Key Takeaways

-

Goldfinch is a protocol focused on bringing real-world finance, especially private credit, on-chain.

-

Its flagship current product is Goldfinch Prime, which Goldfinch says gives non-U.S. investors access to diversified institutional private-credit funds from managers like Ares, Apollo, and Golub.

-

GFI is Goldfinch’s official token and governance token.

-

Goldfinch’s earlier protocol identity was built around crypto lending without crypto collateral, using off-chain assets and borrower pools instead of standard overcollateralized DeFi mechanics.

-

As of May 2026, Goldfinch is best understood not just as a DeFi lending protocol, but as an RWA/private-credit access platform with a stronger institutional-facing product layer than many earlier DeFi credit projects.

Private credit has become one of the most important financial trends of the decade, but for most people it has historically remained difficult to access. Traditional private-credit funds often come with high minimums, limited liquidity, complex paperwork, and distribution channels aimed mainly at institutions and high-net-worth investors. Goldfinch is a crypto project built around the idea that blockchain infrastructure can make this market more accessible, transparent, and globally available. Goldfinch’s official site currently describes Goldfinch Prime as giving investors on-chain access to diversified institutional-grade private credit funds from firms such as Ares, Apollo, and Golub.

That positioning matters because Goldfinch is no longer just a theoretical “real-world lending” protocol. Its current public docs frame the project as a bridge between crypto rails and large private-credit managers. Goldfinch says its mission is to bring real-world finance on-chain, and that Goldfinch Prime represents the next phase of that mission by packaging major private-credit funds into a simpler on-chain investment experience.

The project’s native token is GFI, which Goldfinch’s docs describe as the official token of the protocol and its governance token. Older but still official Goldfinch documentation says GFI is used for community governance and has historically also been tied to staking, rewards, and protocol participation. Developer docs still identify GFI as Goldfinch’s governance token on Ethereum.

What Is Goldfinch?

Goldfinch is a crypto protocol focused on bringing real-world credit on-chain. In community and official documentation, Goldfinch has long described itself as a decentralized credit protocol that enables loans backed by off-chain assets, rather than requiring borrowers to overcollateralize loans with crypto. That original design was meant to make decentralized finance useful for real businesses rather than only for crypto-native traders recycling digital collateral.

Today, Goldfinch’s public messaging has evolved. The most prominent front-end product is now Goldfinch Prime, which the official docs describe as on-chain access to diversified private-credit funds managed by some of the largest names in the asset class. Goldfinch says these firms collectively manage over $1 trillion in assets and that Prime makes this exposure available globally in a low-cost way through stablecoins and blockchain rails.

That makes Goldfinch an interesting hybrid. It still comes from the DeFi and on-chain credit world, but it increasingly presents itself as an access layer for institutional-grade private credit rather than only a protocol for direct decentralized borrower pools. In other words, Goldfinch has shifted from “on-chain credit for real-world borrowers” toward “on-chain access to major private-credit strategies.” That is an inference, but it follows directly from the contrast between the older overview documents and the current Prime-focused materials.

What Problem Is Goldfinch Trying to Solve?

Goldfinch is trying to solve a very old finance problem and a very modern crypto problem at the same time.

The old finance problem is access. Private credit has historically been attractive because it can offer yield and diversification, but it has typically been reserved for institutional and wealthy investors. Goldfinch’s FAQ says private credit has long been an attractive asset class for institutions and HNWIs, and that Goldfinch Prime is designed to expand access to diversified, high-quality private credit on-chain.

The modern crypto problem is capital efficiency and real-world relevance. Traditional DeFi lending protocols generally require borrowers to overcollateralize loans with crypto assets. Goldfinch’s older documentation explicitly criticized that model, arguing it excludes most real-world borrowers and limits DeFi’s usefulness outside crypto-native speculation. Goldfinch’s early community docs say the protocol was designed so borrowing could be supported by off-chain assets and real-world business activity.

How Goldfinch Works Today

The easiest way to understand Goldfinch in 2026 is to break it into two layers:

-

the original protocol and borrower-pool identity

-

the newer Goldfinch Prime product layer

-

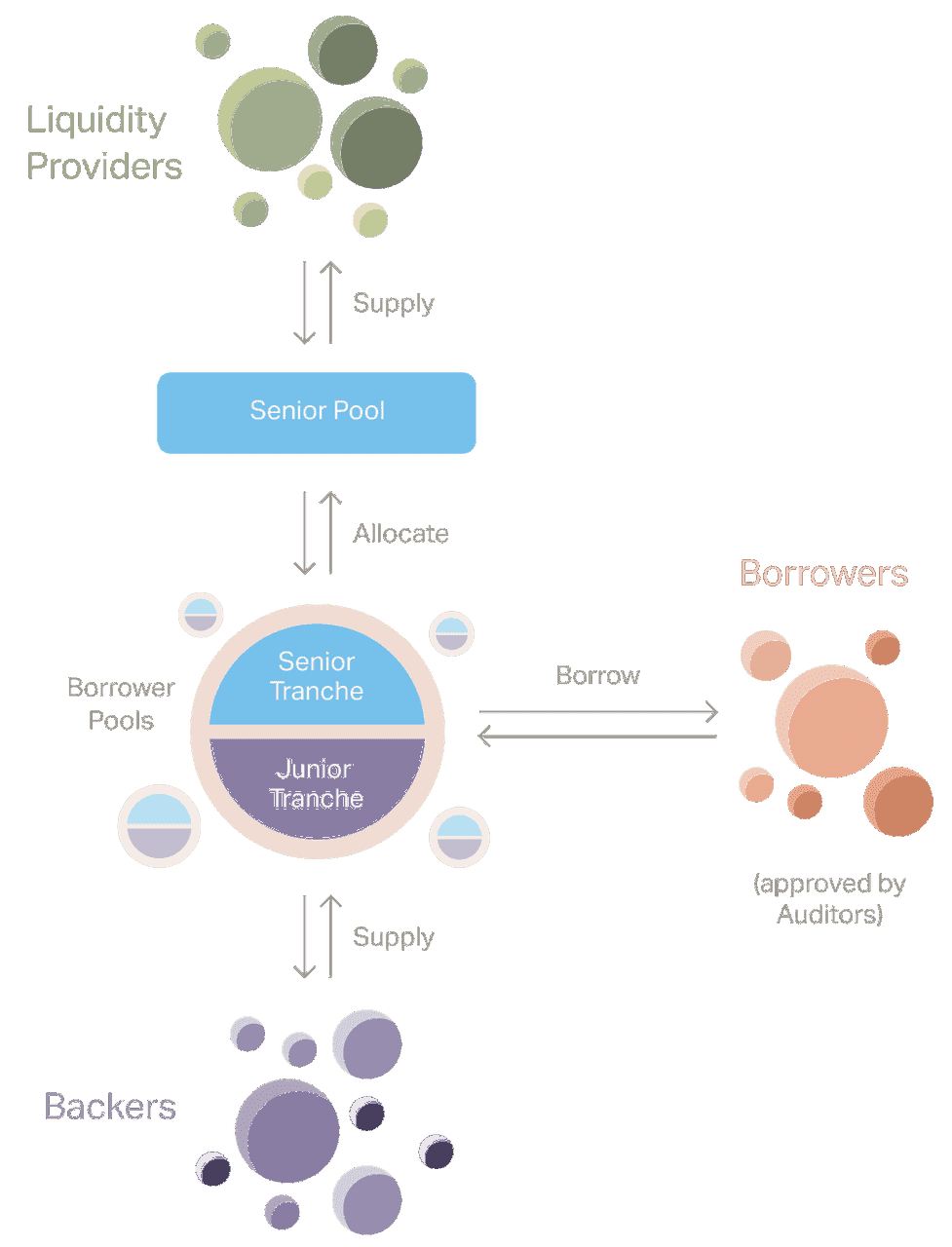

The Original Goldfinch Protocol

Goldfinch’s older documentation describes a protocol built around Borrower Pools, where borrowers could raise capital from the protocol under encoded financing terms such as interest rates and repayment schedules. A related protocol role structure included borrowers, backers, and auditors, with GFI helping coordinate governance and incentives. The whitepaper summary also describes GFI as being used for governance votes, auditor staking, auditor rewards, staking on backers, and other ecosystem rewards.

Community documentation summarizes the original protocol design more directly: Goldfinch allowed borrowing without crypto collateral, with loans instead fully collateralized by off-chain assets. That made it one of the clearest early DeFi attempts to connect lending markets to real businesses rather than purely on-chain collateral loops.

This is important because it explains Goldfinch’s roots. The project did not start as a tokenized fund wrapper. It started as a decentralized credit protocol trying to solve off-chain lending with on-chain coordination.

-

Goldfinch Prime

Goldfinch Prime is the clearest current expression of the project. Goldfinch’s homepage says Prime gives investors access to “multi-billion dollar private credit funds” from managers like Ares, Apollo, Golub, and more, in one on-chain pool. The docs call Prime “the next evolution” of the mission and say it brings the biggest and best private-credit funds in the world on-chain in one simple, diversified investment.

Goldfinch’s FAQ adds that Prime offers non-U.S. investors exposure to private credit through an on-chain structure and explicitly emphasizes diversified private-credit access. That non-U.S. qualifier is important because it signals the product is jurisdiction-aware and not globally permissionless in the simple DeFi sense.

