Key Takeaways

-

RE is the governance token of Re Protocol, a decentralized platform designed to bring regulated reinsurance exposure on-chain.

-

The protocol lets users deposit stablecoins into Insurance Capital Layers (ICLs) and receive yield-bearing tokens tied to different risk profiles.

-

RE is not the yield token itself. The main user-facing products are reUSD and reUSDe, while RE governs the broader protocol.

-

Re Protocol’s core pitch is that it opens access to the reinsurance market, a massive and historically institution-only asset class, through blockchain-based infrastructure.

-

The platform emphasizes fully collateralized deployment, on-chain transparency, third-party reserve attestations, and underwriting discipline.

-

The biggest attraction of RE is exposure to a new category of on-chain real-world yield. The biggest risk is that reinsurance is still a specialized, regulated, and operationally complex market.

RE is the native governance token of Re Protocol, a crypto project built around a very specific idea: bringing reinsurance capital markets on-chain. That already makes it different from most real-world asset tokens. A lot of RWA projects focus on Treasury bills, money market products, commodities, or private credit. Re Protocol is going after something less familiar to crypto users but arguably just as important in the real economy: insurance risk.

This matters because insurance and reinsurance are not fringe markets. They sit underneath modern economic life. Homes, businesses, vehicles, workers, and entire industries depend on insurance coverage, and behind those insurers sits the reinsurance market, where risk is passed to larger pools of capital. Re’s core argument is that this market is huge, yield-generating, and historically difficult for ordinary investors to access, even though it plays a critical role in economic stability.

What Re Protocol Actually Is

Re Protocol describes itself as a decentralized platform that uses blockchain infrastructure to connect on-chain capital with real-world reinsurance treaties. In simpler language, the protocol lets users deposit stablecoins into smart-contract-based capital pools. Those pools then allocate capital into fully collateralized quota-share reinsurance contracts through licensed insurers and related legal structures. In return, users receive tokenized positions that reflect different parts of the insurance capital stack.

Re Protocol users are not directly buying a token that simply represents insurance, instead they are entering a structured on-chain system that routes capital into regulated reinsurance arrangements and then turns that capital position into tokenized exposure.

That is why Re Protocol talks so much about transparency, collateral visibility, underwriting discipline, solvency, and reserve reporting. The project is not trying to imitate a pure DeFi yield farm. It is trying to turn a traditionally offchain institutional market into something blockchain users can participate in more transparently.

Why Reinsurance Matters

To understand RE, you first need to understand reinsurance. Reinsurance is often described as insurance for insurance companies. When insurers take on policies from homes, businesses, autos, or workers compensation, they do not always want to retain the full risk themselves. They can transfer some of that risk to reinsurers, which provide capital backing in exchange for premium income. This process matters because it helps stabilize the financial system. Without reinsurance, insurers would have much less capacity to write policies, absorb shocks, or survive concentrated claims events.

That is why Re’s homepage frames reinsurance not just as a financial product, but as a core piece of civilization technology. The basic point is that reinsurance is one of the systems that allows risk to flow away from concentrated exposure and into deeper capital pools. For investors, that creates an interesting opportunity. Reinsurance generates returns from insurance premiums, not from company equity growth, memecoin speculation, or even typical fixed-income instruments. That makes it potentially attractive as a relatively uncorrelated source of yield.

How Re Protocol Works

The mechanics of Re Protocol are built around Insurance Capital Layers, or ICLs. These ICLs are the protocol’s core vault structures. Users deposit approved assets like USDC, USDe, or sUSDe into an ICL. In return, the protocol mints a corresponding tokenized position, depending on which risk/return sleeve the user chooses.

The two main tokenized products are:

-

reUSD, the lower-volatility, principal-protected token

-

reUSDe, the higher-risk, higher-return profit-sharing token

Once deposited, idle funds are swept into custody infrastructure. When a licensed reinsurer draws capital under a legally binding Surplus Note, the funds move into regulated trust and reinsurance structures offchain. The protocol then mirrors important balances and flows back on-chain through reporting infrastructure and oracle feeds.

This is one of the key design features of the system. Re Protocol is not pretending the real-world piece disappears. Instead, it tries to make offchain movement more transparent by publishing reserve and portfolio data back on-chain.

So the workflow looks roughly like this:

-

user deposits stablecoins

-

protocol mints reUSD or reUSDe

-

capital is custody-managed and deployed through reinsurance structures

-

premiums and outcomes feed back into the token economics

-

users hold a liquid or semi-liquid tokenized claim on that capital exposure

The Difference Between RE, reUSD, and reUSDe

A lot of newcomers will confuse these three, so it is worth separating them clearly.

RE

RE is the governance token of the protocol. It is not the deposit receipt token and not the main yield token ordinary participants use for reinsurance exposure. Instead, RE sits above the system and governs things like protocol upgrades, reporting standards, technical permissions, committee formation, incentive policy, and governance procedures.

