Key Takeaways

-

Usual is a stablecoin and governance ecosystem built around USD0, a dollar stablecoin backed by U.S. Treasury Bills, and EUR0, a euro stablecoin backed by EU Treasury Bonds.

-

USUAL is the protocol’s governance and ownership token, and Usual says it represents rights to 100% of protocol revenue.

-

The ecosystem includes yield and credit products such as USUALx, bUSD0, and UZR, expanding Usual beyond a simple stablecoin issuer into a broader DeFi-native yield and credit platform.

-

Usual’s core value proposition is that stablecoin yield from real-world collateral should accrue to users and token holders rather than only to the issuing company.

-

As of April 2026, the protocol is actively evolving, with recent developments including USUALx unlock mechanics, new collateral proposals, EUR0 banking rails, and the rollout of UZR and related credit products.

Stablecoins have become one of crypto’s most important product categories, but most people still think of them in fairly simple terms: a token pegged to a dollar, backed by reserves, and used for trading or payments. Usual is trying to push that model further. According to its official documentation, Usual is a protocol built around a stablecoin and governance system where the ecosystem’s value and revenue are distributed to users and the community rather than captured mainly by a centralized issuer. Its docs frame this as making “money a public good,” with a product suite including USD0, EUR0, USUAL, USUALx, and bond or credit products such as bUSD0 and UZR.

At the center of the protocol is USD0, which Usual describes as its core stablecoin, fully backed by U.S. Treasury Bills, and designed for payments, trading, and collateral use across DeFi. The same docs describe USUAL as the governance and ownership token representing rights to 100% of protocol revenue, with value flowing primarily from the real-world yield generated by the Treasury collateral backing USD0.

That makes Usual different from many stablecoin projects. Instead of issuing a stablecoin and keeping most of the economics at the company level, Usual’s stated goal is to route the protocol’s value, governance, and treasury upside to the tokenized community layer. In simple terms, Usual is trying to combine a yield-bearing RWA-backed stablecoin system with a governance token that is explicitly tied to real protocol cash flows.

What Is Usual?

Usual is a crypto protocol focused on stablecoins, real-world-yield distribution, governance, and onchain credit. Its official docs say the ecosystem currently includes:

-

USD0 as the core stablecoin,

-

EUR0 as the euro stablecoin,

-

USUAL as the governance and ownership token,

-

and additional products such as USUALx, bUSD0, and related vault or credit primitives.

