Key Takeaways

Private credit means loans or credit exposures that are not issued or traded on public markets.

On-chain private credit brings those exposures onto blockchain infrastructure for issuance, reporting, settlement, distribution, or collateral use.

It is part of the broader RWA trend, where real-world assets such as Treasuries, funds, equity, and credit move onchain.

The category includes assets such as business loans, trade finance, real estate-backed credit, fintech receivables, structured credit, and diversified credit funds.

The biggest benefits are transparency, programmability, broader distribution, and DeFi composability, but the biggest risks are still credit risk, legal complexity, servicing risk, and limited secondary liquidity.

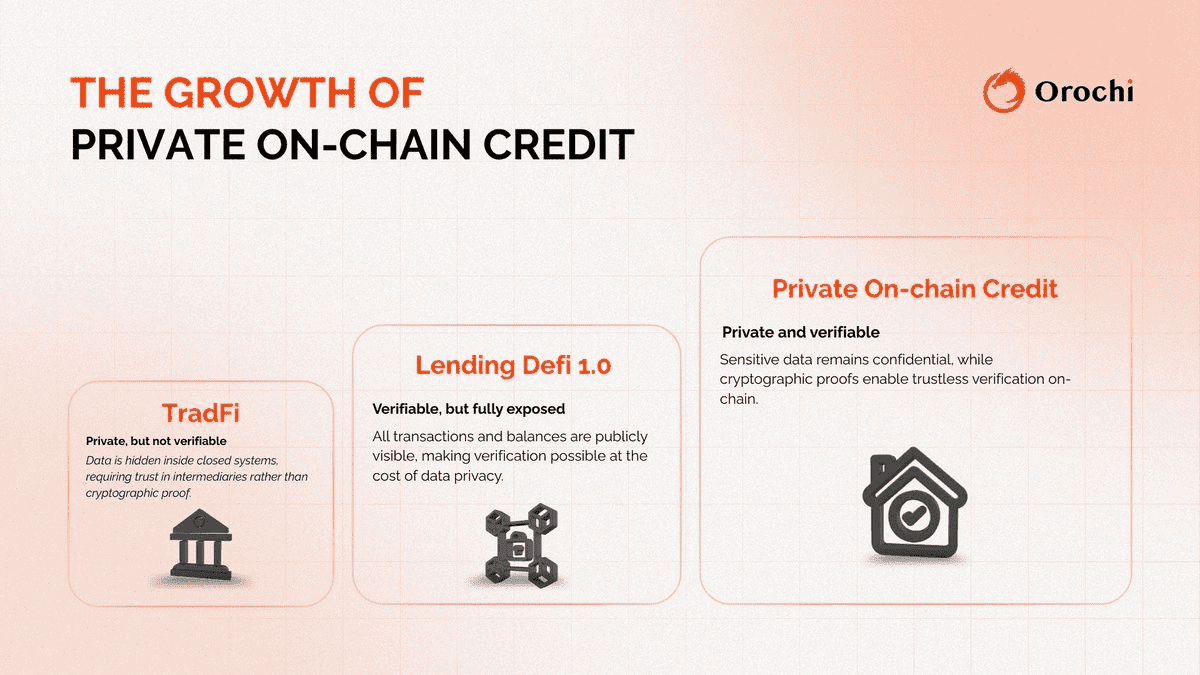

Private credit has quietly become one of the most important corners of modern finance. For years, institutions have used private credit to lend to businesses, finance receivables, structure specialty loans, and earn yield outside public bond markets. Now, that market is starting to move onchain. In crypto, on-chain private credit refers to private debt or credit exposures that are issued, represented, serviced, distributed, or reported through blockchain-based infrastructure rather than staying entirely inside traditional offchain fund plumbing. Goldfinch’s docs define private credit as loans or other forms of credit that are not issued or traded on public markets, usually involving non-bank lenders providing capital to businesses or loan pools.

That definition matters because on-chain private credit is not the same as ordinary DeFi lending. DeFi lending usually means crypto users posting crypto collateral to borrow other crypto assets. On-chain private credit is different: the underlying borrower, receivable, or strategy is usually tied to real-world economic activity, such as business lending, trade finance, consumer receivables, real estate-backed loans, SME finance, or diversified credit funds. RWA.xyz classifies tokenized credit as non-sovereign debt including private credit, on-chain lending, corporate credit, structured credit, and specialty credit.

