Key Takeaways

-

President Trump’s crypto policy has shifted the U.S. federal posture from enforcement-heavy ambiguity toward explicit support for digital assets, self-custody, dollar-backed stablecoins, and clearer SEC/CFTC jurisdictional lines.

-

The administration’s January 2025 executive order created a President’s Working Group on Digital Asset Markets, called for a federal framework for digital assets and stablecoins, and prohibited agencies from advancing a U.S. CBDC.

-

Trump’s March 2025 order establishing a Strategic Bitcoin Reserve strengthened the symbolic and policy status of Bitcoin as a strategic asset class in Washington, even though it did not itself create a new derivatives rulebook.

-

In 2026, the practical story for Bitcoin derivatives is less about political slogans and more about regulators: the SEC and CFTC have moved toward a joint taxonomy for crypto assets, and the CFTC under Chairman Michael S. Selig is openly pushing to onshore perpetuals and modernize collateral rules.

-

For Bitcoin derivatives traders, that likely means more U.S.-regulated product expansion, more institutional participation, and stronger competition with offshore venues. But it does not mean all uncertainty is gone, because major market-structure legislation remains stalled in Congress.

By 2026, “Trump’s crypto policy” is no longer just campaign rhetoric. It has become a real governing framework with direct consequences for how Bitcoin is traded, margined, and regulated in the United States. For spot investors, that matters because regulatory clarity can influence access and liquidity. For derivatives traders, it matters even more, because Bitcoin derivatives sit at the intersection of several policy domains at once: commodities law, securities law, exchange oversight, collateral rules, stablecoin infrastructure, and cross-market supervision.

That is why the biggest question in 2026 is not simply whether Trump is “pro-crypto.” He clearly is. The more useful question is what that pro-crypto posture actually changes for Bitcoin derivatives—futures, options, basis trades, margined spot-like products, and especially the long-awaited push to bring perpetuals-style trading onshore.

The short answer is that Trump’s policy has materially improved the outlook for Bitcoin derivatives in the U.S. It has done so by elevating Bitcoin politically, empowering the CFTC, encouraging SEC-CFTC harmonization, supporting stablecoin rails, and signaling that novel crypto products should be brought into regulated U.S. markets rather than pushed offshore. But the policy shift is not the same thing as a finished legal framework. There is still a meaningful difference between a friendlier regulator and a fully settled statute.

What Trump’s Crypto Policy Actually Looks Like in 2026

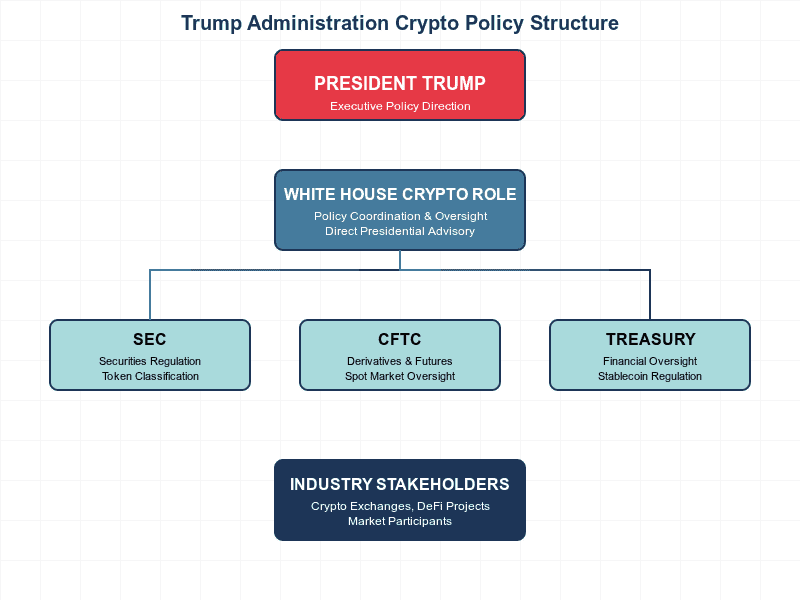

The foundation of the administration’s crypto policy was laid in the January 23, 2025 executive order, Strengthening American Leadership in Digital Financial Technology. That order declared it U.S. policy to support the responsible growth and use of digital assets and blockchain technology, protect lawful access to public blockchain networks and self-custody, promote dollar-backed stablecoins, improve banking access for lawful crypto activity, and provide regulatory clarity built on defined jurisdictional boundaries. It also revoked Biden-era Executive Order 14067 and terminated agency efforts to establish a U.S. central bank digital currency.

The same order created the President’s Working Group on Digital Asset Markets, chaired by the White House’s Special Advisor for AI and Crypto and including the Treasury Secretary, Attorney General, Commerce Secretary, SEC Chair, and CFTC Chair. It required agencies to identify and review crypto-related regulations and directed the Working Group to recommend both regulatory and legislative proposals, including a federal framework for digital assets and stablecoins.

