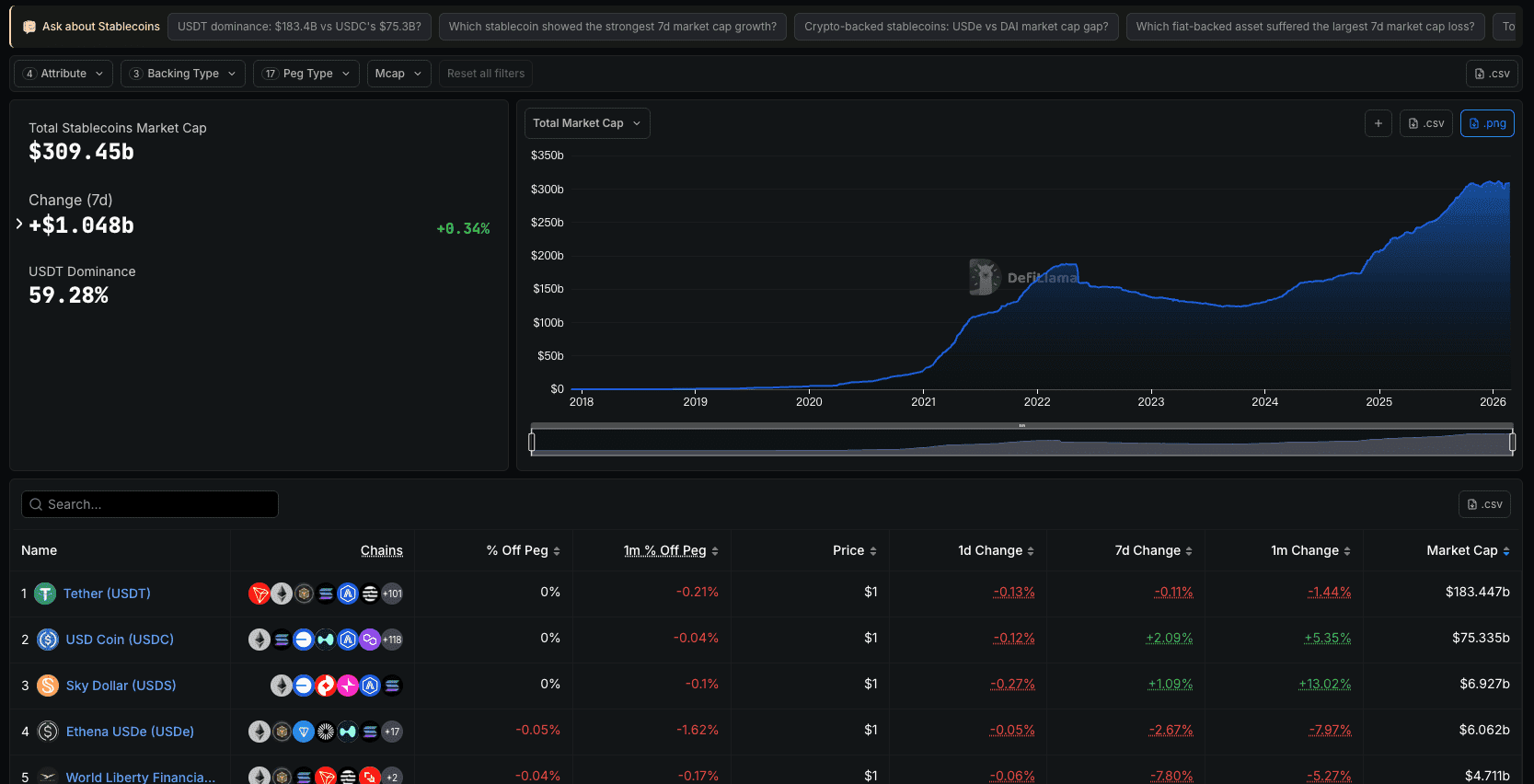

To understand the immense impact of Meta's entry, traders must rigorously analyze the current state of the stablecoin market. As provided by real-time DefiLlama data (February 2026), the global stablecoin market capitalization has swelled to an astonishing $309.45 billion. It is the undisputed lifeblood of the global crypto-economy. However, it is fundamentally an oligopoly.

Analyzing the $309.45 Billion Market Cap Data

1. The Undisputed King: Tether (USDT)

Market Cap: $183.447 Billion

Market Dominance: 59.28%

Tether remains the offshore behemoth. It commands the vast majority of the sector, dominating trading pairs on centralized exchanges (Binance, OKX) and acting as the primary synthetic dollar in emerging markets, heavily utilizing the Tron network for cheap transfers. However, Tether remains largely outside the U.S. regulatory perimeter. Due to its opaque banking relationships and offshore nature, it is highly unlikely that a highly scrutinized, U.S.-domiciled public company like Meta would select USDT as its primary integration partner.