As of April 2026, this sector is no longer theoretical. RWA.xyz’s tokenized credit dashboard shows $5.12 billion in distributed value and $20.32 billion in represented value across tokenized credit assets, with more than 184,000 holders. That makes credit one of the largest real-world-asset segments onchain outside stablecoins.

What Does On-Chain Private Credit Actually Mean?

At a basic level, on-chain private credit means that a private-credit product uses blockchain as part of its financial infrastructure. That can happen in different ways. Sometimes the underlying loans remain offchain while investor interests are tokenized onchain. Sometimes a fund or certificate gives tokenized exposure to an underlying private-credit strategy. Sometimes the borrower side is crypto-native but the credit itself finances real-world activity. Galaxy’s February 2026 note on on-chain credit argues that stablecoins, on-chain data, and smart contracts are creating a new credit infrastructure that is more global, programmable, and efficient than traditional systems.

This is why the phrase can describe several related models rather than one rigid product type. RWA.xyz’s allocation-vault primer explains that managers are increasingly using blockchain to distribute private-credit exposure through tokenized wrappers and vault structures, while keeping the underlying servicing and risk management aligned with traditional private-credit practices.

How Is It Different From Traditional Private Credit?

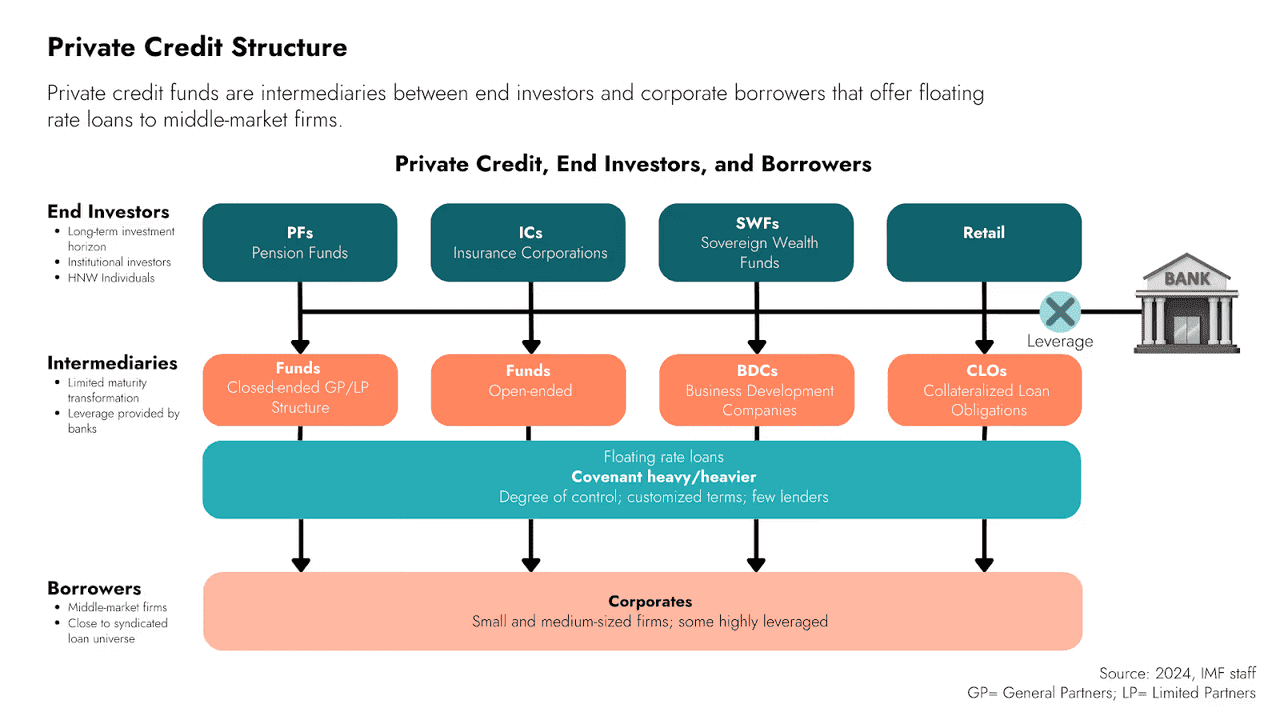

Traditional private credit is usually hard to access. Investors often face high minimums, long lockups, complex subscription documents, and limited reporting visibility. Transfers can be slow, fund administration can be heavy, and distribution is often restricted to institutional or wealthy investors through private channels. Goldfinch’s Prime FAQ says private credit has historically been attractive to institutions and HNWIs, and that on-chain products are trying to expand access to that asset class.