So if the original protocol was about enabling real-world borrowing through decentralized lending structures, Goldfinch Prime is about curating access to established private-credit funds in a more accessible on-chain format.

What Is Goldfinch Prime?

Goldfinch Prime is Goldfinch’s flagship investment product for private credit. The official docs say it offers on-chain access to high-quality, diversified private credit, while the homepage markets it as access to funds from major firms like Ares, Apollo, and Golub.

The FAQ explains the investment case in more practical terms: Prime is designed to expand access to a private-credit asset class that has historically been attractive to institutions and wealthy individuals, but difficult for a broader audience to reach.

A few important things follow from this:

-

Prime is not just a random yield farm.

-

It is not the same thing as direct lending into a single borrower pool.

-

It is positioned more like a structured gateway to diversified private-credit strategies.

That makes Goldfinch Prime especially relevant to the RWA conversation. A lot of RWA projects tokenize cash-like instruments or Treasury exposure. Goldfinch is reaching into a different part of the market: institutional private credit.

What Is Private Credit, and Why Does Goldfinch Focus on It?

Private credit refers to loans or credit strategies that are not issued or traded on public markets. Goldfinch’s docs define it this way and explain that it often involves non-bank lenders providing capital to businesses or loan pools.

This matters because private credit has become one of the fastest-growing segments in finance. While the exact scale of the market depends on the source and methodology, major financial commentary widely treats private credit as a major and expanding institutional asset class. Goldman Sachs’ March 2026 perspective said private credit fundamentals appeared resilient and that the market had become a significant part of the financial system.

Goldfinch focuses on private credit because it offers a strong fit for on-chain distribution:

-

it is yield-oriented

-

it is usually hard to access

-

it benefits from better transparency and simplified investor rails

-

and it offers exposure to real economic activity rather than only crypto-native leverage

That makes it a natural category for tokenized and on-chain finance.

What Is GFI?

GFI is the official token of Goldfinch. Goldfinch’s own documentation says this directly, and developer docs still identify it as Goldfinch’s governance token deployed on Ethereum mainnet.

The official token documentation says GFI is used for community governance, meaning GFI holders can participate in decisions about the direction of the protocol. The older whitepaper summary adds more detail, describing GFI as tied not only to governance votes but also to auditor staking, auditor vote rewards, staking on backers, and early backer incentives.

This is useful context because it shows that GFI’s role has historically been broader than a passive governance label. It has been part of the incentive design of the protocol, especially around participation, staking, and aligned behavior.

As of May 2026, GFI remains publicly tracked as Goldfinch’s governance token on major platforms such as Coinbase and MetaMask. Coinbase describes GFI as the Ethereum token that governs Goldfinch, a decentralized credit protocol for extending loans to real-world businesses.