The second major pillar was the Working Group’s July 30, 2025 report. In that fact sheet, the White House said the administration wanted to make America the “crypto capital of the world,” urged Congress to enact a fit-for-purpose market-structure regime, recommended giving the CFTC authority over spot markets for non-security digital assets, and called on the SEC and CFTC to use existing authority to enable digital-asset trading, clarify registration and custody issues, and use safe harbors and regulatory sandboxes to speed innovation.

The third pillar was Trump’s March 6, 2025 executive order establishing a Strategic Bitcoin Reserve and a separate U.S. Digital Asset Stockpile. The order said Bitcoin’s fixed supply and security give it a strategic status akin to “digital gold,” directed the Treasury to maintain reserve accounts for government-held BTC, and stated that reserve BTC should not be sold except in limited circumstances.

Taken together, these moves created a consistent policy message: the administration sees Bitcoin and digital assets as something to cultivate, structure, and onshore—not something to marginalize through uncertain enforcement. That is the political backdrop for every major Bitcoin derivatives development in 2026.

Why Bitcoin Derivatives Care More About Regulators Than Headlines

Bitcoin derivatives are not driven only by the price of BTC. They are also driven by the legal status of the underlying asset, the permissibility of leverage, the classification of venues, the treatment of collateral, the design of clearing arrangements, and the agencies that supervise them. That is why the SEC-CFTC relationship matters so much.

In March 2026, the SEC issued a formal interpretation clarifying how federal securities laws apply to crypto assets and transactions involving them. The SEC, joined by the CFTC, set out a taxonomy covering digital commodities, digital collectibles, digital tools, stablecoins, and digital securities, and SEC Chair Paul Atkins said the interpretation acknowledges that most crypto assets are not themselves securities. The CFTC said it would administer the Commodity Exchange Act consistently with that interpretation.

For Bitcoin derivatives, that matters because Bitcoin was never really the main securities-law problem. The bigger problem was fragmentation and spillover uncertainty across crypto markets. A clearer federal taxonomy lowers the risk that products tied to non-security crypto assets will be delayed or chilled by unresolved turf battles. The March 2026 SEC-CFTC memorandum of understanding reinforces that point by committing both agencies to clarify product definitions, modernize margin and collateral frameworks, coordinate on novel crypto products, and avoid regulation through enforcement.

The CFTC Is Becoming the Main Growth Engine for Bitcoin Derivatives

The most important regulator for Bitcoin derivatives in 2026 is the CFTC, and Trump’s appointees have made that obvious.

Michael S. Selig, nominated by Trump and sworn in as CFTC Chairman on December 22, 2025, came into office with a mandate to modernize crypto market oversight and coordinate closely with the SEC. His official CFTC biography says he previously served as chief counsel of the SEC’s Crypto Task Force and helped develop a clearer framework for digital-asset securities markets while working to harmonize SEC and CFTC regimes.

In his January 29, 2026 speech, Selig said the CFTC would partner with the SEC on “Project Crypto,” clarify jurisdictional lines, reduce fragmentation, and modernize rules for crypto markets. Most important for derivatives, he explicitly said the CFTC would use its tools to onshore perpetuals and other novel derivative products under “transparent and workable frameworks” with appropriate safeguards.

That is a major signal because perpetual futures dominate offshore crypto trading. Reuters reported on April 22, 2026 that U.S. exchanges are racing to expand into crypto perpetuals ahead of expected CFTC clarification, and that Selig has indicated the agency plans to approve perps soon. Reuters also reported that global perpetual futures volume reached $61.7 trillion in 2025, far above spot crypto volume.

Spot, Margin, and Collateral Rules Are Also Moving in Bitcoin’s Favor

The policy shift is not limited to futures contract design. It also affects the plumbing around derivatives.

In August 2025, the CFTC launched an initiative on listed spot crypto trading; in December 2025 it announced that listed spot cryptocurrency products would begin trading on CFTC-registered futures exchanges for the first time. The agency framed that as part of the administration’s push to create safer regulated alternatives to offshore venues. Reuters separately reported the same development.

That matters for Bitcoin derivatives because spot and derivatives markets are tightly linked. Better-regulated spot access helps benchmark formation, surveillance, basis trading, hedging, and the design of exchange-traded products tied to BTC. A market where spot and derivatives are both increasingly available in regulated U.S. venues is a market that is easier for institutions to trust and integrate.

