Key Takeaways

Chintai is a regulated digital asset platform focused on tokenization, marketplace infrastructure, compliance, custody, and distribution for RWAs.

CHEX is the ecosystem utility token used for platform resources and fee-related functions, with staking built into the model.

The platform emphasizes compliance-first design, including KYC/AML onboarding, codified regulatory controls, geofencing, transaction monitoring, and automated reporting.

Chintai’s product suite covers the full lifecycle of tokenized assets: issuance, listing and trading, custody, compliance, and liquidity distribution.

As of April 2026, Chintai’s recent momentum includes a Chainlink interoperability integration in August 2025 and a January 2026 partnership tied to a nature-based development project in Indonesia with resource rights initially estimated at $28 billion.

A Beginner’s Guide to a Regulated RWA Tokenization Platform

As real-world asset (RWA) tokenization matures, one theme is becoming impossible to ignore: institutions do not just want blockchain speed and programmability—they also want licensing, compliance, custody, and market infrastructure that can stand up in regulated environments. That is the niche Chintai is trying to own. Chintai presents itself as a one-stop platform for regulated digital assets, offering tokenization, marketplace infrastructure, compliance tooling, custody support, and blockchain-based capital markets services. Chintai Network Services Pte Ltd also states that it is regulated by the Monetary Authority of Singapore as a Capital Markets Services licensee and a Recognised Market Operator.

The project’s native token, CHEX, sits at the center of that ecosystem. According to Chintai’s official CHEX page, CHEX is the utility token used to manage resources on the Chintai Network and deepen liquidity, and all actions on the platform require CHEX. The same page describes CHEX as fully distributed, says no more tokens will ever be released, and states that 5% of value generated by Chintai is allocated to buying CHEX on the open market and permanently removing it from circulation.

In simple terms, Chintai is not trying to be “just another crypto token.” It is trying to become regulated infrastructure for bringing real assets on-chain—while CHEX functions as the network utility layer that powers usage, fee flows, and staking incentives. That makes Chintai one of the more interesting “picks-and-shovels” plays in the RWA sector.

What Is Chintai?

Chintai is a Singapore-based digital asset infrastructure company focused on helping businesses and financial institutions tokenize real-world assets in a regulated way. On its official site, Chintai describes itself as an all-in-one solution for businesses to harness real-world digital assets, with offerings spanning tokenization, marketplace services, compliance infrastructure, and blockchain platform services. Its “How it Works” section says the product suite supports the full trade lifecycle across multiple asset classes, including issuance, secondary trading, corporate actions, custody, automated compliance, and KYC/AML onboarding.

That positioning matters because many RWA projects talk mainly about tokenizing an asset, while Chintai is selling a broader stack: not just the token issuance layer, but also the market venue, compliance rails, investor onboarding, custody support, and reporting. In other words, Chintai is trying to solve the operational and regulatory complexity that often prevents real institutions from moving on-chain in a meaningful way.

This is why Chintai tends to appeal more to issuers, asset managers, and institutions than to purely speculative crypto users. Its own site explicitly targets entrepreneurs, SMEs, and financial institutions, and repeatedly frames the platform as a way to modernize capital markets rather than simply launch a token.

What Problem Is Chintai Trying to Solve?

Traditional capital markets are slow, fragmented, and paperwork-heavy. Asset issuance, compliance, distribution, custody, settlement, and investor reporting often sit across multiple vendors and legal jurisdictions. Chintai’s pitch is that blockchain can compress much of that stack into programmable infrastructure—but only if regulation and compliance are built in from the start.

Its issuance page says digital assets on the platform can be customized across virtually any asset class, with codified regulatory controls and automated corporate actions built into smart contracts. Its listing and trading page emphasizes instant settlement, 24/7 access, geofencing, automated compliance, real-time transaction monitoring alerts, and removal of the traditional T+2 settlement cycle.

That is the core Chintai thesis: if RWAs are going to scale, tokenization alone is not enough. You also need a compliant venue, onboarding controls, reporting, custody, and liquidity pathways. Chintai is trying to combine those pieces into a single regulated system.