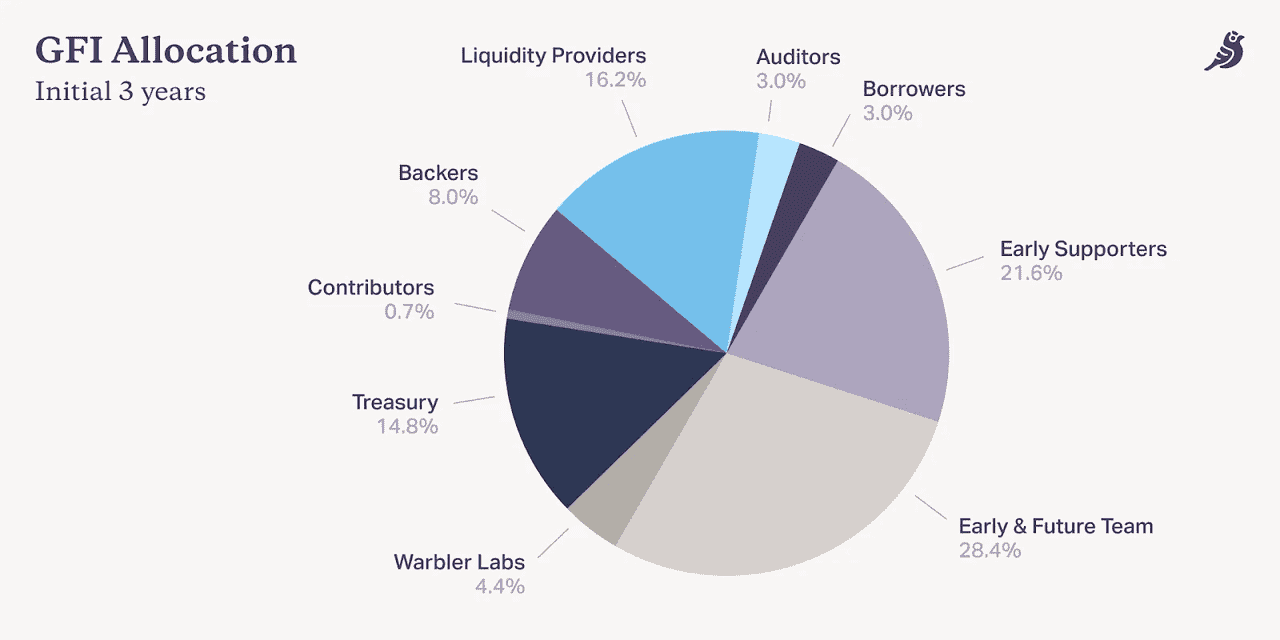

GFI Allocation (source)

What Does GFI Do?

The safest answer, based on current official sources, is that GFI is primarily the governance token of the Goldfinch ecosystem. Goldfinch’s official token page says GFI is used for community governance, and the developer docs confirm this identity.

From older but still official documentation, GFI has also been tied to:

-

auditor staking

-

auditor vote rewards

-

staking on backers

-

early backer rewards

-

and potential other rewards across the protocol

That means GFI has historically served as both:

-

a governance asset

-

and an incentive/co-ordination asset inside the broader Goldfinch system

How Goldfinch Fits Into the RWA Narrative

Goldfinch is one of the clearest examples of a crypto project that fits the RWA thesis without focusing mainly on tokenized Treasuries.

A lot of RWA discussion in 2025 and 2026 has centered on:

-

tokenized Treasury bills

-

tokenized money-market funds

-

tokenized collateral

-

and tokenized stocks

Goldfinch sits in a different lane: private credit. That is important because private credit is one of the biggest and most institutionally relevant markets now moving closer to blockchain rails. Goldfinch’s current docs and site make this central to its identity.

This gives Goldfinch a differentiated position. It is not just another stable-yield wrapper. It is trying to bring a harder-to-access, institutionally significant credit market on-chain.

Why Goldfinch Matters

Goldfinch matters because it helps answer a key question in crypto: what kinds of real-world yield actually belong on-chain?

Private credit is a strong candidate because it is:

-

large

-

institutionally recognized

-

yield-focused

-

and historically hard to access for a broad investor base

Goldfinch’s Prime offering suggests that crypto rails are now mature enough to distribute this kind of exposure in a simpler form.

Goldfinch also matters because it represents a more substantive version of the RWA thesis. Instead of only tokenizing passive reserve assets, it is focused on a real financial sector where underwriting, diversification, and fund access matter. That gives it a more differentiated identity than many “yield” protocols.

Risks and Limitations

Goldfinch is promising, but it is not low-risk.

First, private credit itself carries real credit risk. Goldfinch Prime may offer access to major managers, but private credit is still private credit. Borrowers can default, funds can underperform, and diversification reduces but does not eliminate risk. Goldfinch’s own FAQ directly addresses the risks of private credit, which is a sign that this is central to the product and not a hidden detail.

Second, Goldfinch Prime is not globally open in the way classic DeFi products are. The FAQ specifically describes it for non-U.S. investors, which means jurisdiction and eligibility matter.

Third, token value capture is not always simple. Even if Goldfinch grows as a platform, that does not automatically mean GFI will track that value in a straightforward way. GFI clearly has governance importance, but governance tokens do not always price in ecosystem growth efficiently. This is an inference based on general market behavior, not a claim from Goldfinch.

Fourth, the product narrative has evolved over time. Goldfinch’s earlier borrower-pool and auditor/backer mechanics are still important to understand historically, but current user attention is now far more concentrated on Prime. That means readers should be careful not to mix the older protocol identity and the newer product identity as if they were identical.

Conclusion

Goldfinch is one of the most credible project names in the on-chain private-credit category because it has a clear mission, a differentiated asset-class focus, and a product that is easier to explain to real investors than many older DeFi lending systems.

Its current identity is anchored in Goldfinch Prime, which Goldfinch says gives on-chain access to diversified private-credit funds from large institutional managers. That is a meaningful step beyond the first generation of DeFi credit products.

Goldfinch is bringing private credit on-chain, and GFI is the governance token that helps coordinate that ecosystem.

As RWAs continue to expand beyond tokenized Treasuries into more sophisticated yield sectors, projects like Goldfinch show how blockchain can make institutional asset classes more accessible. For traders looking to stay ahead of emerging narratives—from private credit and RWAs to AI, PayFi, and tokenized market infrastructure—Phemex offers a secure and user-friendly platform to explore the market, monitor new opportunities, and sharpen your trading edge.