2. The Compliant Challenger: USD Coin (USDC)

- Market Cap: $75.335 Billion (Showing strong 1-month growth of +5.35%)

Circle’s USDC is the darling of U.S. institutions and Decentralized Finance (DeFi). Circle has positioned itself as the compliant, transparent, fully-reserved alternative to Tether, actively courting U.S. lawmakers. If Stripe does not issue its own proprietary stablecoin for Meta, USDC is the overwhelming favorite to serve as the underlying asset for WhatsApp payments, given Stripe's existing deep integration with Circle.

3. The Emerging Yield-Bearing Competitors

The data also highlights the rise of next-generation stablecoins:

Sky Dollar (USDS): $6.927 Billion.

Ethena USDe: $6.062 Billion. Ethena represents the "crypto-native" synthetic dollar, utilizing basis trades (shorting perpetual futures while holding spot) to generate high yields.

World Liberty Financial USD (USD1): $4.711 Billion.

While these yield-bearing assets are incredibly popular among crypto-natives, Meta will almost certainly avoid utilizing them directly as a medium of exchange. Meta requires a pure, non-volatile, 1:1 fiat-backed instrument. Using a synthetic like USDe introduces smart contract risk and algorithmic de-pegging risk that Meta’s legal team will never underwrite for 3 billion retail users. However, the concept of yield is currently tearing the regulatory landscape apart.

Part 5: The Regulatory Renaissance – Global Synchronization and the Yield War

The most critical variable allowing Meta’s 2026 return is the radical transformation of the global regulatory landscape. The extreme hostility of 2019 has been replaced by legislative clarity across both sides of the Atlantic. However, a new, massive battleground has emerged regarding stablecoin yield.

1. The U.S. GENIUS Act (2025) and The Legal Foundation

Passed in 2025, the GENIUS Act fundamentally restructured the U.S. approach to digital assets. For the first time in U.S. history, clear, unambiguous legal frameworks were established for U.S. stablecoin issuers.

Definitive Classification: The Act explicitly defined fiat-pegged stablecoins as payment instruments rather than securities. This permanently removed them from the SEC's hostile purview.

Reserve Requirements: It established strict, transparent guidelines requiring issuers to back tokens 1:1 with highly liquid assets (cash, short-duration U.S. Treasuries) subject to monthly audits.

State vs. Federal Chartering: Allowed fintech firms (like Stripe or Circle) to operate under specialized state-level trust charters, bypassing the requirement to become fully chartered national banks.

This legislative clarity de-risked the integration of stablecoins for mega-cap tech companies. It signaled to Meta’s legal department that as long as they partner with a vendor that adheres strictly to the collateral transparency laws, the existential regulatory risk that killed Diem is neutralized.

2. The Global Sandbox: UK FCA Opens the Doors (Feb 2026)

The regulatory thaw is not isolated to the U.S. On February 25, 2026, the UK's Financial Conduct Authority (FCA) announced a monumental step forward, officially selecting four entities—Monee Financial Technologies, ReStabilise, Revolut, and VVTX—to test stablecoin innovation within its Regulatory Sandbox.

This sandbox allows these firms to trial stablecoin products in real-world conditions (spanning payments, wholesale settlement, and crypto trading) with appropriate safeguards. As Matthew Long, FCA director of payments and digital assets, explicitly stated: "We are supporting UK stablecoin issuers to ensure they can be trusted for payments, settlement and trading... to deliver the FCA's strategy and the Government's National Payments Vision."

With testing commencing in Q1 2026, the FCA is utilizing these findings to shape the final UK stablecoin rules later this year, leading up to a fully live authorization regime in October 2027. For a multinational conglomerate like Meta, this synchronized regulatory clarity across the US and the UK provides the global legal runway necessary to deploy WhatsApp payments internationally without facing fragmented, hostile jurisdictions.

3. The $1.3 Trillion Crisis: The Battle Over Stablecoin Yield

While the GENIUS Act provided baseline clarity on issuance, it ignited a fierce new battleground that dominated Capitol Hill in late February 2026: Stablecoin Yield and Deposit Flight.