Collateral is the next big piece. In December 2025, the CFTC launched a digital-assets pilot program allowing certain digital assets—including BTC, ETH, and USDC—to be used as collateral in derivatives markets, alongside guidance on tokenized collateral. The CFTC said this would provide clearer guardrails and enhanced monitoring, while industry participants highlighted the potential for 24/7 trading, near-real-time margin settlement, and improved capital efficiency.

For Bitcoin derivatives desks, that is a meaningful practical change. Better collateral treatment can improve capital efficiency for hedgers, basis traders, and market makers. It can also make it easier to run strategies that bridge spot BTC, ETFs, futures, and options, especially if the broader regulatory environment continues to converge around tokenized collateral and stablecoin settlement rails.

What This Means for Institutional Bitcoin Derivatives Trading

Institutional traders usually care less about ideological debates and more about market access, legal certainty, margin efficiency, and counterparty risk. On those dimensions, Trump’s 2026 crypto posture is mostly constructive for Bitcoin derivatives.

First, it reduces the odds that U.S. institutional flow must default to offshore venues for certain strategies. The combination of SEC-CFTC coordination, CFTC support for spot crypto on regulated exchanges, tokenized collateral pilots, and the push to onshore perpetuals points toward a broader domestic market stack.

Second, it increases the likelihood that Bitcoin derivatives will be treated as part of a coherent U.S. market structure rather than as an exception handled through case-by-case friction. The SEC’s March 2026 crypto interpretation, the CFTC’s innovation agenda, and the interagency MOU all point to a more coordinated model built around clarity, timely processing, and fewer duplicative processes.

Third, it strengthens the link between Bitcoin’s political legitimacy and its financial-market legitimacy. The Strategic Bitcoin Reserve did not create a derivatives rule, but it did reinforce the idea that Bitcoin is no longer treated in Washington merely as a speculative nuisance. That kind of signaling matters when boards, risk committees, and compliance teams evaluate whether Bitcoin derivatives belong in a serious institutional toolkit.

Where the Policy Still Falls Short

The biggest limitation is that regulatory friendliness is not the same as legislation. Reuters reported in January, February, and March 2026 that major crypto market-structure legislation—the Clarity Act—remains stuck amid disputes between banks and crypto firms, especially over stablecoin-related rewards and broader financial-stability concerns. Reuters also reported that some Democrats want ethics restrictions aimed at preventing elected officials from profiting from crypto ventures, a politically sensitive issue given the Trump family’s crypto ties.

That matters for Bitcoin derivatives because without legislation, too much still depends on agency interpretation, self-certification, and administrative priorities that could change over time. Reuters’ April 2026 report on perpetuals noted that these products still sit in a gray area and that self-certification alone may not feel durable enough for all market participants.

There is also a second limitation: being pro-innovation does not mean being permissive about everything. Chairman Selig told Congress in April 2026 that fraud, manipulation, and insider trading in CFTC markets would still face the “full force of the law.” So traders should not confuse a pro-crypto administration with a no-rules environment.

Finally, there is real political risk. If legislation misses the 2026 window, Reuters reports that the path could become harder after the midterms. That means the market may continue to enjoy regulatory momentum without yet having full statutory certainty.

So What Should Bitcoin Derivatives Traders Watch Next?

The next key developments are fairly clear.

The first is whether the CFTC formally creates a stronger pathway for U.S. perpetual futures. That is the single biggest potential unlock for Bitcoin derivatives in 2026 because it would directly challenge offshore dominance in one of crypto’s highest-volume markets.

The second is whether collateral modernization continues. If tokenized collateral, stablecoin margining, and 24/7 settlement become more normalized inside CFTC-regulated markets, Bitcoin derivatives could become significantly more capital-efficient and institution-friendly.

The third is whether Congress converts the administration’s direction into statute. If market-structure legislation passes, the Trump policy shift could become more durable and less dependent on who occupies the White House or chairs the agencies. If it fails, the market will still have made progress, but that progress will remain more reversible.

Conclusion

Trump’s crypto policy in 2026 is best understood as a broad effort to onshore, legitimize, and scale digital-asset markets in the United States. For Bitcoin derivatives, that has several concrete implications: clearer SEC-CFTC coordination, a stronger CFTC role, better odds for onshore perpetuals, more openness to tokenized collateral, and a policy environment that increasingly treats Bitcoin as a strategic and financial asset rather than a regulatory anomaly.

That is the bullish interpretation, and it is grounded in real policy actions. But there is also a sober interpretation: this transition is incomplete. Until Congress passes a lasting market-structure law, Bitcoin derivatives in the U.S. will still depend heavily on administrative will, agency coordination, and how far regulators are willing to go under existing authority.

So the real takeaway is not that Trump’s crypto policy guarantees a Bitcoin derivatives boom. It is that, as of April 2026, it has made that boom more plausible, more onshore, and more institutionally accessible than it looked just a year ago.