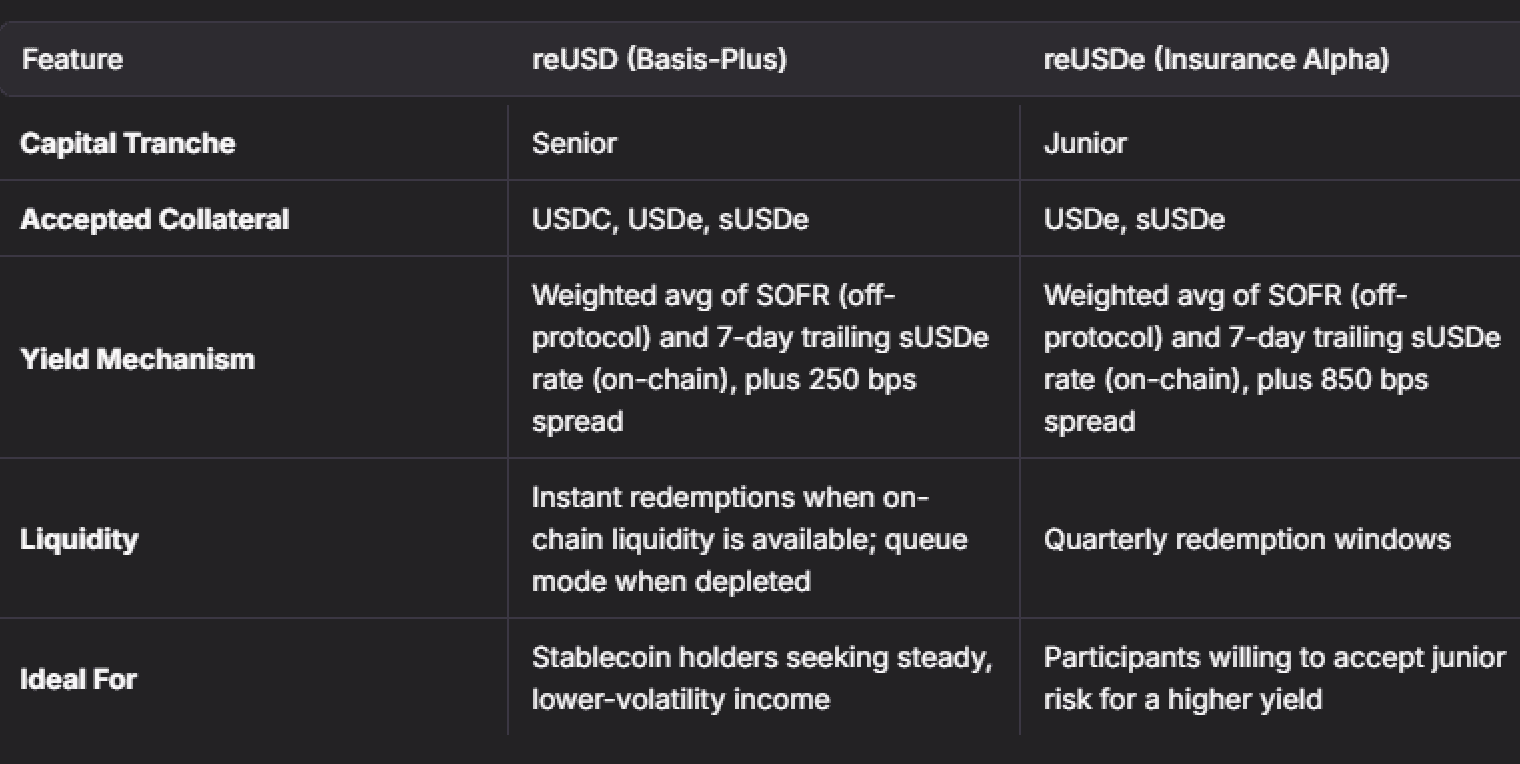

reUSD

reUSD is the lower-volatility side of the system. It is positioned as the stable core of Re Protocol. It’s described as a principal-protected, yield-accruing token whose daily return tracks the greater of a risk-free floor based on SOFR plus 250 basis points, or Ethena basis-trade yield plus 250 basis points. This makes reUSD more like a tokenized stable yield product with reinsurance-linked structure in the background, rather than a direct first-loss underwriting instrument.

reUSDe

reUSDe is the higher-beta side of the capital stack. It absorbs first-loss risk and participates in underwriting profits. It’s designated as the protocol’s performance token, designed for users willing to take more risk in exchange for higher returns. Historically, the docs reference net return ranges in the mid-to-high teens or above, though these are clearly strategy-dependent and not guaranteed.