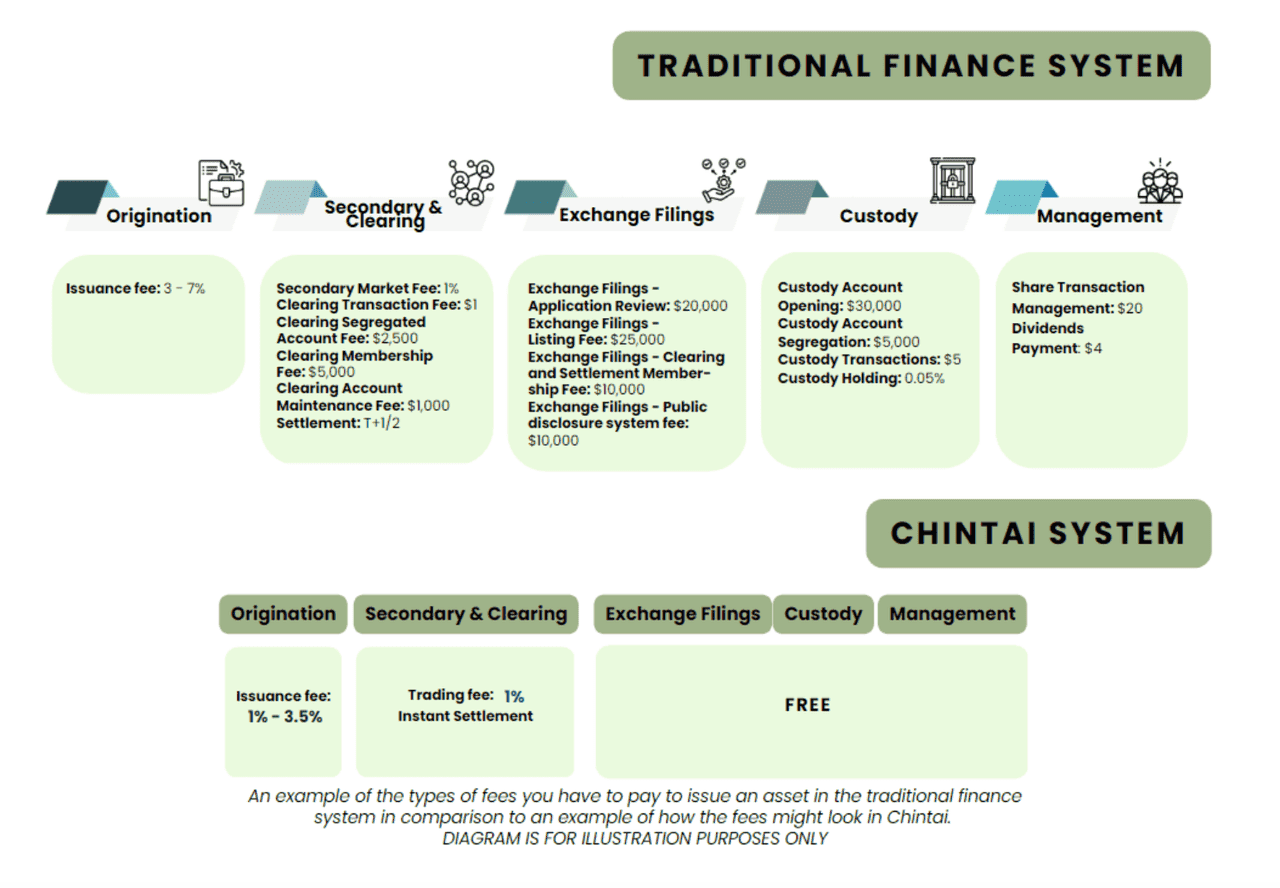

Chintai vs. Traditional Finance System (source)

How Chintai Works

Issuance

On the issuance side, Chintai says users can configure and customize virtually any asset class. The platform highlights support for securities, commodities, bonds, real estate, and even novel assets such as collectibles, art, and whiskey. It also promotes automated dividends and coupon payments, on-chain KYC/AML onboarding, reporting, and USD fiat on/off-ramps through Propine.