The 2025 GENIUS Act strictly prohibited stablecoin issuers (like Circle) from paying direct interest to token holders. However, it left a massive, controversial loophole: it did not prohibit third-party platforms (like Coinbase, or potentially a Meta/Stripe wallet interface) from offering yield rewards to users holding those stablecoins.

In highly contentious Senate Banking Committee hearings this month, lawmakers clashed over this exact mechanism. Senator Angela Alsobrooks led the charge, warning that yield-bearing stablecoin mechanisms create products practically indistinguishable from traditional bank deposits, yet they completely lack FDIC insurance and consumer protections, posing a severe systemic risk. Senator Thom Tillis echoed these concerns, formally demanding that regulators conduct an independent assessment of the deposit flight risks triggered by stablecoins.

The panic from traditional finance is palpable and mathematically quantified. The Independent Community Bankers of America released a devastating research report projecting that if stablecoin yield mechanisms are fully unleashed across platforms like Meta, the traditional banking sector could suffer a catastrophic $1.3 trillion drain in retail deposits. Furthermore, this loss of deposits would result in an estimated $850 billion contraction in community bank lending, strangling local businesses.

Conversely, the crypto industry argues that restricting yield stifles innovation and that no empirical evidence currently links stablecoin adoption directly to immediate bank deposit flight. The stakes are so high that the White House has organized emergency multi-round meetings between banking executives and crypto firms throughout February 2026, desperately hoping to broker a solution by the end of the month.

For Meta, this yield debate is the ultimate wedge issue. If Meta and Stripe can legally figure out a way to pass treasury yield back to 3 billion WhatsApp users, traditional checking accounts will become obsolete overnight.

Part 6: Market Perspectives – The Wall Street, Silicon Valley, and Web3 Consensus

The leaked news of Meta's stablecoin ambitions has fractured market sentiment into three distinct, highly vocal camps: The TradFi bears, the Silicon Valley bulls, and the Web3 purists.

1. The TradFi View: The Panic of Complete Disintermediation

For traditional legacy banking institutions, remittance providers, and global payment processors (Visa, Mastercard), Meta’s entry—combined with the Senate Banking Committee's $1.3 trillion deposit flight fears—is a worst-case, "extinction-level" scenario.

Wall Street analysts view this as the ultimate realization of disintermediation. If 3 billion users can instantly settle payments with finality using a blockchain-backed stablecoin inside WhatsApp, the necessity for the SWIFT network, corresponding banking fees, and exorbitant merchant acquirer rates evaporates.

If consumers begin holding large balances of synthetic dollars inside a Meta-Stripe wallet because it offers frictionless spending (and potentially backend yield), capital will permanently migrate away from traditional checking accounts. Bank stocks with heavy reliance on retail transaction fees and sticky retail deposits are likely to face severe, structural headwinds.

2. The Silicon Valley Bull Case: The Dawn of True Social Commerce

Technology maximalists and equity analysts covering Meta ($META) view this as a massive, fundamentally bullish catalyst. For years, Meta has struggled to close the loop on "Social Commerce." Users see an ad on Instagram, click it, and are redirected to a clunky external Shopify web browser to input their credit card details. The drop-off rate is massive.

By integrating a native stablecoin wallet via Stripe, Meta achieves "one-click checkout" natively within the social feed. The friction of the transaction drops to near zero. Conversion rates for advertisers will skyrocket, allowing Meta to command significantly higher premiums for its ad inventory. Furthermore, by owning the payment rails, Meta can potentially capture a fraction of a cent on billions of micro-transactions daily, expanding its Average Revenue Per User (ARPU) exponentially.

3. The Web3 Purist Perspective: Walled Gardens vs. Open Networks

Within the crypto-native ecosystem, the reaction is deeply polarized.

The Pragmatists: Recognize that Meta’s integration is the ultimate Trojan Horse for Web3 mass adoption. Even if the front-end is highly centralized and permissioned, the back-end will utilize public blockchains. This brings hundreds of millions of new users into the digital asset ecosystem, vastly increasing total network liquidity and familiarizing the masses with digital wallets.

The Purists (The Bear Case): Express profound skepticism. They view Meta’s stablecoin as the ultimate realization of Corporate Surveillance Capitalism. There are fears that Meta will create a "walled garden"—a closed-loop system where the stablecoin can only be spent within the Meta ecosystem, completely cut off from permissionless DeFi protocols like Uniswap or Aave. Furthermore, given Meta's history of data harvesting, crypto-anarchists fear that Meta will analyze blockchain transaction graphs to hyper-target financial advertising, fundamentally compromising user privacy.