On-chain private credit does not eliminate those realities, but it can improve the wrapper around them. Blockchain rails can make ownership records more transparent, create faster settlement, standardize investor access through tokenized fund shares or certificates, and allow some products to plug into DeFi markets as collateral or yield-bearing assets. RWA.xyz’s case study on mF-ONE, for example, shows a tokenized certificate giving on-chain exposure to a diversified private-credit and digital-asset strategy, with potential use in DeFi lending markets like Morpho.

How Is It Different From DeFi Lending?

This is one of the most important distinctions in the entire article.

In classic DeFi lending, users deposit crypto such as ETH, WBTC, or stablecoins into a protocol and borrow against overcollateralized positions. That market is highly liquid and transparent, but it usually stays inside crypto-native collateral loops. Galaxy’s lending research distinguishes these crypto-collateralized DeFi markets from the newer generation of on-chain credit tied to broader real-world activity.

On-chain private credit, by contrast, usually finances something outside the crypto system itself: invoices, trade receivables, SME loans, structured vehicles, business lending pools, or real-estate-backed credit. Goldfinch’s docs say private credit involves non-bank lenders providing capital to businesses or loan pools, which is very different from a trader borrowing USDC against ETH.

So the easiest comparison is this:

DeFi lending = mostly crypto collateral backing crypto borrowing.

On-chain private credit = blockchain rails used to finance or distribute exposure to real-world credit.

Why On-Chain Private Credit Matters

On-chain private credit matters because private credit is a huge market in traditional finance, and blockchain can improve how that market is distributed and monitored. RWA.xyz’s framework work and allocation-vault research show that credit products are increasingly being adapted for on-chain distribution because there is real demand for tokenization yield that is not purely crypto-native.

It also matters because tokenized credit offers something DeFi has long wanted: yield linked to real economic activity instead of only crypto leverage cycles. In a market where traders often rotate between low-risk tokenized Treasuries and higher-risk DeFi yields, on-chain private credit can occupy the middle ground: potentially higher yield than Treasuries, but backed by identifiable real-world lending strategies rather than only on-chain speculation. Galaxy’s February 2026 note frames this as part of a broader convergence between stablecoins, on-chain data, and programmable credit infrastructure.

Finally, it matters because it creates a path for traditional asset managers and credit funds to reach on-chain capital pools. Centrifuge’s 2025 and 2026 materials explicitly describe private credit as one of the asset classes already moving onchain under regulated and institutional structures.