This matters because tokenization is rarely just “put asset on-chain.” Real issuers usually need transfer restrictions, jurisdiction-specific controls, investor eligibility rules, cap table management, and lifecycle events like distributions or coupon payments. Chintai’s issuance layer is designed to turn those requirements into programmable asset logic.

Listing and Trading

Chintai’s listing and trading page describes an MAS-regulated trading venue built for fully on-chain actions, instant settlement, 24/7 market access, automated compliance, and real-time monitoring. It also mentions dual listings, white labeling, transaction reporting, automated contract notes, and even negative maker fees designed to attract liquidity providers.

For the RWA narrative, this is important. A tokenized asset is only compelling if it can eventually be distributed and traded efficiently. Chintai is clearly marketing itself as more than an issuance platform; it wants to be a regulated marketplace layer as well.

Compliance

Compliance is arguably the biggest differentiator in Chintai’s branding. The platform says its smart contracts enforce compliance controls based on regulatory requirements and maintain accurate data for automated reporting and recordkeeping. It also highlights rapid KYC/AML onboarding, codified regulatory controls, geofencing, suspicious transaction reporting, and AI-assisted transaction monitoring.

For institutions, that may be more valuable than flashy DeFi features. The biggest barrier to on-chain adoption is often not the technology itself, but the need to prove who can hold an asset, where they are located, whether they meet investor qualification rules, and how suspicious activity is monitored and reported. Chintai’s product design shows that it understands this institutional bottleneck.

Custody

Custody is another piece of the institutional puzzle. Chintai states that digital assets are stored with a custody solution supported by a licensed Singapore custodian and a U.S. custodian, with multi-signature security, insurance, and ISO 27001-certified custody support referenced on the custody page.

That is a notable positioning choice. In crypto, many projects focus on decentralization and self-custody. Chintai, by contrast, is speaking the language of professional asset servicing and regulated safekeeping. That makes sense given its target market.

Distribution and Liquidity

Finally, Chintai says it uses interoperable technology to enable distribution, dual listings, and access to institutional liquidity via regional partners. The platform emphasizes open architecture, international marketplace access, multi-jurisdiction listings, and investor pools onboarded according to KYC/AML requirements.

This final step is crucial. Tokenized assets need more than issuance—they need credible distribution channels and liquid markets. Chintai is effectively positioning itself as infrastructure for the full journey from origination to secondary market access.

