Key Takeaways

RWA 2.0 generally refers to the next phase of real-world asset tokenization, where tokenized assets become active building blocks for onchain finance rather than passive wrappers.

The first wave of RWAs focused heavily on proof of concept and simple tokenized products like Treasuries and basic yield wrappers. The next wave is increasingly about collateral, settlement, origination, and interoperability.

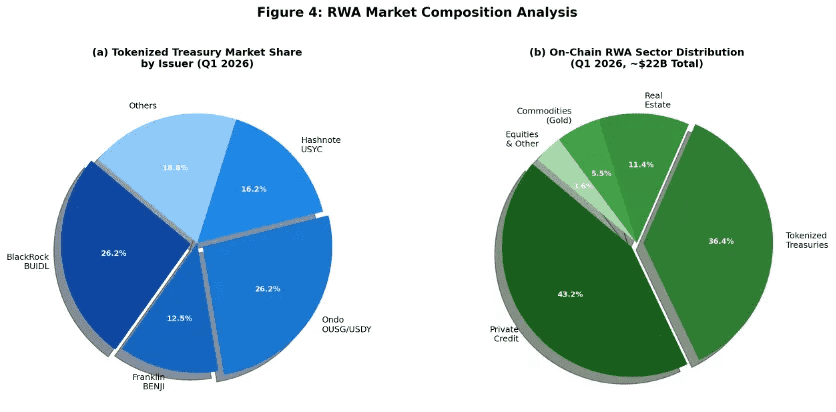

Current market data from RWA.xyz shows that tokenized RWAs have grown to a meaningful scale, with $26.71B distributed asset value and $345.07B represented asset value at the time of the fetched snapshot.

RWA 2.0 is especially visible in trends such as tokenized collateral frameworks, tokenized cash for margin systems, tokenized credit, and tokenized securities settlement.

The biggest promise is more efficient capital markets; the biggest challenge is still legal structure, interoperability, and real market adoption.

Real-world asset tokenization has already moved beyond the “can this be done?” phase. The market is now asking a harder question: what comes after the first wave of tokenized Treasuries and simple onchain wrappers? That next phase is often described as RWA 2.0.

While there is no single official definition used by every company, current industry signals point to a common idea: RWA 2.0 is the stage where tokenized assets stop being passive blockchain representations and start becoming active components of onchain finance. Instead of only putting a real-world asset onchain, RWA 2.0 focuses on how that asset can be used for collateral, settlement, liquidity, credit, portfolio construction, and broader financial coordination. This shift is visible in institutional tokenized-collateral frameworks, tokenized-cash platforms for margin, and broader industry writing that emphasizes origination, payment integration, and market structure—not just tokenization by itself.

That matters because the first wave of RWA adoption was mostly about proving the concept. The second wave is about turning tokenized assets into working financial infrastructure.

What Does RWA 2.0 Actually Mean?

RWA 2.0 is best understood as a market-structure upgrade, not just a marketing slogan.

The first generation of RWAs was largely about demonstrating that real-world assets could be represented onchain at all. That included tokenized Treasury products, tokenized money-market exposure, tokenized gold, and other early wrappers. Those products mattered because they showed that blockchain could represent claims on offchain assets in a credible way. But many of them were still relatively passive: hold the token, receive the yield, and maybe redeem later.

RWA 2.0 pushes beyond that. In this newer phase, the question is no longer only, “Can we tokenize this asset?” The question becomes:

Can this tokenized asset be posted as collateral?

Can it settle trades faster?

Can it plug into DeFi or institutional margin systems?

Can it support new origination models?

Can it move across venues and chains without losing legal clarity?

This interpretation is strongly supported by current industry developments. A16z crypto’s May 2026 trends piece explicitly says the industry will see more origination, not just tokenization, especially around stablecoins and finance. Its March 2026 piece on Wall Street moving onchain frames tokenization as transforming capital markets through faster settlement, lower costs, and 24/7 global access. Centrifuge’s current positioning also emphasizes infrastructure for onchain asset management, not just issuance.

RWA 2.0 is the phase where tokenized assets become integrated financial primitives, not just digital wrappers of offchain assets.

Why the First Wave of RWAs Was Not Enough

The first wave of RWA growth was necessary, but limited.

Early tokenized assets did several important things well:

proved that regulated or structured real-world claims could exist on public blockchains,

attracted institutional attention,

and introduced crypto users to offchain yield.

But they also had clear limitations.

