Key Takeaways

Superstate is a regulated tokenization company focused on bringing funds and equities onchain, rather than a typical DeFi protocol or exchange. Its official site says it connects financial assets with crypto capital markets through tokenized investment products and onchain public listings.

Superstate’s best-known products are USTB and USCC. USTB gives qualified purchasers access to short-duration U.S. Treasury bills, while USCC gives qualified purchasers access to crypto basis strategies plus U.S. Treasuries.

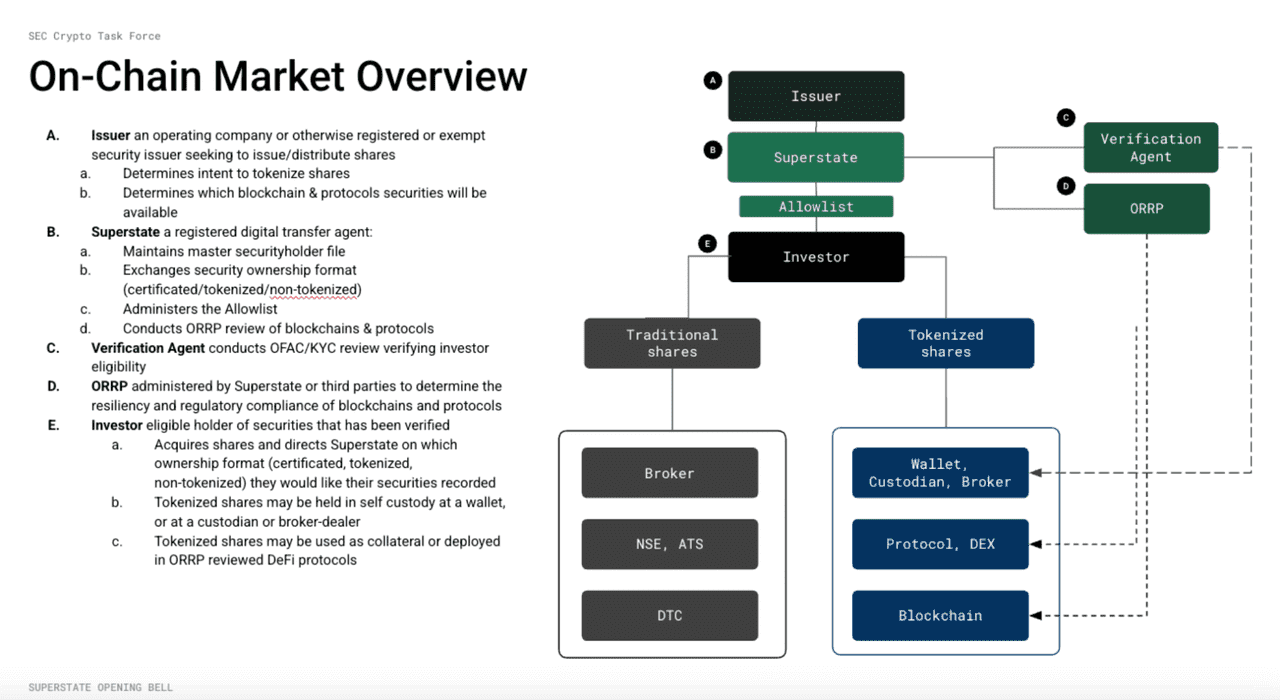

Ownership in Superstate funds can be represented either as a token or in book-entry form, which shows how the firm is trying to bridge traditional fund structures with blockchain rails.

Superstate is also expanding beyond funds into on-chain equities infrastructure. Its investor platform says users can hold onchain equities, and SEC materials and issuer filings show Superstate Services LLC acting as a digital transfer agent or co-transfer agent for tokenized stock initiatives.

The core idea behind Superstate is simple: move familiar financial assets like Treasury funds and stocks onto blockchain-based rails so they can gain better interoperability with crypto markets, potentially including 24/7 access, faster transfer, and DeFi compatibility.

Superstate is one of the clearest examples of how crypto’s tokenization trend is moving beyond theory and into regulated financial products. Instead of building a new Layer 1, a memecoin ecosystem, or a purely crypto-native DeFi app, Superstate is focused on something more specific: bringing traditional financial assets onchain in a way that can still fit inside recognizable legal and market structures.

That distinction matters. A lot of tokenization projects talk broadly about “real-world assets,” but Superstate’s pitch is more concrete. Its homepage says it wants to “move funds and stocks onchain,” and describes its platform as connecting securities with crypto capital markets for global 24/7 access and DeFi use cases. That means Superstate is not just selling a token narrative. It is trying to build infrastructure that sits between traditional securities law, fund structures, transfer agency, and blockchain rails.

