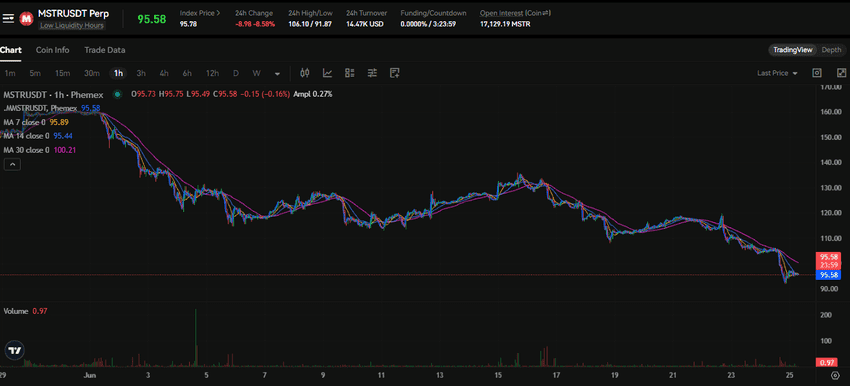

MSTR fell 8.55% to $95.55 on June 25, 2026, while Bitcoin dropped below $61,000 to trade around $60,714. The stock lost roughly a tenth more than the asset it is built on, and that gap is not random. It is the single number that governs how every Bitcoin treasury company trades, and most retail buyers of these stocks have never heard its name.

That number is mNAV, short for market-cap-to-net-asset-value. It measures how much you are paying for a company's Bitcoin relative to what that Bitcoin is actually worth. When the premium is rich, treasury stocks fly. When it compresses, they fall harder than Bitcoin itself, exactly what played out today. Here is what mNAV is, how to calculate it, and how traders use it to judge if a treasury stock is cheap or expensive.

What mNAV Is and How to Calculate It

mNAV stands for market net asset value, and the metric most traders care about is the mNAV multiple. It answers one question. For every dollar of Bitcoin a company holds, how many dollars is the market charging you to own it through the stock?