Many early RWA products were essentially static wrappers. They gave exposure to an asset, but often did not do much beyond that. They were more like tokenized certificates than living financial infrastructure. In many cases, liquidity was thin, composability was limited, and the tokenized asset did not yet interact deeply with broader onchain or institutional systems. This is an inference from the sector’s evolution, but it is consistent with how recent institutional commentary now emphasizes settlement, collateral, and operational integration rather than mere representation.

That is why the market is moving toward a more useful second phase. If tokenization only creates a prettier wrapper, it is interesting. If tokenization improves how collateral moves, how capital is deployed, and how markets settle, it becomes transformative.

The Core Characteristics of RWA 2.0

While different firms describe the trend differently, RWA 2.0 usually includes some combination of five main features.

Financial Utility, Not Just Representation

In RWA 2.0, the tokenized asset is expected to do something.

It may still represent a Treasury bill, a security, or a credit product, but it is increasingly expected to function as collateral, margin, cash-equivalent settlement value, or an ingredient in broader portfolio infrastructure. This is one reason recent institutional announcements matter so much: they show tokenized assets being used in actual workflows, not just issued and held.

Integration With Onchain Finance

Centrifuge’s current positioning is a useful example here. It does not simply market tokenization; it markets infrastructure for onchain asset management, access to institutional-grade RWAs from preferred chains or currencies, and transparent settlement and reporting. That is a much more integrated vision than a basic one-token wrapper.

Better Collateral and Capital Efficiency

One of the biggest themes in 2026 is that tokenized assets are increasingly being discussed as collateral, not just investments. This is arguably one of the clearest markers of RWA 2.0. When a tokenized Treasury or other RWA can be posted into a trading, financing, or margin framework, the token stops being passive and starts becoming capital-efficient. The Reuters-covered institutional collateral framework and broader Wall Street onchain movement are key signals here.

Faster Settlement and Market Infrastructure

A16z crypto’s March 2026 “Why Wall Street is moving onchain” piece is especially relevant. It frames tokenization not as a novelty but as a way to improve capital markets through faster settlement, lower operational costs, and 24/7 access. Those are not wrapper benefits; they are infrastructure benefits.

Origination and New Financial Products

A16z crypto’s May 2026 trends article says the market will see more origination, not just tokenization. That is an especially important clue for understanding RWA 2.0. The next stage is not only about taking existing assets and putting them onchain. It is also about issuing new products natively designed for an onchain financial system.

RWA 2.0 vs RWA 1.0

A useful way to think about the difference is this:

RWA 1.0

tokenize the asset

prove legal structure

offer exposure

maybe provide yield

mostly hold-and-redeem behavior

RWA 2.0

tokenize the asset

preserve legal clarity

make it useful as collateral

improve settlement and capital efficiency

plug it into broader onchain and institutional workflows

create new forms of issuance and market structure around it

This comparison is partly a synthesis, but it is directly supported by recent shifts in industry emphasis. The current conversation is much less about “is tokenization real?” and much more about “how does tokenization change finance once real assets are live onchain?”

Real Examples of RWA 2.0 Trends

The best way to understand RWA 2.0 is through real market examples and signals.

Tokenized Collateral Frameworks

One of the strongest examples is the recent institutional framework involving tokenized Treasury collateral. This is important because it represents a shift from tokenized assets as passive yield exposure to tokenized assets as usable margin and collateral instruments. That is a major step toward the kind of capital efficiency RWA 2.0 promises.

Tokenized Cash for Margined Products

A16z’s trend writing and institutional market developments also point toward tokenized cash and tokenized deposits being used for more continuous financial operations. This fits RWA 2.0 because cash itself becomes part of programmable market infrastructure, not just a blockchain mirror of a bank balance.

Onchain Asset Management Platforms

Centrifuge’s current brand direction is highly relevant. It describes itself as infrastructure for onchain asset management, with access to institutional-grade treasuries, credit, index products, and structured vehicles from preferred chains or currencies. That is much closer to a full financial stack than a one-off tokenized asset product.

Tokenized Stocks and Tokenized Public Markets

RWA.xyz’s commentary on Robinhood’s tokenized stocks is also helpful. It highlights technical issues like multiplier infrastructure for corporate actions and standards for how tokenized equities should actually behave onchain. This shows that the industry is already thinking beyond “tokenize a stock” toward the harder details of how tokenized public markets function as infrastructure.

