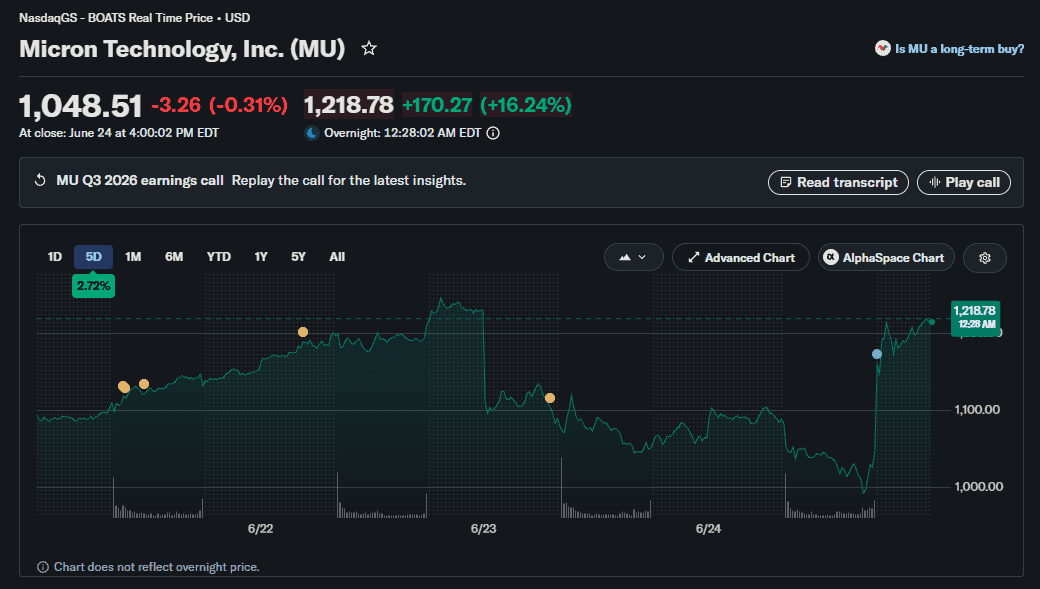

Micron reported its fiscal Q3 2026 results (the quarter covering calendar March to May 2026) after the close on June 24, 2026, and the print itself was strong. Revenue and earnings both beat expectations, management reiterated that its high-bandwidth memory is sold out through 2026, and the demand commentary around AI memory stayed as tight as the bulls hoped. Then the stock fell off a cliff. MU is trading near $1,048.51, down 13.44% on the day, after a trailing-year run of roughly 830% that had priced the company close to perfection.

That is the puzzle worth solving. A memory maker beats, says its hottest product is fully booked, and the market dumps it double digits in a single session. The answer is not in the headline numbers. It is in what the stock had already paid for, what the forward guidance said, and how the broader tape was positioned the day the report landed. For the longer-horizon view on the same name, our Micron MU stock price prediction walks through the 2026 to 2030 case.

- MU price: $1,048.51 after the post-earnings session

- 24-hour move: down 13.44%, one of the sharpest single-day drops of the year for the stock

- Trailing-year context: roughly an 830% run into the print, which set the bar near perfection

- HBM status: sold out through 2026, with allocation conversations already moving to HBM4

- Guidance focus: gross-margin trajectory, where analysts wanted a clear path toward the ~84% zone

The stock did not crash because the business is weak, and the broader memory and AI-semiconductor complex was sliding with it, where peers like NVIDIA at $200.22 drifted lower into a risk-off tape rather than catching a bid on Micron's demand commentary. Here is what actually happened and what a trader watches from here.

Why a Clear Earnings Beat Still Crashed the Stock

The simplest way to understand this selloff is the phrase traders use for exactly these setups. The stock was priced for perfection, a level our Micron and the trillion-dollar club overview tracked as the run extended. When an asset has run roughly 830% in a year and trades at a valuation that already assumes years of flawless execution, beating the current quarter is not enough. The beat is the assumption, not the surprise. To rally from there, the company has to beat AND raise the ceiling on what the market thought was possible, and a solid in-line-to-better guide simply does not clear that bar.

This is the same mechanical setup that punishes crowded trades after a catalyst, the way Bitcoin tends to sell off after an expected Fed decision. The event removes the uncertainty premium. Everyone who wanted to be long ahead of the print already was, and once the result confirms the consensus story without blowing past it, the marginal buyer disappears and the crowded long side unwinds. A great quarter from a stock priced for a perfect quarter produces a selloff, not a rally.

The macro backdrop made it worse. Micron reported into a broad risk-off session where money was rotating out of the highest-beta AI and memory names rather than into them. On a green tape, a strong Micron print with HBM sold out might have been bought. On a red tape with traders trimming the most extended winners, it became a reason to take profit on an 830% move. The stock did not move in isolation. It moved with a market that was already looking for an excuse to de-risk the most crowded corner of the AI trade.

What Micron's Guidance Actually Said

The number that decided the reaction was not revenue or EPS. It was the forward gross-margin guide. Memory is a margin story above almost anything else, because the same wafer can earn wildly different profit depending on product mix and pricing. Analysts going into the print wanted to see a credible path toward the ~84% gross-margin zone, treating that as the bogey for one question. Was HBM richness still expanding the margin profile, or starting to plateau.

