Key Takeaways

Supply chain finance helps suppliers get paid earlier while allowing buyers to preserve longer payment terms.

Traditional supply chain finance systems are often slowed by paper-heavy workflows, fragmented data, reconciliation delays, and limited visibility across participants.

Blockchain can improve supply chain finance by creating a shared, tamper-resistant record of invoices, approvals, shipments, and payment obligations.

Smart contracts may help automate parts of financing, settlement, and compliance once predefined conditions are met.

The biggest promise of blockchain-based supply chain finance is not just speed, but better trust, transparency, and capital efficiency across global trade networks.

Adoption still faces real barriers, including integration challenges, legal complexity, privacy concerns, and the need for cooperation among many stakeholders.

Introduction

Global trade runs on trust, timing, and working capital. Goods move through factories, ports, warehouses, and distributors, but money does not always move at the same speed. That gap creates one of the most important functions in modern commerce: supply chain finance.

At its core, supply chain finance helps businesses manage payment timing more efficiently. Suppliers often want cash sooner. Buyers often want to pay later. Banks, fintech firms, and financing platforms step in to bridge the gap. When the system works well, suppliers improve liquidity, buyers optimize cash flow, and trade relationships become more stable.

But the traditional system is far from perfect. It often depends on siloed databases, manual verification, slow document handling, and inconsistent visibility across participants. In global trade, where a single transaction may involve manufacturers, logistics providers, customs agents, insurers, banks, and enterprise buyers, these inefficiencies add up quickly.

This is why blockchain has attracted so much attention in trade finance and supply chain finance. The promise is simple: if all relevant parties can share access to a trusted, synchronized record of commercial events, financing decisions could become faster, more transparent, and more reliable.

What Is Supply Chain Finance?

Supply chain finance refers to a group of financing solutions that improve cash flow between buyers and suppliers. The most common model works like this: a supplier delivers goods and issues an invoice, the buyer approves the invoice, and a financing provider pays the supplier early at a discount. The buyer then pays the full invoice amount later on the agreed due date.

This arrangement can benefit both sides. The supplier gets access to cash faster instead of waiting 30, 60, or even 90 days for payment. The buyer preserves working capital and avoids straining supplier relationships. In theory, everyone wins.

Supply chain finance is especially important for smaller suppliers. Large buyers often have stronger bargaining power and can push for longer payment terms. Smaller vendors may accept those terms to keep the business, but that can create cash-flow stress. If they need liquidity to buy materials, pay labor, or keep operations running, early-payment solutions become critical.

Over time, supply chain finance has grown into a major part of corporate treasury and trade-finance strategy. But its effectiveness depends heavily on information quality. Financing providers need confidence that invoices are real, approved, and tied to legitimate commercial activity. If the data is fragmented or difficult to verify, financing becomes slower, more expensive, or less accessible.

Why Traditional Supply Chain Finance Has Friction

Supply chain finance sounds straightforward in theory, but in practice it often suffers from operational friction.

One major problem is fragmented information. Different participants may each hold their own version of the truth. The buyer has one system. The supplier has another. The logistics firm has another. The financing provider may only see a narrow slice of the transaction. This makes reconciliation slow and increases the chance of error or dispute.

A second problem is manual processing. Many workflows still rely on document review, invoice matching, approval chains, and paper-based or semi-digital procedures. Even when systems are digitized, they are often not synchronized across institutions. That means staff still spend time verifying information that should already be trusted.

A third problem is fraud and duplication risk. If invoice data is not easily shared and verified across parties, there is greater risk of duplicate financing, fake documentation, or manipulated records. Financing providers may respond by increasing compliance checks, slowing approvals, or charging more for the risk.

A fourth issue is limited visibility. Supply chain finance works best when all parties can see key milestones clearly: order creation, shipment status, invoice issuance, buyer approval, financing status, and final payment. In reality, these events may sit in disconnected systems with different update cycles and permission rules.

All of this raises costs. It also slows access to liquidity, which is the exact problem supply chain finance is meant to solve.