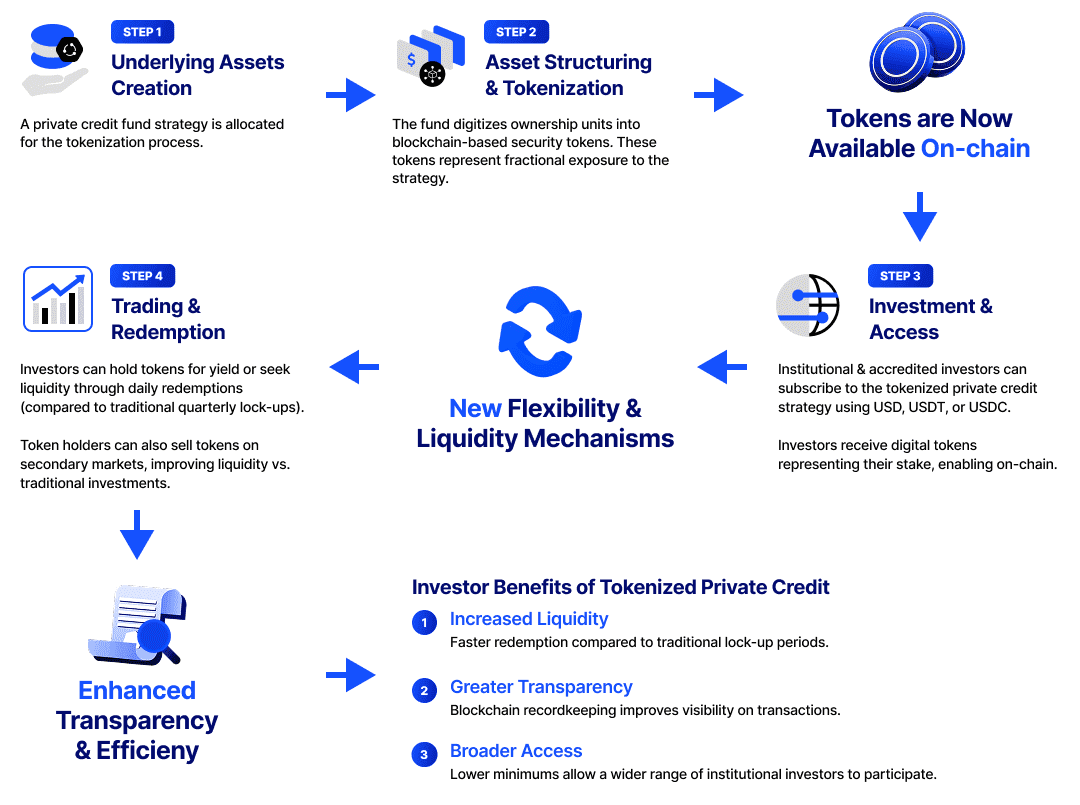

How On-Chain Private Credit Works

Most on-chain private-credit products follow a similar sequence, even if the exact legal structure varies.

A real-world credit strategy exists

This could be consumer lending, SME loans, trade finance, invoice financing, real-estate-backed debt, or a diversified private-credit fund. Goldfinch’s docs and RWA.xyz’s asset examples both show that the underlying assets usually remain normal real-world credit exposures.

A legal issuer or fund structure wraps that exposure

Because these are regulated financial claims, they usually sit inside SPVs, feeder funds, certificates, or similar legal vehicles. RWA.xyz’s allocation-vault primer explicitly compares tokenized allocation vaults with traditional fund structures and shows how managers adapt existing private-credit strategies for on-chain investors.

The investor interest gets tokenized

The token might represent a share, certificate, note, vault share, or other claim on the underlying strategy. For example, RWA.xyz describes mF-ONE as a tokenized certificate providing exposure to Fasanara’s credit strategy.

On-chain settlement, reporting, or transfer happens

Instead of keeping everything in offchain administration systems, ownership records, transfers, NAV updates, or reporting can be published through blockchain infrastructure. Centrifuge’s positioning as infrastructure for on-chain asset management is built around this step.

The tokenized asset may plug into DeFi

Some on-chain credit products can be used as collateral, deposited in vaults, or integrated into lending markets. RWA.xyz’s mF-ONE example notes usage in DeFi lending environments, which is one reason tokenization is strategically attractive.

The important point is that tokenization changes distribution and functionality, but it does not remove the underlying need for underwriting, legal structures, servicing, and collections.

Common Types of On-Chain Private Credit

This category is broader than many people assume.

Direct business lending

This includes loans to businesses, often SMEs or specialized borrowers, originated offchain and funded through tokenized pools or vehicles. Goldfinch’s private-credit framing fits this model directly.

Trade finance and receivables

This includes invoice financing, supply-chain receivables, and short-duration credit linked to business cash flows. RWA.xyz’s diversified credit examples and Galaxy’s views on the future of on-chain credit both place receivables and trade-finance-style strategies inside the broader tokenized-credit universe.

Real-estate-backed credit

Real estate does not need to be tokenized as equity to show up onchain. Debt backed by property or mortgage-like structures can also be tokenized, and RWA.xyz notes that many tokenized real-estate designs increasingly look more like private credit than speculative property tokens.

Diversified private-credit funds

Some products wrap a managed credit strategy rather than one loan pool. mF-ONE is one example, described as a diversified private-credit and digital-asset fund exposure.

Structured and specialty credit

RWA.xyz’s tokenized credit category explicitly includes structured and specialty credit, showing how broad the sector has become.

Real Examples in the Market

A useful way to understand the sector is through real examples.

Goldfinch

Goldfinch is one of the better-known names in on-chain private credit. Its docs define the asset class clearly, and Goldfinch Prime is presented as on-chain access to diversified private credit for eligible investors.

Centrifuge

Centrifuge is not only a credit product; it is infrastructure for tokenizing and distributing real-world assets, including private credit. Its public materials repeatedly point to credit, funds, and structured vehicles as core use cases.

Fasanara / mF-ONE

RWA.xyz’s mF-ONE example is helpful because it shows how a traditional diversified credit strategy can be wrapped in a tokenized certificate and then used more natively in on-chain markets.