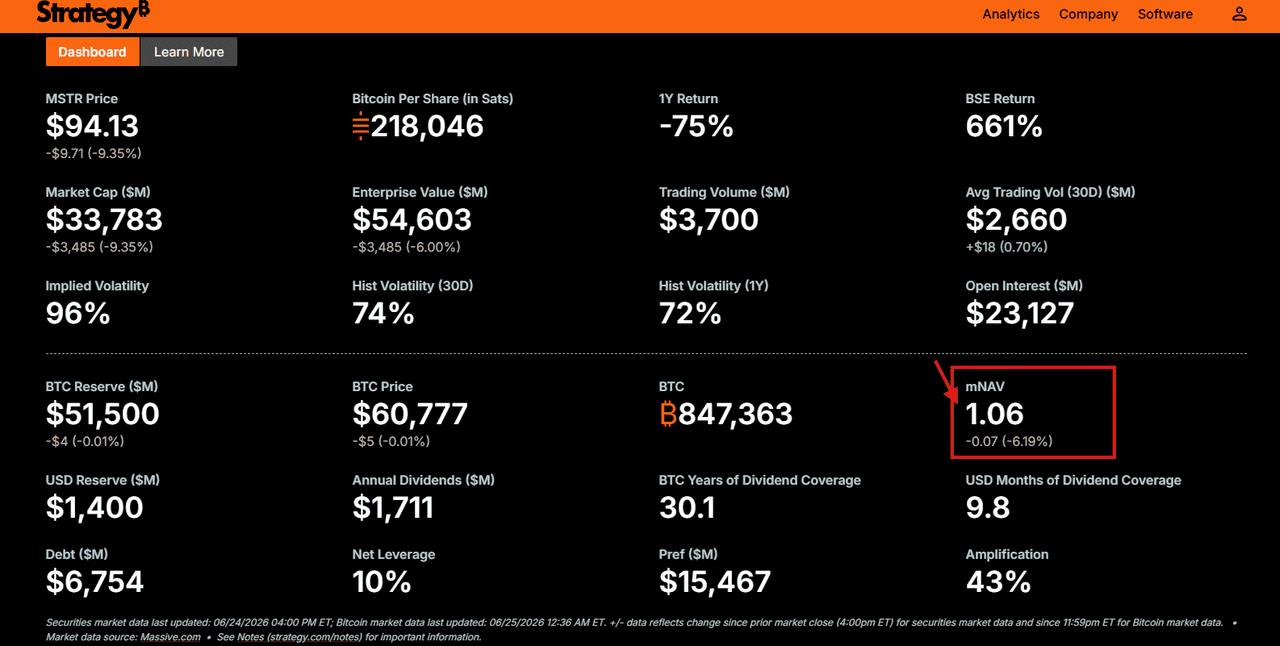

The math is direct. Take the company's market capitalization and divide it by the net asset value of its Bitcoin holdings. Strategy, the company formerly branded MicroStrategy, holds more than 700,000 BTC. At a BTC price near $60,714, that treasury is worth roughly $42.5 billion before you adjust for debt. If the company's market cap is larger than that figure, the stock trades at a premium and mNAV is above 1. If the market cap is smaller, the stock trades at a discount and mNAV is below 1.

Source: Strategy

A worked example makes it concrete. Suppose a treasury company holds 700,000 BTC worth $42.5 billion, carries $8 billion in convertible debt, and has a market cap of $68 billion. The net asset value of the Bitcoin after subtracting debt is about $34.5 billion. Dividing the $68 billion market cap by that net figure gives an mNAV close to 1.97. The market is paying nearly two dollars for every dollar of net Bitcoin value.

|

Term

|

What it measures

|

Reading

|

|

mNAV above 1

|

Stock trades at a premium to its Bitcoin

|

Bullish sentiment, expensive

|

|

mNAV equal to 1

|

Stock priced at exactly its Bitcoin value

|

Fair, no premium

|

|

mNAV below 1

|

Stock trades at a discount to its Bitcoin

|

Bearish sentiment, cheap on paper

|

The reason this matters more than a normal price-to-book ratio is that the underlying asset reprices every second. A treasury stock's fundamentals move with BTC tick by tick, so the premium is the only thing left for traders to actually trade.

Why the Premium Exists and Why It Compresses

A rational first reaction is that no one should pay $1.97 for $1 of Bitcoin when they can buy the Bitcoin directly. The premium exists anyway, and there are real reasons for it.

Some buyers cannot hold spot Bitcoin. Pension funds, certain mandates, and retirement accounts can own a Nasdaq-listed stock but not a crypto wallet, so the stock becomes their only access point. The company also compounds its Bitcoin per share over time by issuing stock at a premium and buying more Bitcoin with the proceeds, a flywheel that rewards holders when the premium is high. Michael Saylor, the executive chairman, has built the entire strategy around this loop, and his Bitcoin buying is funded largely by capital raised against that premium.

The premium compresses when sentiment turns. In a bull market, traders extrapolate the flywheel forever and bid mNAV toward 2 or higher. In a selloff, the same traders question if the company can keep issuing stock at a premium, and the multiple deflates toward 1. Today's 8.55% drop in MSTR against a smaller BTC move is mNAV compression in real time. Bitcoin fell, and on top of that the premium investors were willing to pay shrank.

The honest read is that the premium is a sentiment gauge wearing a valuation costume. It tells you how much faith the market has in the treasury model on any given day, not the intrinsic worth of the Bitcoin underneath.

Why This Makes MSTR a Leveraged Bitcoin Proxy

The combination of a moving asset and a moving premium is what turns a treasury stock into a leveraged play. When Bitcoin rises, the BTC holdings gain value and the premium often expands at the same time, so the stock can rise far more than the coin. When Bitcoin falls, both effects reverse and the stock falls harder.

Today is the clean illustration. BTC slipped below $61,000, a move of a few percent from recent levels, while MSTRdropped 8.55% to $95.55. The stock behaved like Bitcoin with the volume turned up. This is why traders treat these names as high-beta BTC exposure rather than as ordinary equities.

The debt layer amplifies the effect further. Because the company funds Bitcoin purchases partly with borrowed money, the equity sits behind that debt in the capital structure. A drop in Bitcoin shrinks the asset side while the debt stays fixed, which mathematically magnifies the hit to net asset value per share. Leverage cuts both ways, and a treasury stock is leverage you can buy in a brokerage account.