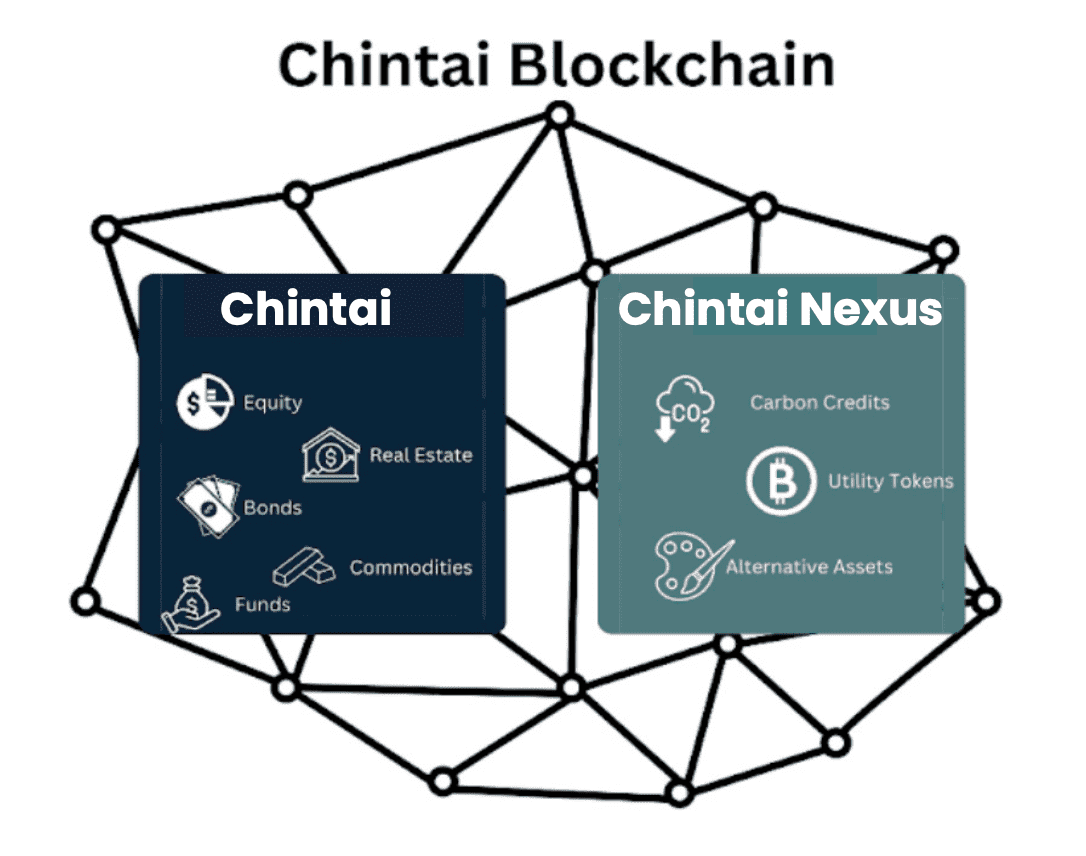

Chintai Blockchain (source)

What Is CHEX?

CHEX is the utility token that powers activity across the Chintai ecosystem. Chintai’s official CHEX page says the token is used to manage network resources and deepen liquidity, and that all platform actions require CHEX. The page also says gas fees are paid in CHEX and redistributed to CHEX stakers, while issuers must actively manage and maintain CHEX holdings unless Chintai does so on their behalf.

In practical terms, CHEX is not presented as a meme coin or governance-only token. It is meant to be economically tied to actual platform usage. If more assets are issued, traded, and maintained on Chintai infrastructure, more CHEX should be needed within the system. That is the core investment narrative around the token.

The project also emphasizes staking. According to the official CHEX page, those who stake CHEX are entitled to a portion of the platform’s gas fees; gas fees from issuances are distributed over the course of a year, while trading fees are distributed instantly. The site also notes that some clients may choose to airdrop a portion of their issuance to CHEX stakers, though those airdrops are not guaranteed and happen at the client’s discretion.

CHEX Tokenomics

Chintai’s current token page describes CHEX as fully distributed, stating that all tokens are already in circulation and that no additional tokens will ever be released. It also labels CHEX as deflationary, saying 5% of value generated by Chintai is used to purchase CHEX on the open market and permanently remove it from circulation.

Older CHEX documentation indexed on the web describes a maximum supply of 1 billion CHEX and a deflationary model in which fees can be redirected to buy and burn tokens. Because token presentation across historical documents and third-party trackers can vary, the safest approach for readers is to prioritize Chintai’s current official CHEX page and current official token documentation when evaluating token mechanics.

From a valuation standpoint, the token model is straightforward: the more real usage Chintai can generate from asset issuance, trading, and services, the stronger the economic case for CHEX becomes. But that thesis depends on business execution, client growth, and actual tokenized asset volume—not just general excitement around RWAs.

Why Chintai Matters in the RWA Sector

The RWA sector is crowded with big narratives: tokenized Treasuries, tokenized funds, stablecoin settlement, on-chain private credit, and tokenized commodities. Many projects focus on one slice of that stack. Chintai’s angle is broader: it wants to be regulated infrastructure for issuers and financial firms that need compliant tokenization from end to end.