Why Stablecoins Matter So Much for RWA 2.0

Stablecoins are deeply connected to RWA 2.0 because they are often the settlement layer for tokenized assets.

A16z crypto’s May 2026 trends piece is especially useful here. It argues that stablecoins are reshaping finance and that the market will see more origination, not just tokenization. This matters because tokenized RWAs need a native way to settle, move liquidity, and interface with users and institutions. Stablecoins are the most obvious candidate.

In practice, many RWA 2.0 systems will likely combine:

tokenized real-world assets,

stablecoin settlement,

collateral management,

and some form of programmable market logic.

The Role of Data and Transparency

Another major feature of RWA 2.0 is better data.

RWA.xyz positions itself as the industry-standard data platform for tokenized RWAs, used by institutions, regulators, investors, and issuers to analyze assets across public blockchains. That is important because as tokenized markets get more complex, data and transparency stop being optional. Investors need to know:

what the asset is,

how it is structured,

where it lives,

what its value is,

and how it behaves across chains and venues.

RWA 2.0 therefore is not only about better tokens. It is also about better reference data, better analytics, and more market visibility. Without that, composability can quickly turn into confusion.

Why Wall Street Cares

RWA 2.0 matters because the institutions that shape capital markets are no longer just “exploring blockchain.” They are increasingly trying to use it.

A16z crypto’s March 2026 piece says Wall Street is not merely experimenting anymore but moving onchain, and specifically ties tokenization to faster settlement, lower costs, and 24/7 global access. That is exactly the kind of institutional motive that supports RWA 2.0. The goal is not just to make tokenized products look modern; the goal is to improve how markets function.

This is also why infrastructure providers matter more than ever. RWA 2.0 is not just about issuers. It also depends on:

fund administrators,

custodians,

legal/compliance providers,

agency services,

and reference-data platforms. RWA.xyz’s provider-directory commentary from 2023 already highlighted these categories as essential tools and services for tokenization, and that remains true in 2026.

Risks and Limitations of RWA 2.0

RWA 2.0 is promising, but it is not guaranteed.

Legal and Structural Complexity

Tokenized assets still need enforceable offchain rights. A better smart contract does not replace legal structure, custody, bankruptcy remoteness, transfer restrictions, or compliance obligations. This is one reason infrastructure providers and service categories remain so important.

Interoperability Challenges

If tokenized assets are going to function as collateral and settlement instruments across many venues or chains, interoperability becomes critical. Without it, the market risks becoming a set of isolated token silos rather than a unified financial system. This is an inference, but it follows directly from the increasing emphasis on capital-market infrastructure and cross-platform utility.

Liquidity and Market Adoption

Tokenization does not automatically create liquidity. Many tokenized assets still face thin secondary markets and adoption friction. RWA 2.0 is partly an attempt to solve this by making assets more useful, but adoption still has to happen.

Overhype Risk

Because “RWA 2.0” sounds bigger and more advanced, there is a risk that projects will use the term loosely. Not every tokenized asset platform that launches a second feature is automatically part of a deeper market-structure evolution. A good test is whether the project is actually improving collateral utility, settlement design, origination, or interoperability. This is an inference based on current market trends.

Why RWA 2.0 Could Become a Major 2026 Narrative

RWA 2.0 is becoming a major 2026 narrative because it sits at the overlap of several strong trends:

Wall Street moving onchain,

stablecoins becoming more central,

tokenized collateral emerging,

and onchain asset management maturing.

The market already has enough scale to matter. RWA.xyz’s current dashboard shows tens of billions in distributed tokenized-asset value and a much larger represented-value figure. That scale gives the sector room to move from first-generation proof-of-concept products into more operational, market-structure-heavy systems.

Put simply, RWA 1.0 helped prove the sector. RWA 2.0 is about making the sector actually useful.

Conclusion

RWA 2.0 is the phase where tokenized assets stop being passive blockchain wrappers and start becoming active infrastructure for finance.

It builds on the first wave of tokenization but shifts the focus toward:

collateral utility,

faster settlement,

stablecoin-linked financial rails,

origination of new onchain products,

and broader integration with capital markets.

As tokenized collateral, tokenized cash, stablecoins, and onchain asset-management platforms continue to evolve, RWA 2.0 is becoming one of the most important narratives in crypto finance. For traders looking to stay ahead of emerging sectors—from RWAs and tokenized capital markets to AI agents, PayFi, and chain abstraction—Phemex offers a secure and user-friendly platform to explore the market, monitor new opportunities, and sharpen your trading edge.