Credbull

Centrifuge’s 2024 write-up on Credbull describes it as a licensed on-chain private-credit fund, highlighting real-time transparency and on-chain distribution.

Galaxy

Galaxy’s recent research does not just comment on the market; it is also active through products such as the Galaxy Onchain Credit Fund and even tokenized structured-credit vehicles like its tokenized CLO announcement in January 2026.

These examples show that on-chain private credit is no longer limited to one type of issuer or structure. Asset managers, crypto-native protocols, and hybrid firms are all participating.

Benefits of On-Chain Private Credit

More transparency

Blockchain-based ownership and reporting can make it easier to track holdings, NAV movements, and fund activity compared with older private-credit infrastructure. Centrifuge and RWA.xyz both emphasize real-time transparency as a key advantage.

Better distribution

Tokenization can help private-credit products reach a broader set of investors and liquidity venues. Goldfinch Prime’s positioning around expanding access is a clear example.

Faster settlement and programmability

On-chain wrappers can improve transfer speed, automate reporting or distributions, and make credit products more usable in digital-asset environments. Galaxy’s February 2026 perspective emphasizes programmability and efficiency as major parts of the new credit infrastructure.

DeFi composability

Some tokenized credit products can be posted into DeFi lending or vault systems, turning traditionally illiquid exposures into more flexible financial instruments. The mF-ONE example is especially relevant here.

Potential diversification

For crypto investors, on-chain private credit offers exposure to yield sources that are less directly tied to crypto leverage cycles. This is an inference, but it is strongly supported by the fact that the underlying returns come from non-public real-world debt rather than only crypto-collateral loops.

Risks of On-Chain Private Credit

Credit risk still exists

This is the most important caveat. Blockchain does not eliminate defaults. RWA.xyz’s distressed-debt case study says this plainly: putting a private-credit transaction onchain does not remove the underlying credit risk.

Legal and servicing complexity

These products still rely on offchain legal documents, servicing agents, originators, custodians, and enforcement mechanisms. Tokenization changes the wrapper, not the need for real-world collections and legal recourse.

Liquidity risk

Secondary markets for tokenized credit are still developing. RWA.xyz’s real-estate dashboard notes that secondary liquidity remains a primary bottleneck for tokenized real-world assets, and that lesson applies broadly to credit as well.

Structure risk

The tokenized wrapper matters. Different products use different legal claims, investor rights, and redemption rules. Not every on-chain credit token gives the same protections. This is an inference based on the variety of structures described in RWA.xyz’s research and market examples.

Operational risk

Smart contracts, oracles, NAV updates, and cross-platform integrations add technical risk on top of ordinary private-credit risk. Galaxy’s view of on-chain credit as a new infrastructure underscores that these products sit across both financial and blockchain systems.

Why This Sector Could Keep Growing in 2026

Several trends support continued growth.

First, the market already has a measurable scale. RWA.xyz’s tokenized-credit dashboard shows billions in value and a large holder base, which suggests this is no longer an experimental fringe.

Second, institutional infrastructure is improving. Centrifuge’s late-2025 and early-2026 pieces argue that tokenized private credit is already operating with more mature structures and expectations, while Galaxy’s recent work suggests that credit infrastructure is converging with stablecoins and prime-service infrastructure.

Third, investors want yield sources beyond pure crypto volatility. Tokenized private credit can serve that demand, especially when paired with on-chain distribution and reporting. This is an inference, but it follows directly from the market’s growth and from the positioning of funds like Goldfinch Prime and tokenized diversified-credit products.

Conclusion

On-chain private credit is one of the clearest examples of how blockchain is moving beyond purely crypto-native speculation and into actual financial infrastructure.

It takes an old asset class, private debt, and updates the operating model with tokenization, on-chain settlement, improved transparency, and in some cases DeFi composability. Goldfinch, Centrifuge, Galaxy, and the broader RWA ecosystem are all helping shape what that looks like in practice.

As RWAs continue to expand beyond tokenized Treasuries into more sophisticated yield strategies, on-chain private credit is likely to remain one of the most important sectors to watch. For traders looking to stay ahead of emerging narratives—from RWAs and on-chain credit to PayFi, AI, and tokenized markets—Phemex offers a secure and user-friendly platform to explore the market, monitor new opportunities, and sharpen your trading edge.