What Blockchain Brings to Supply Chain Finance

Blockchain is often misunderstood as just a tool for cryptocurrencies. But the broader idea is more powerful: it is a shared ledger system that allows multiple parties to access a synchronized record of transactions or events without relying entirely on one central database.

For supply chain finance, this matters because the challenge is not only moving money. It is coordinating data among many parties who may not fully trust one another.

A blockchain-based supply chain finance system could record key events such as:

purchase order creation

shipment confirmation

goods receipt

invoice issuance

buyer approval

financing disbursement

final settlement

If these events are recorded on a shared ledger, authorized participants can see the same status in near real time. That reduces reconciliation problems and lowers uncertainty around what has actually happened.

The value is not that blockchain magically creates trust out of nothing. The value is that it can reduce dependence on fragmented bilateral recordkeeping. When commercial events are easier to verify across the network, financing providers may be more confident in advancing capital.

This is why blockchain is often described as an infrastructure upgrade for trade-related finance. It improves the credibility and visibility of the data that financing decisions depend on.

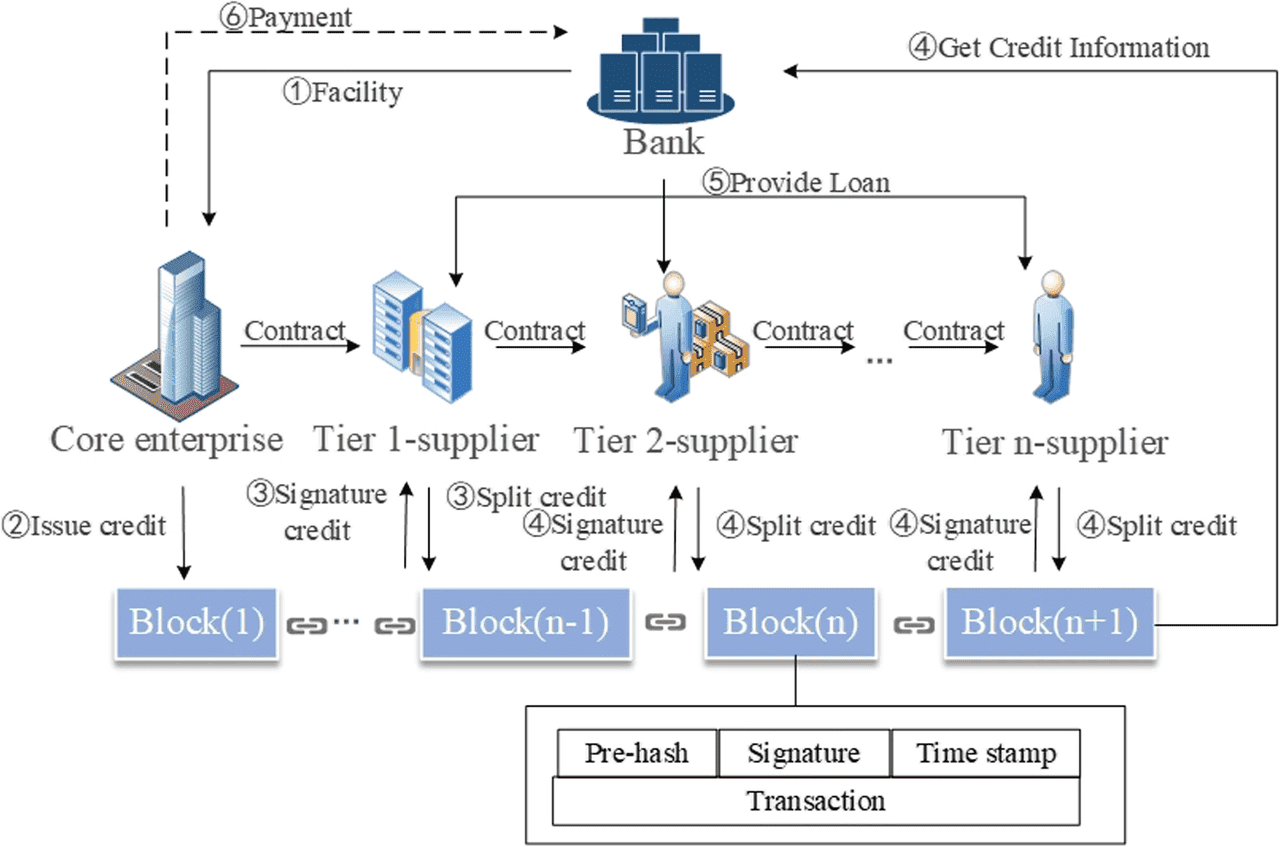

How a Blockchain-Based Supply Chain Finance Process Could Work

To understand the practical impact, imagine a manufacturer selling goods to a large retailer.