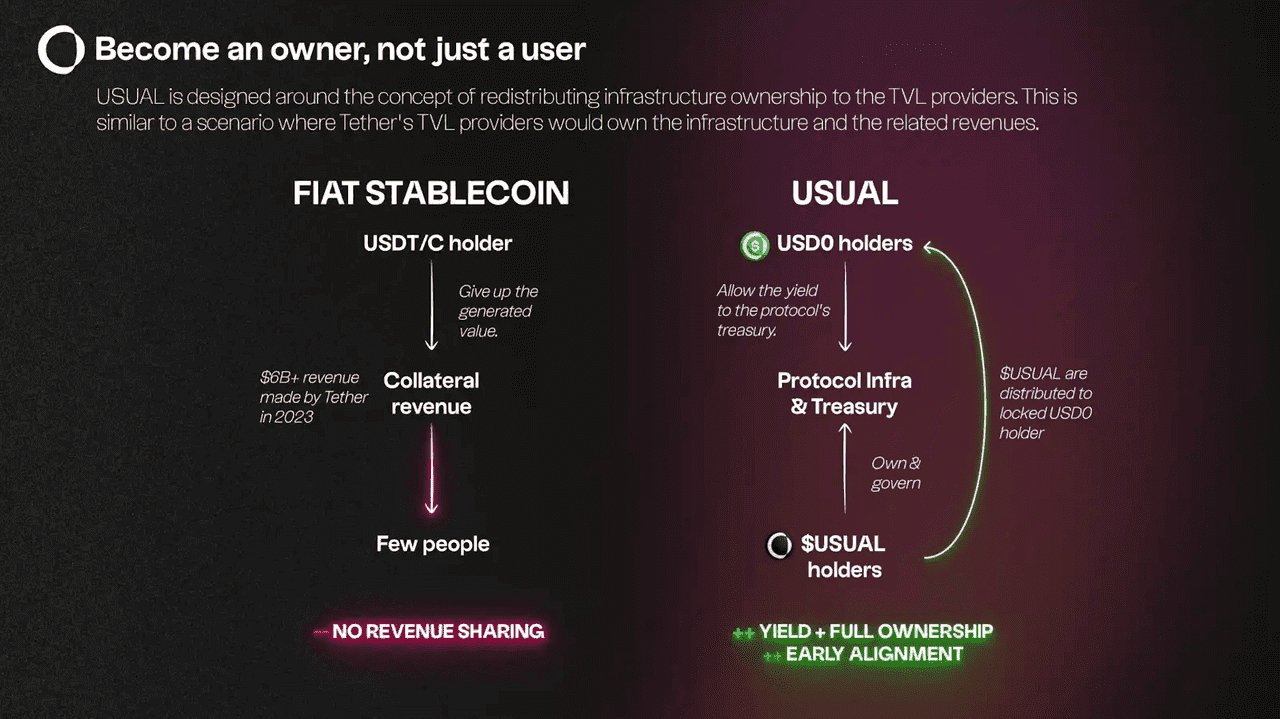

The project’s “Why Usual?” page makes the central claim very clearly: the goal is to make users the owners of the protocol’s infrastructure, treasury, and governance through the USUAL token, with 100% of the protocol’s value distributed to the USUAL holder and community. It adds that revenue flows from the real-world yield on U.S. Treasury Bill collateral backing USD0, creating sustainable cash flows intended to support the token’s value.

That positioning matters because it separates Usual from two other common models in crypto:

First, it is not just a governance token with vague narrative value. The docs repeatedly tie USUAL to real protocol revenue. Second, it is not just a stablecoin with no community upside. The protocol is explicitly designed so that the governance layer shares in the economics generated by the stablecoin system.

This is why Usual often gets discussed in the overlap between RWA-backed stablecoins, protocol-owned value, and governance tokens backed by real cash flow rather than pure speculation.

What Problem Is Usual Trying to Solve?

The basic Usual critique is that most stablecoin systems are economically unbalanced.

In the traditional stablecoin model, users provide the demand and liquidity, but the issuer usually keeps most of the benefit generated by the reserves. If a stablecoin is backed by U.S. Treasury Bills, for example, the yield on those assets can become a large and very stable business line for the issuer. Usual’s docs explicitly argue that users and the community should own that infrastructure and receive its value rather than leaving the economics concentrated at the top.

USUAL is revenue-backed, not speculation-backed, and that yield generated by USD0’s collateral flows to USUAL holders through a Revenue Switch that distributes protocol earnings weekly in USD0 to stakers.

So the problem Usual is trying to solve is not just “how do we launch another stablecoin?” It is closer to:

-

how do you issue a stablecoin backed by high-quality real-world assets,

-

how do you route the economics of that system to the community,

-

and how do you build additional yield and credit products around it?

That broader framing is what makes Usual more than a simple payments token.

How Usual Works

The easiest way to understand Usual is to break it into three layers:

-

the stablecoin layer,

-

the governance and value-accrual layer,

-

and the yield/credit product layer.

-

The Stablecoin Layer: USD0 and EUR0

The foundation of the ecosystem is USD0. Usual’s docs describe it as the core stablecoin, fully backed by U.S. Treasury Bills, and usable for payments, trading, and DeFi collateral. The docs also list EUR0 as the euro-denominated stablecoin, fully backed by EU Treasury Bonds.