Frame ~84% correctly. It is the analyst expectation and target, not a figure Micron stamped on a slide as a hard commitment. When a stock is priced for perfection, the gap between what analysts modeled and what management actually guided becomes the entire trade. If the guide pointed toward that zone with full conviction, the stock probably holds. If it left the path ambiguous, or framed the next leg of margin expansion as dependent on mix and timing rather than a sure thing, that ambiguity is enough to crack an extended stock. The reaction tells you which way the read landed.

The second forward variable was HBM4 allocation. HBM being sold out through 2026 is the bull's favorite line, but "sold out" is a known quantity already baked into the price. The live question is HBM4, the next generation, and how much of that capacity Micron has locked with which customers at what pricing. Allocation commentary that sounded merely solid rather than dominant gives the bear case its opening. The market had already paid for sold-out HBM. It wanted to be paid forward on HBM4, and a measured tone there does not satisfy a perfection valuation.

The Bull Case Versus the Bear Case on Micron

Both sides of this stock are credible right now, which is exactly why the move was violent. The bull case rests on structural tightness. The bear case rests on valuation and cycle history. Here is how they line up.

|

Factor

|

Bull case

|

Bear case

|

|

HBM demand

|

Sold out through 2026, AI memory structurally tight

|

Already fully priced, no upside surprise left

|

|

Gross margin

|

Mix shift toward HBM keeps expanding margins

|

Path toward ~84% looked ambiguous, not guaranteed

|

|

Valuation

|

Justified by multi-year AI memory cycle

|

Priced for perfection after an 830% run

|

|

Cycle

|

This time the AI demand floor is higher

|

Memory is cyclical and fear of a peak is rational

|

|

HBM4

|

Next leg of growth and pricing power

|

Allocation commentary sounded solid, not dominant

|

The bull case is straightforward. AI accelerators need enormous amounts of high-bandwidth memory, supply is constrained, and Micron is one of only three companies on earth that can make it at scale alongside rivals like Samsung. If that tightness holds into HBM4, today's drop is a discount on a structural winner. The honest version of the bull thesis is that the business is fine and the stock got ahead of itself, so a sharp reset in price without a reset in fundamentals is a gift. The detail behind the numbers sits in Micron's own investor relations materials and the filings on SEC EDGAR.

The bear case is equally honest. Memory has always been cyclical, and every cycle in history eventually peaked while everyone insisted that this time the demand was permanent. An 830% run prices in years of flawless margin expansion, and the moment the gross-margin path looks anything less than certain, the stock has enormous room to fall just on multiple compression. The bear does not need the business to break. The bear only needs the perfection premium to deflate, and a single ambiguous guidance line was enough to start that.

What a Trader Watches Next on MU

The first thing to watch is how clearly the gross-margin path gets clarified on the earnings call and in the analyst notes that follow. If the ~84% trajectory firms up in the commentary and the sell-side keeps its margin estimates intact, the drop reads as a valuation reset on a still-healthy business. If estimates start coming down, the selloff has further to run because the perfection premium has not finished deflating.

The second is the broader AI-semiconductor tape, because Micron does not trade alone. Watch how NVDA near $200.22, custom-silicon names like Marvell, and the rest of the memory and accelerator complex behave, because they either stabilize or keep leaking, because a stock that fell partly on rotation needs the rotation to stop before it can base. Live quotes are easy to track on the MU market page on Google Finance. If the whole group keeps bleeding, Micron's strong fundamentals will not save the price in the short term.

The third is HBM4 headlines. Any concrete allocation win, a named multi-year supply agreement, or pricing confirmation for the next-generation product directly attacks the bear thesis. The bear case leans on the idea that the next leg is not locked in. Evidence that it is locked in is the cleanest catalyst for the stock to reclaim what it gave back.

Frequently Asked Questions

Why did Micron stock crash if it beat earnings?

Because it was priced for perfection. After a roughly 830% trailing-year run, the market had already assumed a strong beat, so beating the quarter was not a surprise. A solid-but-not-spectacular forward guide on gross margin, into a broad risk-off tape, was enough to trigger profit-taking that pushed MU down 13.44% to $1,048.51.

What does priced for perfection mean for a stock like MU?

It means the valuation already assumes years of flawless execution, so good news is the baseline rather than a catalyst. To rally, the company has to exceed expectations that were already extremely high. When results merely meet that bar, the crowded long side unwinds and the stock can fall hard even on a genuinely strong report.

Is Micron's HBM really sold out through 2026?

Yes, management reiterated that its high-bandwidth memory is sold out through 2026, which reflects real structural tightness in AI memory. The catch is that this fact was already widely known and priced in, so it provided no fresh upside. The market's attention has shifted to HBM4 allocation and pricing for the next cycle.

Does the Micron crash mean the AI memory boom is over?

Not necessarily. The selloff was driven more by valuation and positioning than by any sign that AI memory demand is weakening. Memory is cyclical, so peak fear is rational, but the drop is best read as a perfection premium deflating rather than confirmation that the boom has ended.

Bottom Line

Micron crashed because a great quarter is not enough when the stock is priced for a perfect one. If the gross-margin path toward ~84% firms up on the call and sell-side estimates hold, the drop to $1,048.51 reads as a valuation reset on a healthy business and the structural HBM thesis is intact. If margin estimates start falling and the broader AI-semiconductor complex keeps leaking with NVDA near $200.22, the perfection premium has more to deflate and the next support test comes lower. Watch the margin commentary first, the group tape second, and HBM4 allocation headlines third. The business looks fine. The price had simply run too far ahead of it.

This article is for informational purposes only and does not constitute financial or investment advice. Cryptocurrency trading involves substantial risk. Always conduct your own research before making trading decisions.