So if you are asking what Superstate is, the short answer is this: Superstate is a regulated tokenization platform that helps bring investment funds and equities onto blockchain infrastructure.

What Superstate Actually Does

Superstate’s business model is built around tokenized financial products and tokenization infrastructure. Its official “About” page says the company connects financial assets with crypto capital markets to expand access, improve liquidity, and advance capital formation through onchain public listings and tokenized investment products. That means Superstate is playing two roles at once.

First, it operates tokenized funds, where investors can gain exposure to familiar assets like U.S. Treasury bills or crypto basis strategies through regulated fund structures whose ownership can be represented onchain. Second, it is building infrastructure for tokenized securities, especially through its digital transfer-agent capability and its platform for issuers and investors.

This makes Superstate different from a typical DeFi RWA protocol. Many RWA protocols tokenize claims in a more crypto-native format, but Superstate is trying to work directly with the institutional and legal machinery of funds and securities. That makes it especially relevant to the bigger discussion around whether blockchain can become part of mainstream capital markets rather than just parallel crypto markets.

Superstate’s Two Main Funds: USTB and USCC

The easiest way to understand Superstate is by looking at its products.

USTB

Superstate’s Short Duration US Government Securities Fund, represented by USTB, offers qualified purchasers access to short-duration Treasury bills. The fund says its objective is current income with liquidity and stability of principal, targeting returns in line with the federal funds rate. Ownership in the fund is recognized by USTB and can be held either as a token or in book-entry form.

That is important because it shows how Superstate is approaching tokenization: not as a replacement for traditional fund economics, but as a new wrapper and transfer rail for a familiar underlying exposure. USTB is not trying to reinvent Treasury-bill investing. It is trying to make a Treasury fund more interoperable with blockchain infrastructure.

USCC

Superstate’s Crypto Carry Fund, represented by USCC, offers qualified purchasers access to crypto basis strategies across multiple cryptocurrencies and U.S. Treasury securities. The fund says it optimizes the yield and risk of crypto cash-and-carry trades, and subscriptions and redemptions can be facilitated through either USD or USDC, with liquidity each market day. Ownership, like USTB, can be recognized through a token or in book-entry form.

USCC is especially interesting because it shows that Superstate is not limited to tokenizing low-risk cash-like instruments. It is also trying to bridge more crypto-native return strategies with regulated fund structures and onchain representation. In other words, USTB and USCC together show two sides of Superstate’s thesis: tokenized traditional yield and tokenized crypto-market strategy access.

Why Superstate Matters in the Tokenization Trend

Superstate matters because it sits at the intersection of several major themes in crypto and finance. The first is real-world assets. Tokenized Treasuries have become one of the clearest product-market fits in the RWA sector, because they combine familiar yield with blockchain-based transferability. USTB fits directly into that category.

The second is regulated onchain finance. Superstate is not building around anonymous, permissionless participation for every product. Its fund pages repeatedly refer to qualified purchasers, showing that the company is deliberately operating within traditional investor-qualification frameworks rather than pretending regulation does not exist.

The third is capital-markets infrastructure. Superstate’s broader platform is not just about funds. Its investor page says users can add Ethereum, Solana, or Plume wallet addresses to an allowlist and securely hold onchain equities, with both custodial and non-custodial wallets supported. That tells you Superstate’s long-term goal is larger than one or two tokenized funds. It is trying to build a real bridge between crypto wallets and conventional securities ownership.

Superstate and Onchain Equities

Superstate’s investor platform says users can hold on-chain equities, not just tokenized funds. The same page presents FundOS and broader investor tooling as part of a platform for tokenized private funds, ETFs, and equities.

That ambition is reinforced by SEC materials and public company filings. An SEC roundtable page from April 2026 describes Superstate’s general counsel as helping develop one of the first SEC-registered transfer agents purpose-built for digital assets, as well as multiple tokenized security funds with more than $700 million in AUM.

Meanwhile, several SEC filings from public issuers show Superstate Services LLC acting as a digital transfer agent or co-transfer agent for efforts to tokenize common stock on blockchains such as Ethereum and Solana. For example, Forward Industries disclosed that Superstate was engaged as co-transfer agent to allow shareholders to tokenize holdings on Solana, and other filings describe similar intentions around Ethereum-based tokenized stock.