How Convertible Debt and At-the-Money Issuance Shape mNAV

Two financing tools drive the whole machine, and understanding them is the difference between reading mNAV correctly and getting fooled by it.

Convertible debt is a bond that can turn into stock if the share price rises above a set conversion level. Strategy has used convertible notes to raise billions at low interest rates, betting that the shares climb enough for the bonds to convert rather than be repaid in cash. This is cheap funding while Bitcoin rises. The catch is that a deep selloff can leave the debt sitting as an obligation that must be serviced, which is why the debt-adjusted version of mNAV matters more than the headline version during drawdowns.

At-the-money issuance, often shortened to ATM, lets the company sell new shares directly into the open market over time. When mNAV is well above 1, every share sold raises more dollars than the Bitcoin it buys is worth, so each issuance is accretive and grows Bitcoin per share. When mNAV falls near or below 1, that math breaks. Selling shares at a discount to Bitcoin value destroys Bitcoin per share, so the company loses its most powerful tool exactly when it needs capital most.

This is the feedback loop that makes treasury stocks reflexive. A high premium funds more buying, which feeds the story, which supports the premium. A low premium starves the flywheel, which weakens the story, which pressures the premium further. The same dynamic shows up in how Bitcoin ETF flows move sentiment across the whole BTC-proxy complex, treasury stocks included.

How Traders Use mNAV to Judge Cheap Versus Expensive

mNAV is most useful as a relative gauge, not an absolute one. A multiple of 1.5 means nothing on its own. It means a great deal once you compare it to where that same stock has traded over the past year.

The practical approach is to track the mNAV range. If a treasury stock has historically swung between 1.2 and 2.5, then a reading near 1.2 suggests the market is pricing in heavy pessimism and the premium has little room left to fall. A reading near 2.5 suggests euphoria and a premium that has historically reverted. Traders who buy near the bottom of the mNAV range and trim near the top are trading the premium, not the Bitcoin.

The deeper signal is mNAV below 1. A treasury stock trading at a discount to its own Bitcoin is, on paper, cheaper than buying the coin outright, since you get the Bitcoin plus the operating business for less than the Bitcoin alone. That looks like free money, but it usually appears precisely when the market doubts the company can survive its debt or keep the flywheel turning. The discount is the market pricing in real risk, not handing out a gift. You can cross-check the holdings and share count against the company's own disclosures on the Strategy investor relations site and its filings on SEC EDGAR before trusting any mNAV figure you read online.

FAQ

What is mNAV?

mNAV is market-cap-to-net-asset-value, a multiple that shows how much the market charges for a treasury company's Bitcoin relative to what that Bitcoin is worth. You calculate it by dividing the company's market cap by the net value of its Bitcoin holdings after subtracting debt. Above 1 is a premium, below 1 is a discount, and it is the core valuation lens for any Bitcoin treasury stock. The term is related to net asset value, the same concept funds use to value their holdings.

Why does MicroStrategy trade above its Bitcoin value?

Strategy trades at a premium because some investors can only access Bitcoin through a listed stock, and because the company grows Bitcoin per share by issuing stock at a premium and buying more BTC. That flywheel justifies an mNAV above 1 as long as sentiment holds. The premium shrinks fast in selloffs, which is what drove the 8.55% drop on June 25, 2026.

Is MSTR a leveraged Bitcoin play?

Yes. The stock moves more than Bitcoin in both directions because its premium expands in rallies and compresses in selloffs, and because convertible debt amplifies moves in net asset value. Today MSTR fell 8.55% while BTC slipped a few percent, the textbook signature of a leveraged proxy. Treat it as high-beta Bitcoin exposure, not a stable equity.

Bottom Line

mNAV is the number that decides treasury stocks, and June 25, 2026 was a clean lesson in why. MSTR fell 8.55% to $95.55 while BTC lost less ground below $61,000, because the stock carries both the asset and a premium that deflates when fear rises. Track the mNAV range rather than the headline price. A reading near the low end of its historical band signals pessimism that tends to revert, a reading near the high end signals a premium that tends to compress, and a slip below 1 is a warning that the market doubts the flywheel, not a discount to grab blindly. The Bitcoin is the engine, but the premium is what you are actually trading.

This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency trading involves substantial risk. Always conduct your own research before making trading decisions.