This is important because the backing model is central to Usual’s identity. The project is not presenting itself as an algorithmic stablecoin, nor as a purely crypto-collateral stablecoin. It is positioning itself squarely in the real-world-asset-backed stablecoin category.

The recent EUR0 banking-rail announcement reinforces this direction. In its January 2026 blog post, Usual said users could move from a bank account to EUR0 without an exchange, calling the EUR ↔ EUR0 rail the first banking connection and signaling that more currencies and rails will follow. That indicates the project is trying to bridge onchain stablecoins and traditional finance more directly over time.

-

The Governance and Ownership Layer: USUAL

The next layer is USUAL, which the docs describe as the protocol’s governance and ownership token. The official governance-token page says USUAL represents ownership of 100% of protocol revenue and is backed by real cash flows, primarily the yield generated by the U.S. Treasury Bills backing USD0.

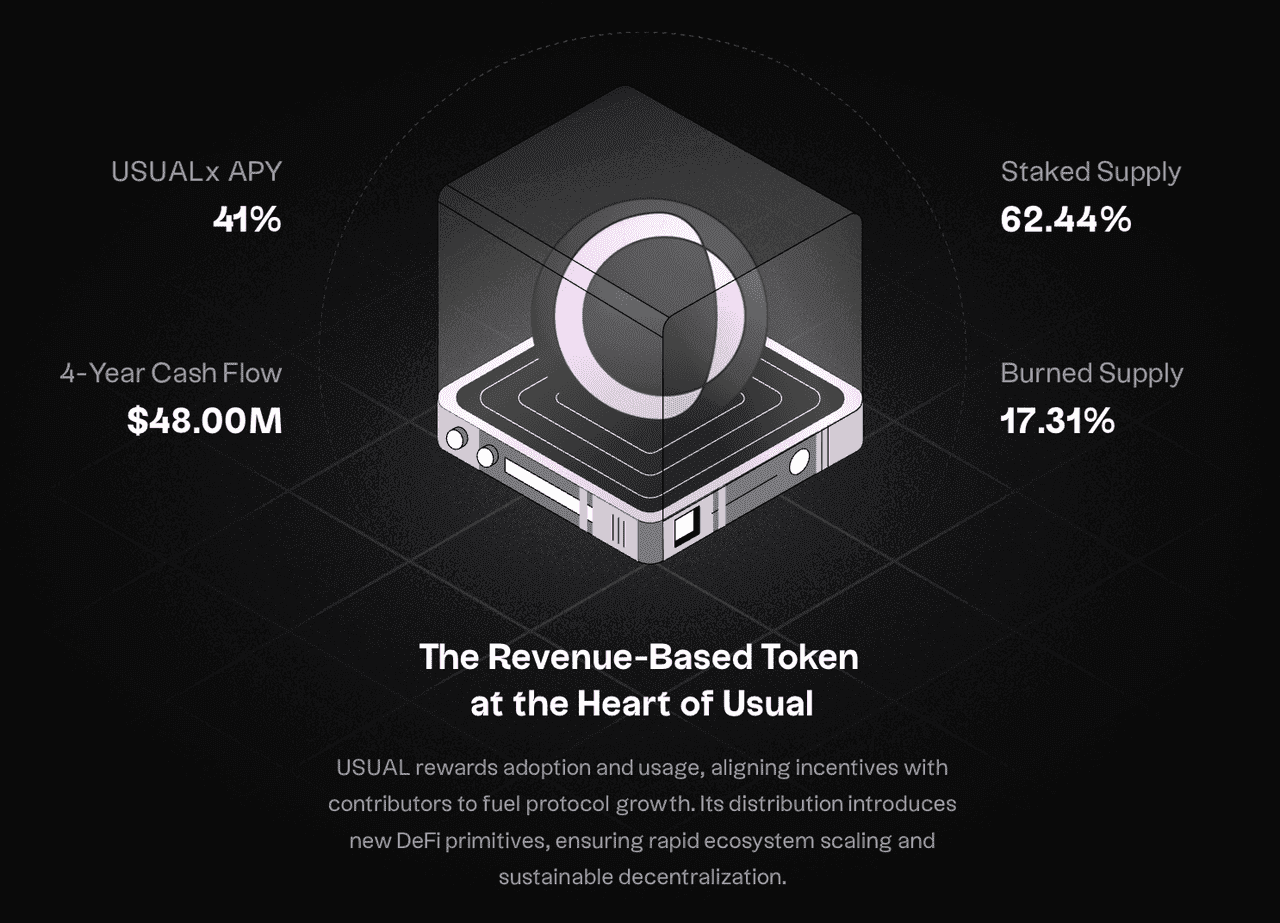

That is one of the boldest claims in the project. It means the governance token is not just supposed to vote on parameters. It is meant to represent an economic claim on the protocol’s revenue. The docs further say the Revenue Switch distributes protocol earnings weekly in USD0 to stakers, which creates a direct line between underlying reserve yield and token-holder incentives.

Usual’s governance docs also explain that the protocol is designed to progressively decentralize, starting with more structured safeguards and moving toward community-led DAO control over time. That is a common pattern in newer protocols, but here it matters especially because the governance layer is explicitly tied to value capture and treasury control.

-

The Staked Governance Layer: USUALx

Usual also has USUALx, a staked or locked version of the governance token. While the full token mechanics are spread across product pages and announcements, the January 2026 blog post made clear that USUALx has an unlock window process rather than constant instant liquidity.

This suggests USUALx is designed as a more committed version of governance participation, likely intended to align long-term holders more tightly with the protocol’s economics and governance direction.