Part 7: Actionable Trading Implications & Alpha Generation

For the institutional trader and macro allocator, the leaked Meta RFP represents a highly actionable narrative. This is not a distant 10-year metaverse projection; this is a tangible payment rail integration slated for H2 2026. Capital flows will preempt the official launch. Here is the tactical playbook:

Trade Vector 1: The Infrastructure Proxy (Stripe, Bridge, and the Underlying L1s)

Because Stripe remains a private company, retail cannot trade it directly. However, institutional allocators in secondary private markets should view Stripe equity at a heavy premium.

For liquid crypto traders, the true alpha lies in anticipating which public blockchains Stripe and Meta will utilize for settlement.

High-Throughput L1s (Solana - $SOL): Solana is a prime candidate. Stripe has already demonstrated a strong affinity for Solana due to its sub-cent fees and rapid finality, having integrated it heavily into their fiat-to-crypto products. A Meta-Stripe integration that utilizes Solana as a primary settlement layer would be a generational catalyst for $SOL, driving institutional validation and massive on-chain metric growth.

Ethereum L2s (Base): Coinbase’s Base network is another highly probable candidate. Given the existing corporate relationships between Silicon Valley giants and Base's explosive growth in consumer-facing dApps, settling WhatsApp micro-transactions on Base would solidify its position as the premier L2, benefiting the broader Ethereum ($ETH) ecosystem via sequencer fees.

Trade Vector 2: The Stablecoin Issuer Wars ($USDC vs. $USDT)

Referencing the $309B market data, if Meta selects an existing stablecoin rather than having Stripe issue a bespoke “Meta-Dollar,” Circle (USDC) is the overwhelming favorite due to its regulatory compliance.

Traders should aggressively monitor Circle's impending IPO or equity valuation.

Conversely, if Meta launches a massively successful US-compliant stablecoin via WhatsApp, it poses the first genuine, existential threat to Tether's ($USDT) 59.28% market dominance. If users in Argentina can seamlessly use a compliant Meta/Stripe stablecoin, their reliance on offshore, opaque USDT via platforms like Binance P2P will likely wane. Pair Trade: Long USDC ecosystem metrics, Short USDT dominance.

Trade Vector 3: Short TradFi Banks and Legacy Payment Processors

In the traditional equities market, the Meta stablecoin integration should be viewed as a structural short thesis on two fronts:

Legacy Remittance: Western Union ($WU) and MoneyGram. As Meta rolls out feeless, instant stablecoin remittances globally, the legacy business models of these firms face imminent, unrecoverable margin compression.

Regional Banks (KRE): Given the Senate Banking Committee's highlighted fears of a $1.3 trillion deposit drain and an $850 billion contraction in loans if stablecoin yield platforms proliferate, regional banks are highly vulnerable. If Meta integrates yield mechanics into WhatsApp, retail deposits will flee traditional community banks at an unprecedented velocity.

Trade Vector 4: Meta Equity ($META)

From an equities perspective, a successful stablecoin integration effectively transforms Meta from a pure-play advertising company into a globally systemic financial infrastructure provider. By successfully executing the "Super-App" transition, Meta commands a massive multiple expansion. The integration diversifies revenue away from cyclical ad-spend, opening up a multi-billion dollar Total Addressable Market in fintech, P2P lending, and creator economy monetization.

Conclusion: The Dawn of Corporate Digital Liquidity

The news of Mark Zuckerberg's planned return to the stablecoin space in the second half of 2026 is not merely a tech headline; it is a macroeconomic earthquake.

The scars of the Libra/Diem failure have forged a more cunning, politically savvy Meta. By abandoning the hubris of issuing a sovereign synthetic currency, and instead opting to become the ultimate consumer-facing distribution network via third-party vendors like Stripe, Meta is executing a masterclass in regulatory arbitrage.

Buoyed by the legislative clarity of the U.S. GENIUS Act and the synchronized global regulatory thaw seen in the UK FCA's Sandbox initiatives, Meta is poised to introduce frictionless, dollar-backed digital cash to 3 billion people. Driven by the existential necessity of competing in the Super-App wars, Meta is perfectly positioned to exploit the ongoing congressional battle over the $1.3 trillion stablecoin yield deposit flight.

Colliding with a stablecoin market already worth $309.45 billion, Meta's entry will act as pouring gasoline on a raging fire. For the professional trader and institutional allocator, the implications are staggering. We are witnessing the fusion of global social networks with blockchain settlement rails. The winner of this race will not just control the world's attention; they will control the velocity of the world's money. The Leviathan has awakened, and global financial infrastructure will never be the same.