This is a major clue about what Superstate may become. It is not just a tokenized-fund issuer. It may also become part of the recordkeeping and transfer infrastructure for blockchain-based securities markets.

How Superstate Differs From a Typical Crypto Protocol

Calling Superstate a “protocol” can be a little misleading if someone is expecting something like Uniswap, Aave, or Maker.

Superstate is much closer to a regulated financial company using blockchain rails than to a purely decentralized protocol. Its 2023 financing announcement states that Superstate Advisers LLC is a registered investment adviser, and that Superstate Services LLC is a registered transfer agent with the SEC.

That makes Superstate fundamentally different from tokenization projects that rely mostly on smart contracts and DAOs. Superstate is operating inside the legal architecture of traditional finance and trying to extend that structure onto blockchain infrastructure. This is a feature, not a bug, because institutional tokenization usually depends on exactly that kind of legal and compliance foundation.

What Problem Superstate Is Trying to Solve

At a high level, Superstate is trying to solve the gap between traditional securities systems and crypto capital markets.

Traditional funds and equities are usually confined to brokerage accounts, transfer agents, custodians, and conventional settlement rails. Crypto assets, by contrast, move across wallets, blockchains, exchanges, and DeFi protocols with much greater programmability and 24/7 transferability. Superstate’s entire business is built around the idea that these two worlds should not remain separate forever.

By making ownership recognizable either in token form or book-entry form, Superstate is trying to create a bridge where regulated financial products can live closer to the environment where digital capital already moves. That could matter for:

faster transfer and settlement,

broader wallet-based access,

more seamless integration with tokenized collateral or DeFi use cases,

and a larger investor base that thinks in blockchain-native rather than brokerage-native terms.

In short, Superstate is trying to make securities more compatible with the infrastructure of crypto.

The Bull Case for Superstate

The bullish case for Superstate is strong because it is aligned with several durable market trends.

First, tokenized Treasuries and tokenized cash-like products have already become one of the most credible sectors in the RWA market. USTB fits neatly into that growing demand.

Second, Superstate has expanded beyond funds into equities tokenization infrastructure, which is potentially an even larger market if public and private securities gradually move onchain. The SEC roundtable description and issuer filings suggest the company is already involved in that direction.

Third, Superstate appears to be positioned as a compliance-first bridge between traditional finance and crypto, which may be exactly what institutional tokenization needs. In a space where many projects overemphasize decentralization without solving the legal layer, Superstate’s regulated structure may be an advantage rather than a constraint.

Fourth, the company seems to be moving into a broader ecosystem role through products, platform infrastructure, and transfer-agent services. That makes it more than a one-product story.

The Risks and Limitations

Superstate also faces real limits. The first is that tokenization is still early. Even if the long-term thesis is strong, the speed of adoption for tokenized securities and tokenized funds may be slower than crypto investors hope. Regulated financial infrastructure usually moves gradually, not overnight.

The second is that Superstate’s fund products, at least as described publicly, are not open to everyone. USTB and USCC are currently pitched to qualified purchasers, which means the addressable user base is narrower than a fully open crypto product.

The third is that blockchain-based securities still need strong answers around custody, transfer restrictions, investor protection, legal finality, and market interoperability. Superstate appears to be working directly on those issues, but the broader market structure is still evolving.

The fourth is competition. Superstate is not the only company pursuing tokenized funds, tokenized Treasuries, or digital securities infrastructure. Its success will depend on execution, regulatory positioning, and whether its platform becomes a preferred bridge for issuers and investors. This point is an inference from the broader tokenization sector, but it follows directly from the market it is entering.

What Is Superstate in One Sentence

Superstate is a regulated tokenization company that brings funds and equities onchain, using blockchain infrastructure to connect traditional securities with crypto capital markets.

That is the cleanest summary because it captures both sides of the business: tokenized investment products like USTB and USCC, and broader onchain securities infrastructure through its platform and transfer-agent work.

Conclusion

Superstate is one of the most important companies to watch in the tokenization space because it is not just talking about putting assets onchain. It is actively building the legal, operational, and product infrastructure to do it in a regulated form. Its current offerings include tokenized fund exposure through USTB and USCC, and its broader platform points toward a larger future involving onchain equities and tokenized capital-markets infrastructure.

That makes Superstate more than a trend-driven RWA name. It is a serious attempt to bridge traditional finance and crypto at the level where it matters most: ownership, transfer, settlement, and investor access.

The open question is not whether Superstate is real. It clearly is. The open question is how big the market for onchain regulated securities becomes, and whether Superstate can become one of the core rails that market ends up using.