That infrastructure-first positioning can be attractive in a market where institutions increasingly want blockchain exposure without the legal ambiguity of fully permissionless systems. Chintai’s repeated emphasis on licensing, KYC/AML, geofencing, transaction monitoring, custody, and reporting is not accidental—it is effectively telling potential clients, “you do not need to choose between blockchain efficiency and regulated operations.”

For traders and analysts, that means CHEX is often better understood as an RWA infrastructure token than as a pure consumer-facing asset. If the next stage of tokenization is institutional and compliance-heavy, then projects like Chintai may occupy a strategically useful layer of the market.

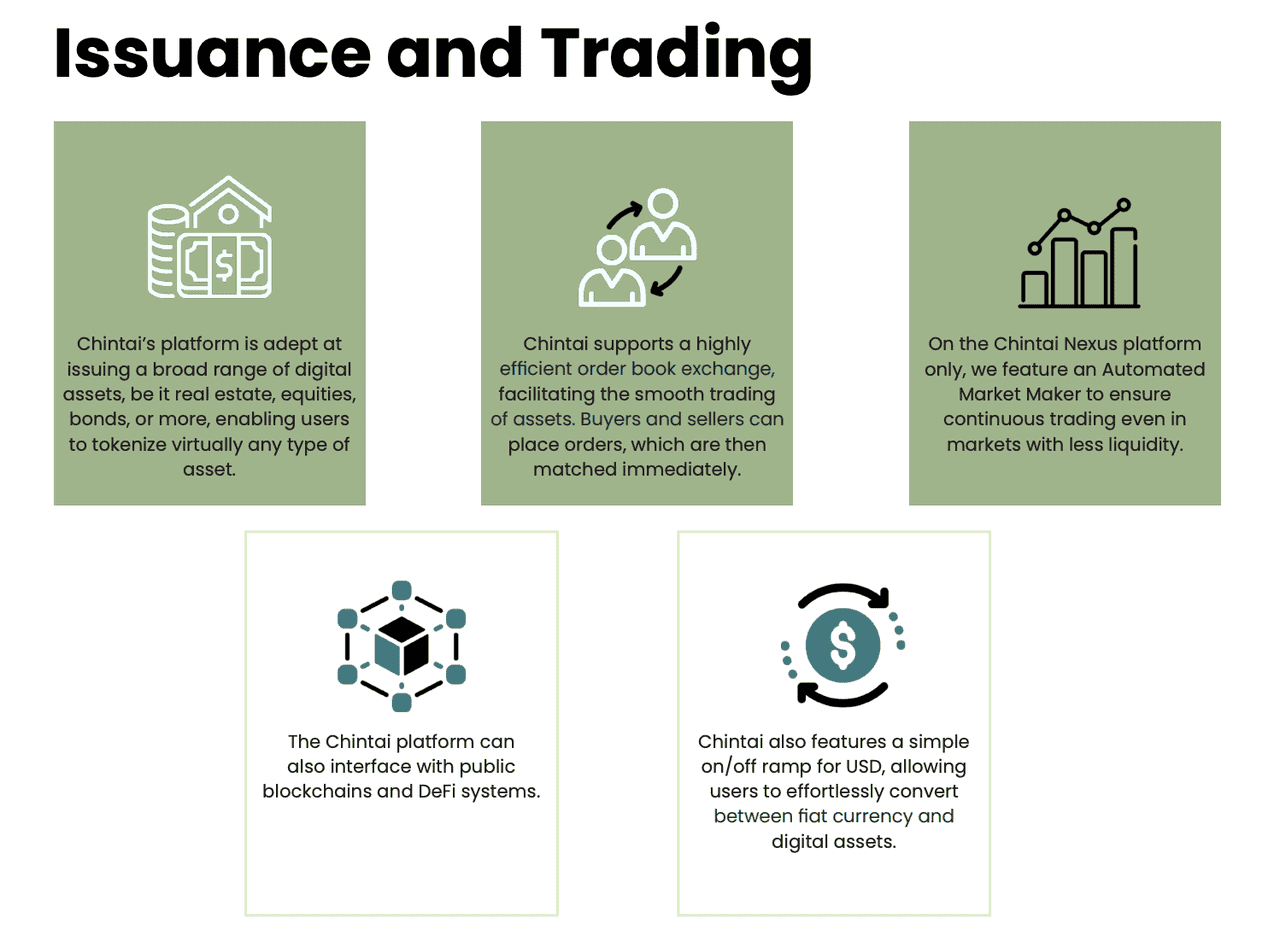

Issuance and Trading of Chintai platform (source)