First, the retailer issues a purchase order. That event is recorded on a blockchain-based platform accessible to approved participants.

Next, the manufacturer ships the goods. Shipping confirmation and logistics milestones are added to the shared ledger. Once the goods arrive and the retailer confirms receipt, the invoice is issued and linked to the underlying transaction history.

At that point, the retailer approves the invoice. This approval is crucial because it reduces credit uncertainty. A financing provider reviewing the transaction can now see a chain of verified events: purchase order, shipment, delivery, invoice, and buyer approval.

Instead of requesting multiple manual confirmations from separate systems, the financing provider can rely on a shared record. That makes it easier to advance funds to the supplier earlier.

Finally, on the payment due date, the buyer settles the invoice. The ledger updates again, closing the financing cycle.

This model does not eliminate the need for legal contracts, risk assessment, or credit underwriting. But it can make the process more efficient by reducing information friction at every stage.

The Role of Smart Contracts

Blockchain becomes even more powerful in supply chain finance when paired with smart contracts.

A smart contract is a programmable agreement that executes certain actions automatically when predefined conditions are met. In supply chain finance, that could mean releasing financing once an invoice is approved, initiating payment once goods are confirmed delivered, or calculating discount rates based on payment timing.

For example, a smart contract could be written to say:

if the buyer approves the invoice

and shipment delivery has been verified

then release early payment to the supplier

and record the repayment obligation due from the buyer on a specified date

This kind of automation can reduce delays and manual intervention. It can also make workflows more predictable.

That said, smart contracts are only as useful as the data feeding them. If the underlying commercial information is wrong, incomplete, or manipulated before it reaches the chain, automation can simply accelerate bad outcomes. So smart contracts improve efficiency, but they do not remove the need for reliable inputs and good governance.

Why Transparency Matters So Much

One of blockchain’s biggest advantages in supply chain finance is shared visibility.

Traditional financing processes often involve trust gaps. A supplier may not know whether the financing provider has fully reviewed the invoice. A bank may not know whether the shipment information is current. A buyer may not know whether a supplier has already financed the same receivable somewhere else. These gaps create delays, disputes, and higher operational costs.

A shared ledger can reduce that uncertainty by making transaction status easier to verify. Not every participant needs access to every detail, but authorized parties can access the information relevant to them in a consistent format.

This transparency can improve invoice authenticity checks, duplicate-financing prevention, audit trails, settlement tracking, supplier confidence, and financier confidence. In global commerce, trust is expensive when it has to be rebuilt manually at every step. Blockchain can reduce that cost by making trusted records easier to share.

Benefits for Suppliers, Buyers, and Financing Providers

For suppliers

Suppliers gain faster access to cash. This can be especially valuable for small and medium-sized businesses that operate with tight working capital. Better visibility into invoice status may also reduce uncertainty about when financing will be available.

For buyers

Buyers can maintain healthy supplier relationships while preserving longer payment cycles. A more transparent system may also make internal approval and settlement processes easier to manage.

For financing providers

Banks and fintech lenders gain better visibility into transaction history and commercial milestones. That can improve underwriting confidence, reduce fraud risk, and make financing decisions faster.

For the broader ecosystem

If supply chain finance becomes more efficient, the whole trade network can benefit. Stronger liquidity at the supplier level can improve production reliability, reduce disruption risk, and support healthier long-term commercial relationships.

Tokenization and On-Chain Receivables

One of the more ambitious ideas in blockchain-based supply chain finance is the tokenization of receivables.