That matters because protocols tied to real cash flow often need ways to distinguish between short-term trading demand and longer-term governance-aligned staking. USUALx appears to be part of Usual’s answer to that issue.

What Is USD0?

USD0 is the core stablecoin of the Usual ecosystem. According to the docs, it is fully backed by U.S. Treasury Bills and is intended for payments, trading, and DeFi collateral.

This makes USD0 part of the growing category of stablecoins that try to combine:

-

dollar stability,

-

real-world reserve backing,

-

and DeFi composability.

USD0 is therefore not only meant to function as a stable medium of exchange. It is also the reserve and collateral base from which the rest of the ecosystem’s economics flow. Treasury-backed collateral generates yield, and that yield becomes the economic engine behind USUAL’s governance-token value proposition.

What Is USUAL?

USUAL is the protocol’s governance and ownership token. Official docs say it represents rights to 100% of protocol revenue, with that value primarily arising from the yield on the U.S. Treasury collateral backing USD0.

This positioning is what makes Usual stand out in a crowded governance-token market. Many governance tokens promise future ecosystem value without clearly defined economic links. Usual’s docs are much more direct: the token is meant to be revenue-backed by stable, real-world yield.

That does not guarantee market performance, of course. But it does provide a clearer economic thesis than many governance tokens have. Instead of relying mainly on narrative or inflationary incentives, Usual is trying to anchor token value to recurring protocol earnings.

What Is bUSD0?

One of Usual’s more interesting newer products is bUSD0, also called Bond USD0. The docs describe bUSD0 as the bonded, yield-bearing form of USD0. It works like a liquid bond: USD0 is locked until a fixed maturity date, while daily USUAL token rewards are distributed to bUSD0 holders as “coupons.” The docs also say bUSD0 is the first bond token in the Usual ecosystem.

This matters because it shows Usual expanding beyond a simple stablecoin/governance-token pair into structured onchain fixed-income-like products. In effect, the protocol is turning stablecoin capital into a bond-like instrument with a maturity profile and reward distribution.

That makes bUSD0 a bridge between:

-

stablecoins,

-

protocol incentives,

-

and yield products modeled more like fixed-income instruments than ordinary DeFi LP tokens.