Recent Chintai Developments as of April 2026

As of today, one of Chintai’s biggest recent headlines is its January 6, 2026 announcement with the Maluku Archipelago Joint Venture. According to the company announcement, Chintai entered a partnership to tokenize assets tied to a 60-year nature-based development project in Indonesia, with resource rights available for future development and tokenization initially estimated at $28 billion. The release says the future issue would be linked to those rights and that Chintai would provide tokenization infrastructure, on-chain governance systems, and security-token risk frameworks.

Another notable development came on August 12, 2025, when Chintai highlighted adoption of the Chainlink interoperability standard and an integration with Chainlink to scale regulated digital asset origination globally. Even without diving into technical specifics, the strategic implication is clear: Chintai is not only focused on tokenization itself, but also on interoperability and institutional-grade connectivity across blockchain environments.

The company’s news feed also highlights additional 2025 milestones, including a product launch with Splyce on Solana for institutional-grade tokenized securities, a SmartGold initiative tied to $1.6 billion in IRA gold, a $30 million tokenized bitcoin mining infrastructure fund via Alteri, and a $100 million tokenized real estate fund via Patel Real Estate. Taken together, these examples show that Chintai is trying to grow across multiple RWA categories rather than depending on a single flagship asset type.

What Are the Risks?

Chintai’s story is compelling, but it is not risk-free.

First, execution risk is real. Chintai’s token thesis depends on whether the company can continue attracting issuers, financial institutions, and regulated asset deals at meaningful scale. A strong product narrative does not automatically translate into sustained revenue or token demand.

Second, regulatory complexity cuts both ways. Chintai’s compliance-first identity is a strength, but also means the business must operate in a space with high legal, jurisdictional, and operational friction. That can slow growth compared with more permissionless crypto projects.

Third, RWA adoption itself is still early. Even though tokenization is one of crypto’s most promising verticals, the industry is still figuring out how to scale liquidity, custody, secondary trading, and investor access across jurisdictions. Chintai may be building for a very large future market, but that market is still developing. This is an inference based on the product categories Chintai emphasizes and the institutional infrastructure it continues to build.

Fourth, CHEX is still a crypto asset. Even if its value proposition is tied to real business activity, the token can remain volatile, and market pricing may diverge widely from fundamentals over long periods. That is especially true in niche sectors like RWA infrastructure, where sentiment can swing sharply.

Final Thoughts

Chintai is one of the cleaner examples of where crypto may be heading next: away from purely speculative tokens and toward blockchain systems that try to modernize actual capital markets. Its official positioning is less about hype and more about licensed tokenization infrastructure, compliant trading venues, custody, distribution, and full-lifecycle asset servicing. That gives the project a very different profile from many RWA tokens that focus mainly on narrative momentum.

CHEX, in turn, is designed as the utility layer behind that system. It is used for network resources, fee flows, staking rewards, and liquidity incentives, with a deflationary model and no future token releases stated on the official token page. If Chintai succeeds in becoming a meaningful infrastructure provider for compliant tokenized assets, CHEX could benefit from that growth. If adoption stalls, the token thesis weakens.

As the RWA sector continues to evolve, projects like Chintai (CHEX) are showing how blockchain can be used to bring regulated real-world assets on-chain. For traders looking to stay ahead of emerging crypto narratives—from RWAs and tokenization to AI and TradFi—Phemex offers a secure and user-friendly platform to explore the market, track new opportunities, and sharpen your trading edge.