In simple terms, tokenization means representing a real-world financial claim on-chain. An approved invoice or receivable could, in theory, be turned into a digital token representing the right to payment. That token might then be financed, transferred, or used within a broader digital asset ecosystem.

This concept is part of the wider real-world asset trend in crypto. The idea is that claims on cash flows, invoices, trade receivables, or other assets can be represented digitally and managed more efficiently.

For supply chain finance, this could open the door to:

more programmable financing structures

broader capital-market access

faster settlement

secondary-market liquidity for receivables

more transparent audit trails

However, this is also where legal and regulatory complexity grows. A receivable is not just data. It is a legal claim shaped by contract law, jurisdiction, enforceability, and counterparty risk. Tokenization can improve operational handling, but it does not erase the legal realities behind the asset.

So the opportunity is real, but the implementation challenge is equally real.

The Biggest Challenges to Adoption

Despite the promise, blockchain-based supply chain finance is not a guaranteed transformation.

The first challenge is integration. Large enterprises already use ERP systems, banking interfaces, treasury platforms, and procurement software. Any blockchain solution has to fit into existing workflows rather than demand total replacement.

The second challenge is standardization. Supply chain finance involves many parties, often across borders. If each platform uses different data formats, rules, or permission structures, the coordination problem simply moves to a new layer instead of being solved.

The third challenge is privacy. Supply chains contain commercially sensitive information. Companies do not want every participant seeing pricing, volumes, counterparties, or financing terms unnecessarily. That means blockchain systems must balance transparency with permissioned access.

The fourth challenge is legal enforceability. Financial claims are ultimately governed by law, not by code alone. Smart contracts and tokenized invoices still need to align with legal frameworks, regulatory requirements, and dispute resolution mechanisms.

The fifth challenge is network effects. Blockchain-based supply chain finance works best when many stakeholders participate. But adoption is hard if each participant waits for others to move first. This chicken-and-egg problem is common in enterprise infrastructure transitions.

So while blockchain can improve supply chain finance, adoption will likely be gradual rather than sudden.

Why This Matters for Crypto and Financial Markets

Supply chain finance on the blockchain is not just a niche enterprise topic. It matters for crypto because it represents one of the clearest examples of how blockchain can support real-world economic activity beyond pure speculation.

For years, critics of crypto have asked what blockchain is actually good for outside trading digital assets. Supply chain finance offers a strong answer. It is a real business function involving real invoices, real counterparties, and real liquidity needs.

This is also why the topic connects naturally to the rise of real-world assets, stablecoins, and on-chain financial infrastructure. If trade receivables, payment obligations, and financing workflows move onto blockchain rails, they can interact with a broader digital financial system in new ways.

That does not mean every trade-finance workflow will migrate on-chain. But it does mean blockchain is becoming increasingly relevant wherever financial coordination and document trust are central problems.

The Bigger Picture

The deeper significance of blockchain in supply chain finance is that it changes how trust is organized.

Traditional systems often rely on bilateral verification, centralized recordkeeping, and repetitive reconciliation. Blockchain offers a different model: shared infrastructure, synchronized records, and programmable workflows.

That can make financing more efficient, but it can also do something more important. It can make trade networks more legible. When the movement of goods, approvals, invoices, and payments becomes easier to verify, financing becomes easier to structure.

In that sense, blockchain is not just digitizing supply chain finance. It is redesigning the information layer that supply chain finance depends on.

Conclusion

Supply chain finance exists to solve a timing problem in global commerce: suppliers need cash sooner, while buyers often want to pay later. Traditional solutions help, but they are often slowed by fragmented systems, manual processes, and limited visibility.

Blockchain offers a compelling upgrade because it creates a shared, verifiable record of commercial events. That can improve transparency, reduce reconciliation costs, support smarter automation through smart contracts, and make financing decisions faster and more reliable.

The opportunity is significant, especially as tokenization and on-chain real-world assets continue to grow. But the transition will not be simple. Integration, privacy, legal structure, and network coordination all remain major challenges.

So the most realistic takeaway is this: supply chain finance on the blockchain is not a silver bullet, but it could become one of the most practical and important real-world uses of blockchain infrastructure.