For users, the simplest description is that bUSD0 is a way to lock USD0 into a more structured yield profile while receiving ongoing USUAL rewards.

What Is UZR?

Another major step in the ecosystem’s evolution is UZR, or Usual Zero Rate. In its January 2026 blog post, Usual described UZR as a native credit primitive for USD0. The announcement said UZR makes USD0 working capital through zero-rate borrowing, protocol-owned credit via Fira, and bUSD0 as a zero-coupon bond.

That is a notable shift because it moves Usual beyond the “stablecoin + governance token” model into onchain credit infrastructure. If USD0 is the reserve base, then UZR appears to be part of the protocol’s attempt to turn that reserve base into a more active credit and capital-market layer.

In other words, Usual is trying to build not just money, but also credit primitives around that money. That is strategically important because many successful financial ecosystems are not built only on stable assets. They are built on the ability to use those assets for borrowing, lending, structuring, and investment. UZR suggests Usual wants to move in that direction.

Recent Usual Developments as of April 2026

As of April 2026, several recent developments help show where the protocol is going.

One is the USUALx unlock window, announced in January 2026, which shows the governance layer maturing and introducing more structured staking/unlocking mechanics.

Another is EUR0 and its first banking connection. Usual’s January 2026 blog said users could move from a bank account to EUR0 without needing an exchange, and that more rails and currencies would follow. That suggests the protocol is trying to broaden from dollar exposure into euro-denominated stablecoin infrastructure as well.

A third is UZR, announced in January 2026 as a native credit primitive for USD0. That points to a strategic move from reserve-backed stablecoin issuance into more complete onchain credit architecture.

Finally, governance proposals around collateral continued into late 2025 and early 2026, including UIP-14 and UIP-16, which proposed adding assets such as USTBL and U0R as USD0 collateral. That shows the collateral and risk framework is still actively evolving through governance.

Risks and Limitations

The first risk is execution risk. The protocol is trying to do several things at once: stablecoin issuance, governance value accrual, staked-governance mechanics, bond products, and credit primitives. Ambitious financial ecosystems can create upside, but they also become more complex to manage. This is an inference based on the product suite described in the docs and blog.

The second risk is governance and design risk. Because USUAL is directly tied to protocol revenue and governance, token design choices matter a great deal. Unlock windows, staking alignment, and reward-routing mechanics can all materially affect incentives.

The third risk is collateral and regulatory risk. USD0 and EUR0 depend on high-quality real-world collateral and the legal/operational infrastructure that supports those assets. Treasury-backed stablecoins are generally seen as safer than algorithmic ones, but they still rely on custody, legal structure, and regulatory durability. This is an inference from the product model and not a specific project warning.

The fourth risk is token-capture risk. Even though the docs clearly state that USUAL represents 100% of protocol revenue, the market may still price the token differently from that theoretical value, especially in early-stage or evolving ecosystems. Revenue-backed does not automatically mean fairly valued. This is an inference based on how crypto markets behave more broadly.

Conclusion

Usual is one of the more interesting stablecoin projects in crypto because it is trying to solve a real structural issue: who captures the value created by reserve-backed money?

Its answer is to build a system where:

-

USD0 provides the Treasury-backed stablecoin base,

-

USUAL captures governance and revenue rights,

-

USUALx strengthens long-term governance alignment,

-

and products like bUSD0 and UZR extend the ecosystem into structured yield and credit.

That makes Usual more than just another stablecoin issuer. It is an attempt to build a community-owned financial protocol around real-world yield.

As stablecoins, RWAs, and onchain credit continue to evolve, projects like Usual show how crypto can repackage traditional reserve assets into more community-owned financial infrastructure. For traders looking to stay ahead of emerging narratives—from stablecoins and RWAs to PayFi, AI, and onchain credit—Phemex offers a secure and user-friendly platform to explore the market, monitor new opportunities, and sharpen your trading edge.