So one way to think about the ecosystem is:

-

RE = governance and protocol coordination

-

reUSD = lower-volatility yield token

-

reUSDe = higher-risk, profit-participating exposure

Why Re Protocol Is Interesting

Re Protocol is interesting because it opens a part of finance that has usually been difficult for crypto-native investors to reach. Tokenized Treasuries are increasingly common. Stablecoin lending is already familiar. But tokenized access to reinsurance premium streams is much less common, and that gives the project a distinctive place in the RWA sector.

There are a few reasons this stands out. First, the return source is tied to real insurance premiums. That means the protocol’s economic base is not purely crypto-native demand. Second, reinsurance is often described as a relatively uncorrelated market compared with many traditional asset classes. That makes it potentially useful in diversified on-chain portfolios. Third, the protocol makes a serious effort to emphasize proof-of-reserves, custody visibility, actuarial review, oracle reporting, and legal structure. That is exactly the kind of infrastructure serious RWAs need if they want to move beyond narrative into actual financial use.

Transparency, Solvency, and Risk Controls

Because reinsurance is complex, Re Protocol spends a lot of effort explaining how it tries to reduce trust gaps.

The protocol workflow includes:

-

idle funds are held in Fireblocks vaults under multisig

-

offchain balances are attested daily by The Network Firm

-

those attested balances are published through Chainlink

-

smart contracts, tokens, and oracle infrastructure undergo audits

-

key controls are managed through MPC multisig systems

-

minting and redemption are permissioned for verified users only

The main point is that Re knows users will worry about the offchain bridge. Since the protocol depends on real trust accounts, licensed entities, and surplus note structures, it needs to prove that those balances and flows are visible. That is also why the protocol stresses verifiable solvency. It wants users to think of this less like a black-box RWA wrapper and more like a system where reserve conditions and collateral states are inspectable. Of course, transparency does not eliminate all risk. But it does make the product easier to evaluate than a structure where the user is forced to rely entirely on opaque issuer claims.

Governance and the Role of RE

The governance design is another important part of the RE token story.

According to the protocol docs, governance begins in a more centralized phase with a council of experts, blockchain operators, and reinsurance specialists. The long-term intention is to transition toward a DAO model as the platform matures.

This staged model is actually sensible for a project in such a regulated and operationally complex category. Reinsurance is not a market where every parameter can safely be handed over to token voting on day one. So RE governance is best understood as progressive decentralization with guardrails.

That also means RE is not the same kind of governance token as a pure DeFi protocol where tokenholders directly control all major decisions immediately. In Re Protocol, the governance layer sits alongside domain experts, legal structures, and regulated counterparties.

The Bull Case for RE

The strongest bull case for RE is that it opens access to a distinct real-world yield market that is much less saturated than tokenized Treasuries or generic DeFi lending.

A second bullish point is the structure. Re Protocol is not just saying “trust us.” It is making reserve reporting, oracle publication, collateral transparency, and underwriting discipline central to its identity.

A third bullish point is that the yield source comes from real insurance premium activity, which could make it attractive to users looking for on-chain returns tied to non-crypto economic activity.

A fourth bullish point is category differentiation. If RWAs continue expanding, protocols that expose users to unique asset classes may stand out more than yet another tokenized money market product.

The Risks and Weaknesses

The biggest risk is complexity. Reinsurance is not an easy market to understand, and that makes due diligence harder than with simpler products like tokenized T-bills.

A second risk is legal and operational dependence. The system relies on:

-

licensed entities

-

regulated trust structures

-

counterparties

-

custody providers

-

oracles

-

and actuarial processes

That gives the protocol real-world grounding, but it also creates more possible failure points than a fully on-chain native system.

A third risk is token-value capture. RE governs the system, but the direct yield exposure sits mostly in reUSD and reUSDe. Investors need to ask whether governance, incentives, and ecosystem expansion are enough to support long-term demand for RE itself.

A fourth risk is dilution. With only about 160 million of 1 billion tokens circulating, future supply expansion could weigh on price performance unless protocol growth keeps pace.

What Is RE in One Sentence?

RE is the governance token of Re Protocol, a decentralized reinsurance platform that channels stablecoin capital into fully collateralized, regulated insurance structures and tokenizes the resulting exposure on-chain.

Conclusion

RE is not just another RWA governance token. It sits on top of a protocol trying to bring reinsurance capital markets on-chain, which makes it one of the more distinctive projects in the sector. The broader Re Protocol ecosystem is built around reUSD and reUSDe, which let users choose between lower-volatility and higher-risk insurance-linked exposure. RE, meanwhile, governs the protocol and its evolution as the system moves from expert-led oversight toward more decentralized community control.

That makes RE interesting for two reasons. First, it gives exposure to one of the least-digitized but most important markets in global finance. Second, it shows how crypto can be used to create transparent access to markets that were previously difficult for on-chain users to reach.

The opportunity is real, but so is the complexity. Anyone looking at RE should understand not just the token, but the reinsurance market, the legal structures behind the protocol, and the difference between governance exposure and direct yield participation.